Money 2.0: Stablecoins and the New Financial Stack

How Stablecoins, Real-Time Payments, and Tokenized Yield Are Rewriting Finance

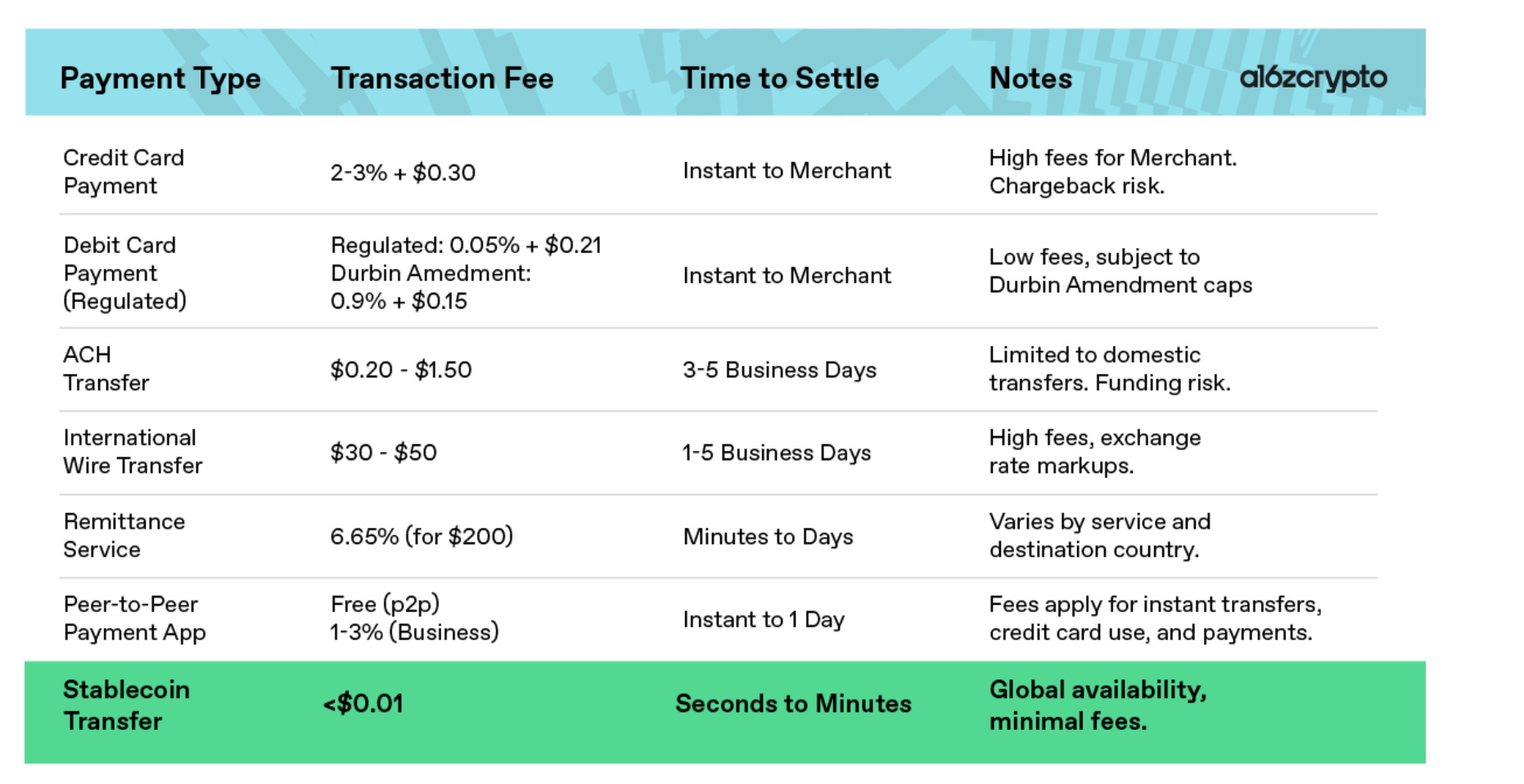

The buzz around stablecoins is deafening, and for good reason. They promise to slash merchant fees by roughly 60%,shrink cross-border transaction costs by an astounding 50-70%, and revolutionize treasury management through instant settlement and reduced capital buffers.

For too long, money has been synonymous with regulation, a heavily governed entity. But stablecoins usher in an era where money transforms into technology. The question isn't if this shift is happening, but how we seize this monumental opportunity. This piece dives into exactly that.

Why Are Stablecoins Even a Thing?

Why the sudden ubiquity of stablecoins?

It boils down to three powerful attributes: 24/7 instant settlement, affordability, and programmability.

While these concepts have been explored elsewhere, it's worth a quick refresher on their fundamental impact.

Instant 24/7 Settlement

Think of 24/7 instant settlement as a seismic upgrade from the traditional 24/5 banking schedule. This isn't just about convenience; it has profound implications. Primarily, it dramatically increases liquidity. Instead of funds languishing for up to seven days in intermediary accounts (like the arcane nostro/vostro systems of international transfers), money changes hands instantly. Secondly, real-time settlement significantly reduces both counterparty risk and the need for hefty settlement buffers.

What does this mean for businesses? Merchants, for example, can strategically hold idle funds in yield-bearing accounts for longer periods. Furthermore, with the reduction in settlement and credit risks afforded by instant settlement, they can allocate even more capital to these lucrative, yield-generating opportunities. In essence, businesses can retain control of their capital longer and put it to work immediately.

Stablecoins Can Be Cheaper Than Legacy Payments

Yes, stablecoins are cheaper. While there's some debate over whether this holds true given currently non-insignificant on/off-ramp fees (though these will likely reduce as more competitors join), if the money stays and settles on-chain, then this claim is certainly valid.

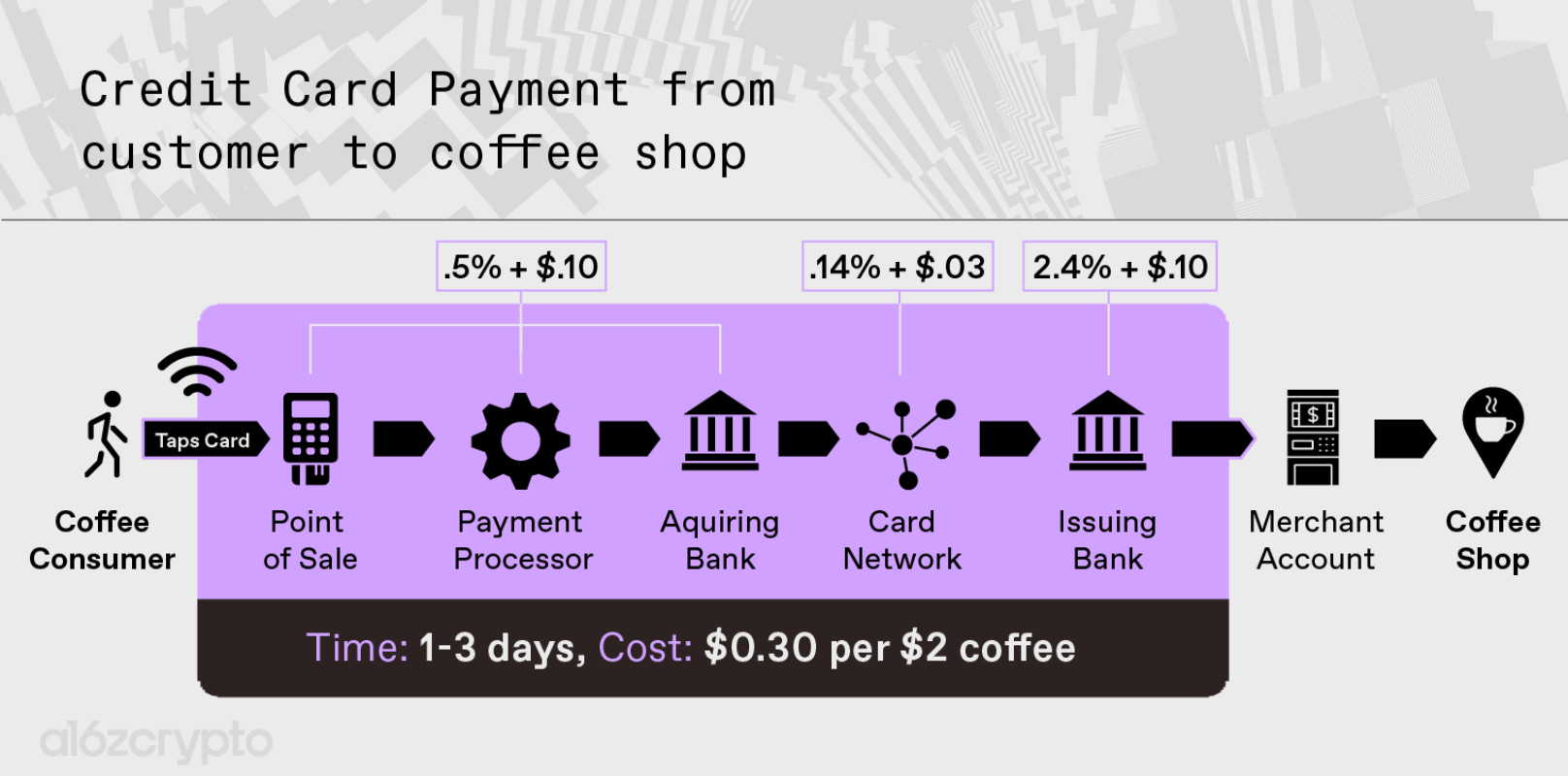

a16z made calculations of how much merchants save by shifting to stablecoin rails, especially in the US where the interchange isn’t capped like it is in Europe.

First, let’s go through cost savings on processing fees. In the US, credit card charges to merchants are typically 2.9% + $0.30 per transaction, whereas Stripe’s new stablecoin transaction fees are 1.5% per transaction. So, on a $5 coffee (a slightly more realistic price point than a16z’s example), Starbucks would pay $0.075 with stablecoins versus $0.445 in traditional fees, saving 83%.

In addition to saving on processing fees, merchants also save on cross-border fees. As per a16z, merchants can save 99.9% on these fees (from $44 to $0.01 on average).

Finally, merchants save by simplifying their backend reconciliation processes. For a single mid-sized merchant, annual backend reconciliation costs (labor, outsourcing, compliance) can easily range from $20,000 to $50,000 or more.

Stablecoins Create New Sources of Revenue for Merchants

Currently, under the GENIUS Act, non-financial companies (like traditional merchants) generally cannot issue stablecoins unless they receive rare, high-level regulatory clearance.

While this is still speculative, it's possible that non-bank entities like large merchants (Walmart, Amazon) will, at some point, be able to legally issue stablecoins and gain incremental passive treasury yield. After all, MercadoLibre, the Latin American e-commerce giant, has already launched its stablecoin.

Instead of large loyalty programs like Starbucks’, where customers preload funds onto their Starbucks accounts, stablecoins would allow for a similar closed-loop payment ecosystem while giving customers increased flexibility. How this would happen is that Amazon could give a 10% discount on products purchased with Amazon’s stablecoin, let’s call it “AmazonUSD.”

While skeptics might argue that merchants like Starbucks benefit from unused prepaid funds (in 2024, Starbucks generated $207.6 million in revenue from unused prepaid funds), there are a few counterarguments:

a) Consumers will be getting smarter as competitors start to offer less extractive native stablecoins that can be converted to any other digital USD version and don’t expire.

b) The addressable participant pool will increase; that is, more people will be willing to hold Amazon’s or Starbucks’ stablecoin just in case, if they know they can at any minute exchange it for USDC.

c) While merchants may lose on extractive closed-loop revenue sources like unused prepaid funds, they could gain from minting fees, and even LP fees through "LP-as-a-service" companies, or by lending out their stablecoin to market makers for extra yield.

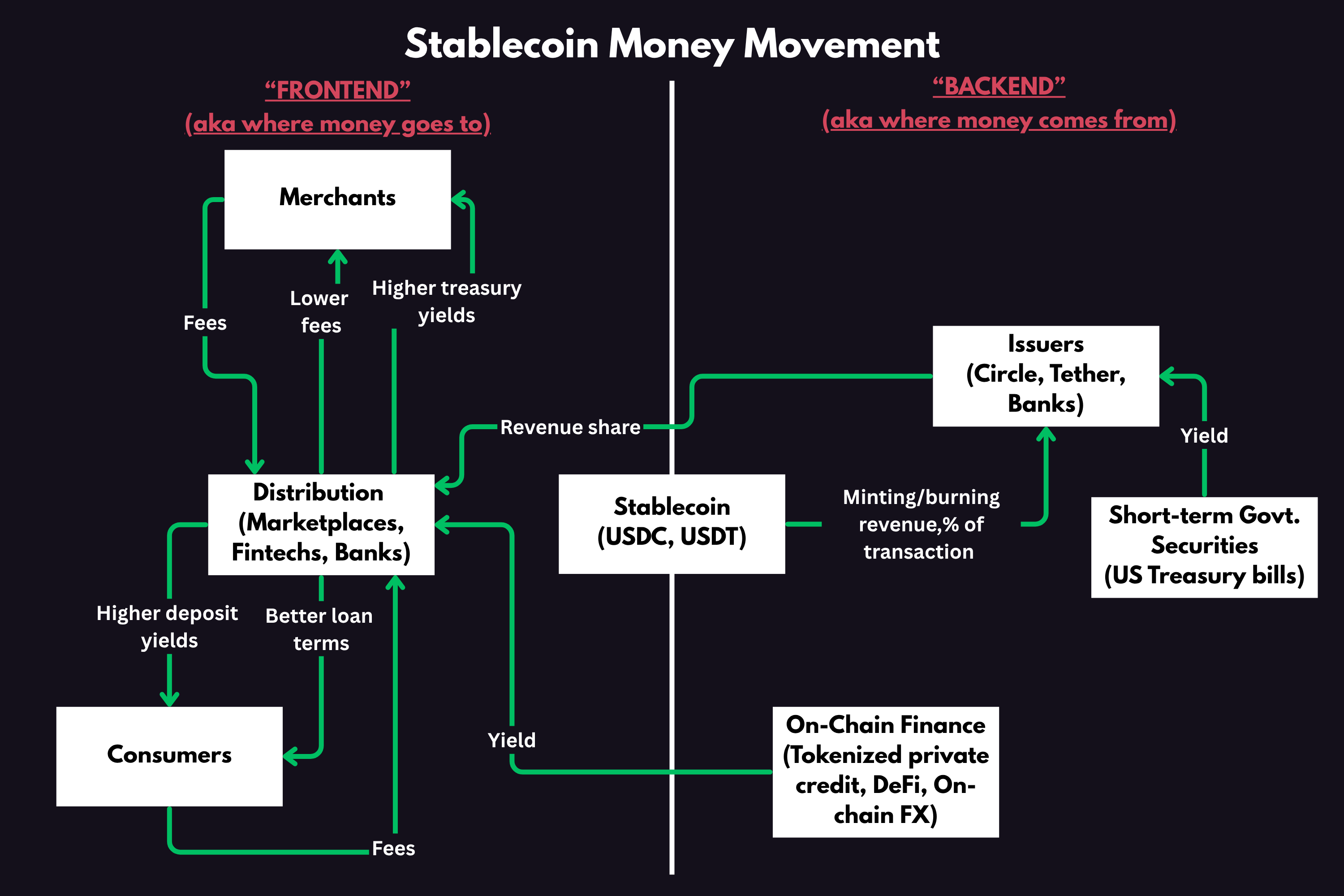

The Stablecoin Money Flow

Recently, a bank asked me, “who gets the money” in stablecoins. The answer to this is multi-sided. Below is a simplified visualization on how the money flows and where it comes from in the stablecoin ecosystem.

Before we dig deeper into some of the key players in the ecosystem, there are interesting takeaways that come from the above visualization:

Stablecoins are a mechanism for packaging treasury, private credit, and DeFi yield into better consumer terms. Stablecoin treasury yield means stablecoin issuers and distributors don’t have to levy as extractive fees.

There are two layers that unlock additional income for stablecoin issuers and distributors: 1) yield from treasuries, and 2) efficiency gains from 24/7 settlement and real-time tracking inherent in blockchain technology.

Non-bank entities (e.g., large merchants) will potentially start looking more like banks in the future—think Starbucks rewards program but with real-time digital dollars instead of prefunded accounts.

Stablecoin distributors could become the “closed loop” payment networks (where the network controls relationships with both its cardmembers, i.e., the customers, and merchants, i.e., where cards are accepted), as opposed to current open-loop payment systems.

How Stablecoin Issuers Make Money

The short answer is that they do, and they don’t.

First, how do they make money? In three main ways: 1) money market yields, 2) minting and burning fees, and 3) listing fees (popular stablecoins get paid tens of millions of dollars by blockchains for listing on said blockchains).

While minting, and in some cases redemption, fees are “only” ~0.1%, EU and US regulation doesn’t allow the yield to be passed down directly to consumers. This means stablecoin issuers get to keep the difference. However, regulation also states that these yields have to come from the safest (and lowest yield) sources—one of the reasons why Tether has been banned in Europe. This limits their opportunity for financial engineering. These yields will likely compress in the future, not only due to lower interest rates but also increased competition.

While Tether is the most profitable company per employee ($93 million profit per employee) with 74% net margins(net income divided by revenue), Circle has below-average net margins of 9.3%, which places it under the S&P500 average of ~12%.

Why are Circle’s margins so low versus Tether? Because it pays a lot for distribution. It paid $908 million (or roughly 54% of its revenue) in 2024 alone to Coinbase for distribution.

This gives us a glimpse into how the stablecoin ecosystem might look as the market gets flooded with new stablecoins. Companies with pre-existing distribution, like Tether, will have high margins, while new upstarts, even relatively powerful ones like Circle, will have to compete (and pay) for distribution. In short, the companies that stand to gain the most here are financial networks with existing distribution, like exchanges (Robinhood, Coinbase) and banks (BofA, Citi, JPM). Imagine Binance listing fees but for stablecoins.

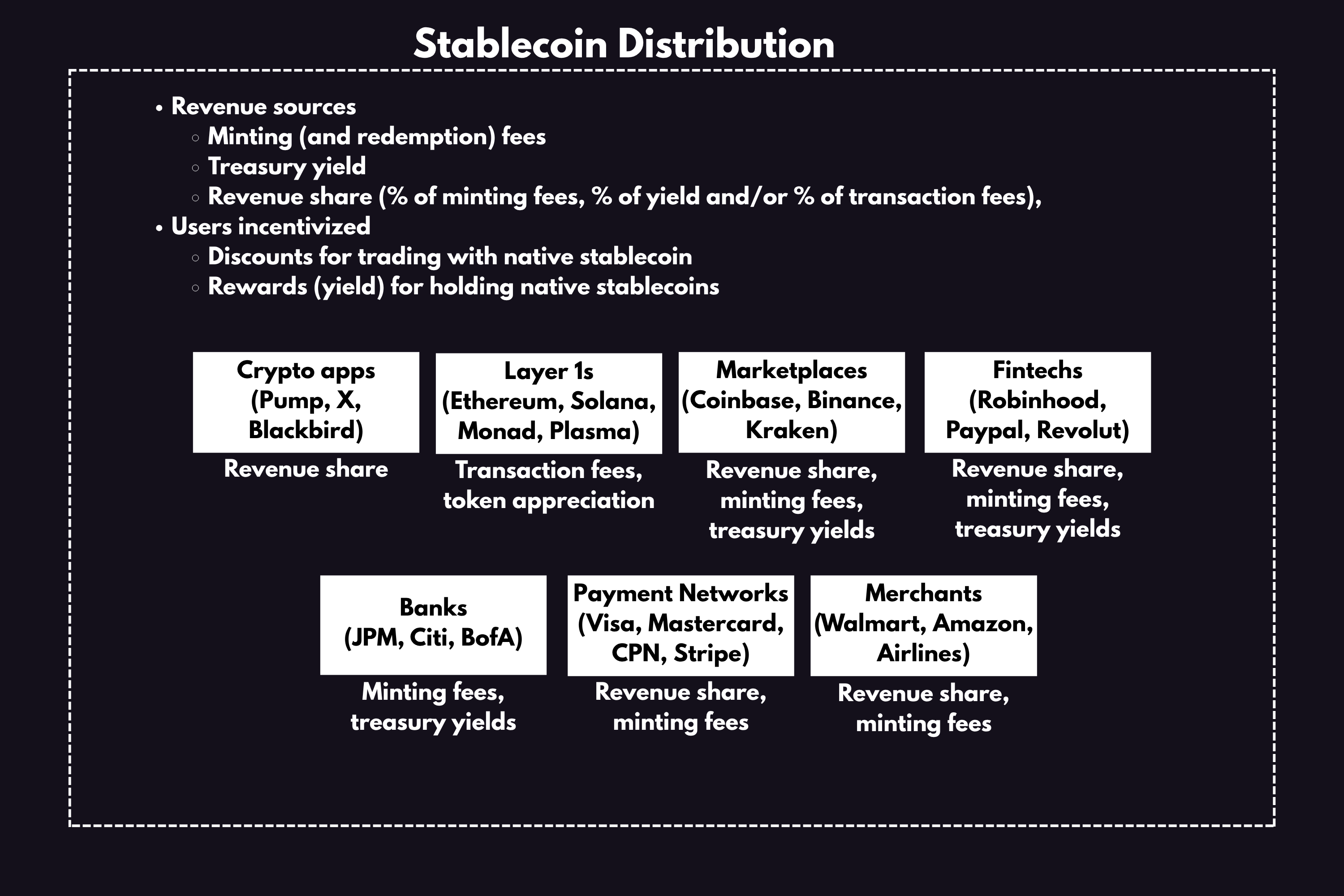

How Stablecoin Distributors Are the Likely Winners of the Stablecoin Wars

Where stablecoin issuance is more about regulatory arbitrage, stablecoin distribution is where most of the value will be captured. The reason Tether doesn’t have to pay $900M+ to Coinbase like Circle is that it already has great distribution, specifically among traders and in Asian markets.

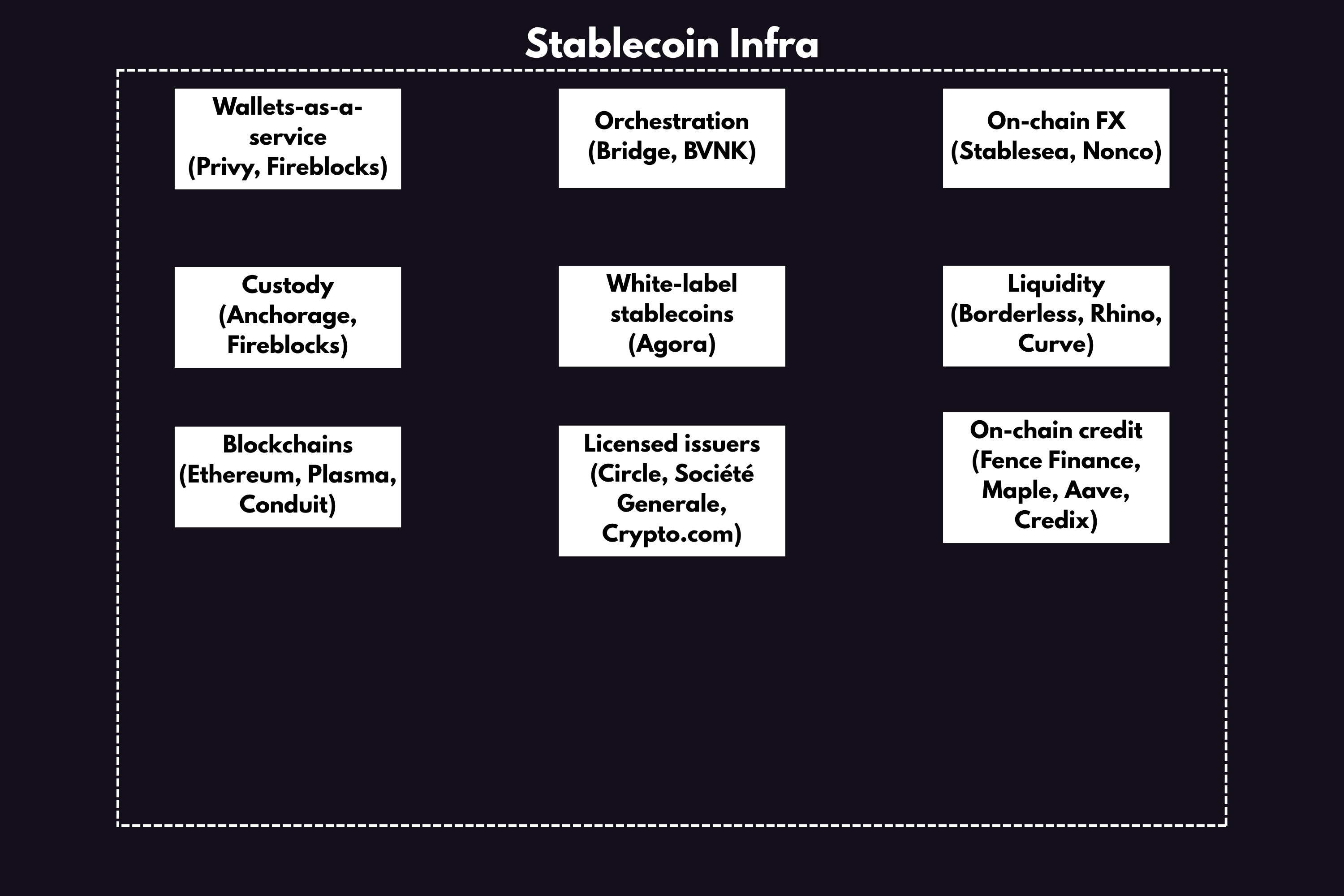

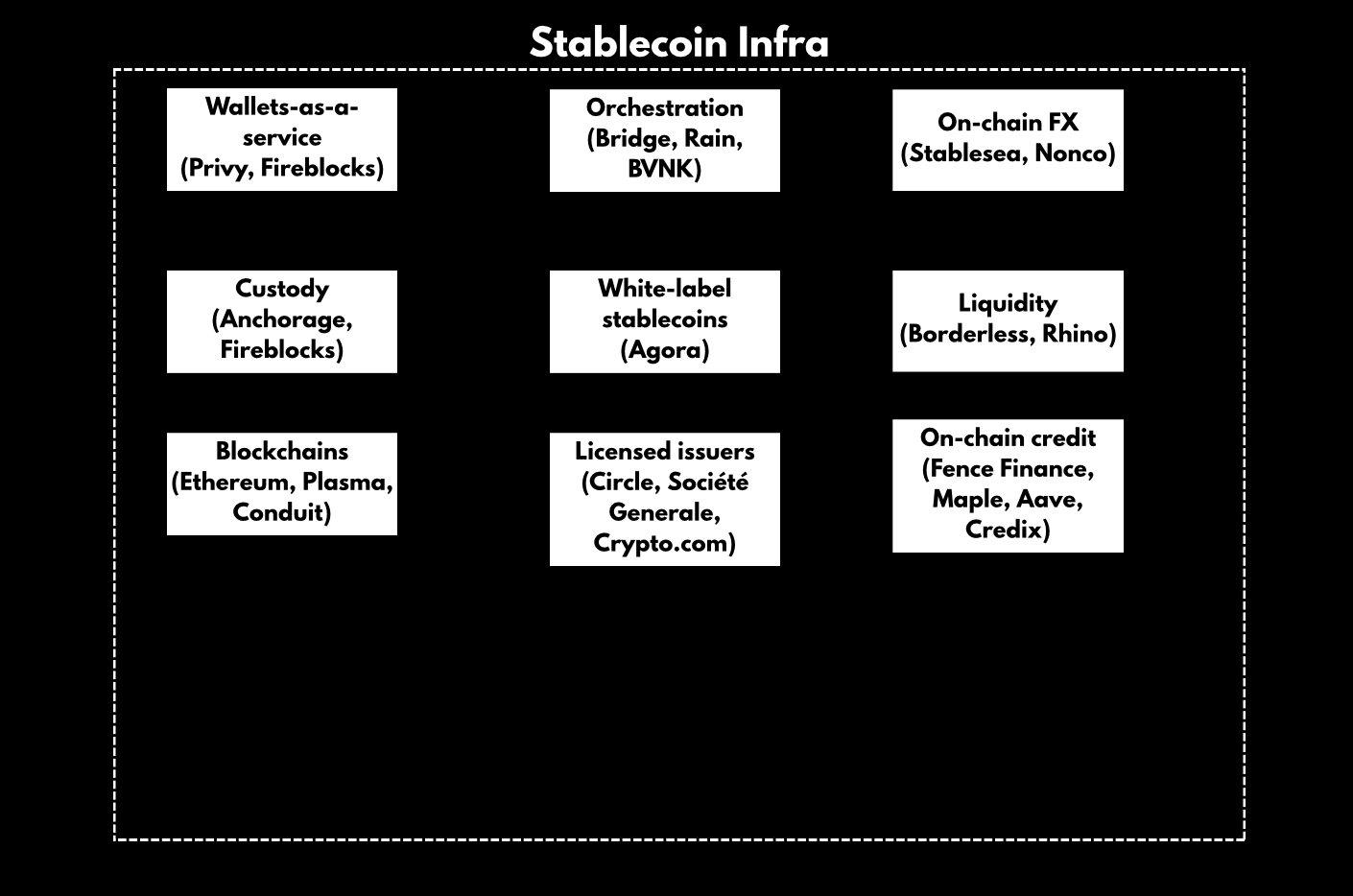

I’ve created a visual categorization of stablecoin distributors below. These include: crypto apps, Layer 1s, Marketplaces, Fintechs, Banks, Payment Networks, and Merchants. While value accrual will happen at the distribution layer, there is increasing competition among them.

There are four main competitive levers that distributors can try to optimize for:

Retail customer wallet share: Who has the closest relationship with retail customers? Fintechs like Revolut, X, and PayPal have an edge here, as do marketplaces like Coinbase and Robinhood.

DeFi acceptance: Which stablecoins will be the golden standards in DeFi? The highest market cap ones could have an an edge (e.g., USDC, USDT). On the other hand, smaller, less popular stablecoins will likely pass on more of their yield via incentives, making them more competitive.

Decentralized trading: Which stablecoins have the deepest liquidity versus other stablecoin and crypto pairs? Most popular (highest market cap) coins have the edge here (USDC, USDT).

Regulatory arbitrage: Which companies can legally issue stablecoins? Circle, other first movers, and big banks like Bank of America, BBVA, and Citi have an edge here.

In summary, there are network effects: larger market cap equals more liquidity, which equals better on-chain FX rates, which then leads to higher DeFi acceptance. All this drives higher revenue, which in turn leads to better distribution (via marketing or acquisitions).

However, at this stage, it’s still unclear which stablecoins will accrue the strongest network effects.

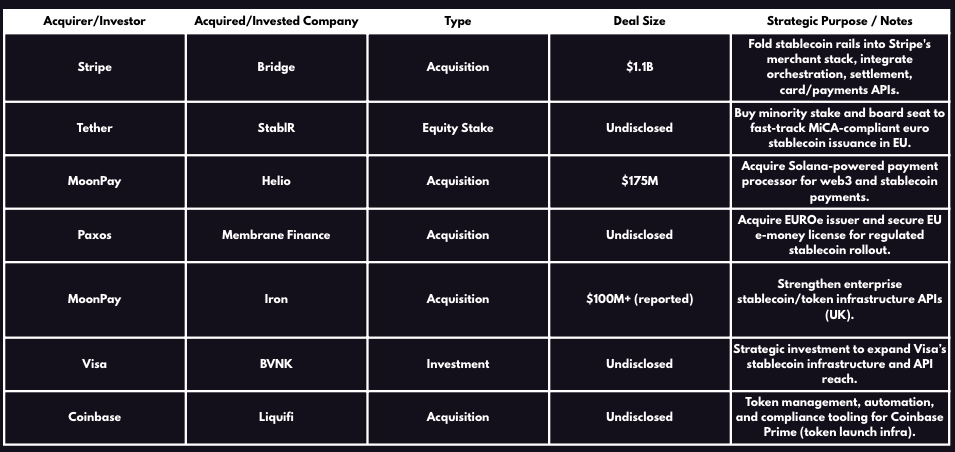

Stablecoin Infra Will Be M&A Playground

We’ve already seen this happen through multiple investments and acquisitions. Some of them are highlighted below.

There are four trends I’m seeing related to stablecoin infrastructure:

Big players like Stripe and Coinbase are acquiring stablecoin infrastructure companies in efforts to become their own self-sufficient payment networks.

Big fintechs like Revolut or Robinhood are “co-opting” crypto innovation. We’ve consistently seen these take innovations from the crypto world and apply them to their own ecosystems, from yield accounts to tokenization.

Infrastructure companies are also starting from a single use case and expanding to a full-stack solution. For instance, Bridge started as a stablecoin on-ramp, but has become a full-stack stablecoin orchestration platform. Due and Mural Pay are creating payment networks, especially in emerging markets.

New innovative companies will come out of creative M&A deals that package different infra layers into full-stack or semi-full-stack orchestration offerings.

In sum, consolidation will occur; Stripe’s Bridge and Privy acquisitions were just the beginning.

New Financial Products Will Come to Be

While enhancing existing financial pipes is a great opportunity for incumbents and upstarts alike, I’m most excited by the net new financial opportunities stablecoins (and more broadly, tokenization) bring.

I would categorize new financial products in the following way:

New way of doing old things

These are more efficient ways of running legacy systems—e.g., JPM Coin, tokenized private credit, instant delivery versus payment (the exchange of asset(s) and money). These are like clean tap water: they should be a basic right across the globe, but aren’t (usually due to legacy pipes). These include:

Not having to pay thousands of dollars just for sending money from one business to another.

Not having to pay 6% on average on remittances.

Not having to wait 3 working days to send money to a broker.

The ability to trade in and out of stocks whenever, wherever.

The ability to trade stocks at low fees.

New ways of doing new things

This happens when new mechanisms are combined with new service models—e.g., agentic payments.

Mechanism: While chargebacks have been the mechanism of keeping two transacting parties honest until now, blockchain allows new ways to maintain honesty:

Atomic swaps: (e.g., Agent A receives payment only if Agent B delivers service).

Slashing: Just like in proof-of-stake systems, a dishonest party gets their stake (e.g., in escrow) slashed and redistributed.

New service/business models

Investing in autonomous AI agent outputs (think owning shares in an AI agent) and AI agent-to-agent and platform payments. Most AI companies already use Stripe for payment processing (78% of the Forbes AI 50 companies build on Stripe), and while Stripe is championing stablecoin accounts as the new payment infrastructure, using stablecoins as payment vehicles for AI agents is actually not that unlikely.

Creating markets for new assets via AMMs and other autonomous pricing mechanisms.

Democratized payables and receivables markets—new cashflow-generating investment vehicles.

“Truth” markets—utilizing financial stake for determining “objective” truth.

Dynamic information markets—paying on-demand for knowledge bases used.

Culture markets—prediction markets on cultural relevance, NFTs.

Personal data markets—selling your own data.

Public IP markets—unbundling and investing in IP (anyone can try to be the modern-day micro-Medicis).

Compute markets—GPU and other granular resource markets.

These net-new asset classes aren’t just about digitizing existing value; they’re about unbundling, financializing, and creating liquid markets for intangible or previously non-tradable forms of value.

How You Can Make Money

Finally, you might say, “Okay, so what? How is this relevant to me?” It very much depends on which of these groups you belong to.

Builder

Based on recent history, the best exit opportunities seem to be in creating infrastructure that the Coinbases, Revoluts, and Stripes of the world can plug into their machinery. Incumbents are usually too slow and way behind the curve to build out services in-house. These could be wallets (Privy) or stablecoins as a service (Bridge). In the past few weeks alone, we’ve seen Coinbase acquire LiquiFi (automated payroll and token vesting), Thesis acquire Lolli (Bitcoin rewards), and Monad acquire Portal (stablecoin infra).

Particularly, bridges between the real world and the digital one are a compelling opportunity, as they are relatively new categories and ripe for innovation.

However, instead of just looking where we are currently, it would be beneficial to look where the puck is going. Ask yourself: assuming everything will run on stablecoins, what happens then?

Some first-principles conclusions are:

You will have to be able to swap different currencies at good rates (on-chain FX), especially low-liquidity yet popular corridors.

Just like with lending, at some point banks and other financial institutions will likely lobby for more lax constraints for stablecoin collateralization requirements. Risk management abilities will be key in this scenario.

Providing better yield for stablecoins. While stablecoins themselves cannot pass on yields, separate yield engines behind them can (yield-as-a-service), not too dissimilar from Pendle. Yield amount, regulatory compliance, and safety are key. As in DeFi, stablecoin yields will become a differentiating factor for stablecoin platforms.

New ways to finance short-term working capital credit (think account payables and receivables).

Privacy-preserving technologies (like zk) for public blockchains will become important for institutions to hide their transactions.

New asset types will be tokenized. Things like IP, healthcare data, transparent carbon credits, public infrastructure projects, litigations (you can fund and benefit from lawsuits), and real-time payment streams(e.g., invest in your or another specific neighborhood by purchasing residents’ recurring bill payables).

Embedded and programmable payments. These will be to stablecoin infra what chargebacks and other value-added services are to the incumbent card networks.

On-demand, machine-to-machine, and agent payments. Smart contract programmability (e.g., atomic swaps which ensure fair exchange of assets/services) as well as Coinbase’s standard x402 have a lot of potential here.

While we have some early winners already (Bridge/Stripe and BVNK), it’s still early days. If you build something better (e.g., a better stablecoin liquidity engine), the open nature of blockchains means it can be implemented by all.

The beauty of it all is that building is open to anyone. As builders solve their own problems, it will ensure a wide variety of services—a 16-year-old student from Nigeria will build something different from a 32-year-old accountant from California.

Investor

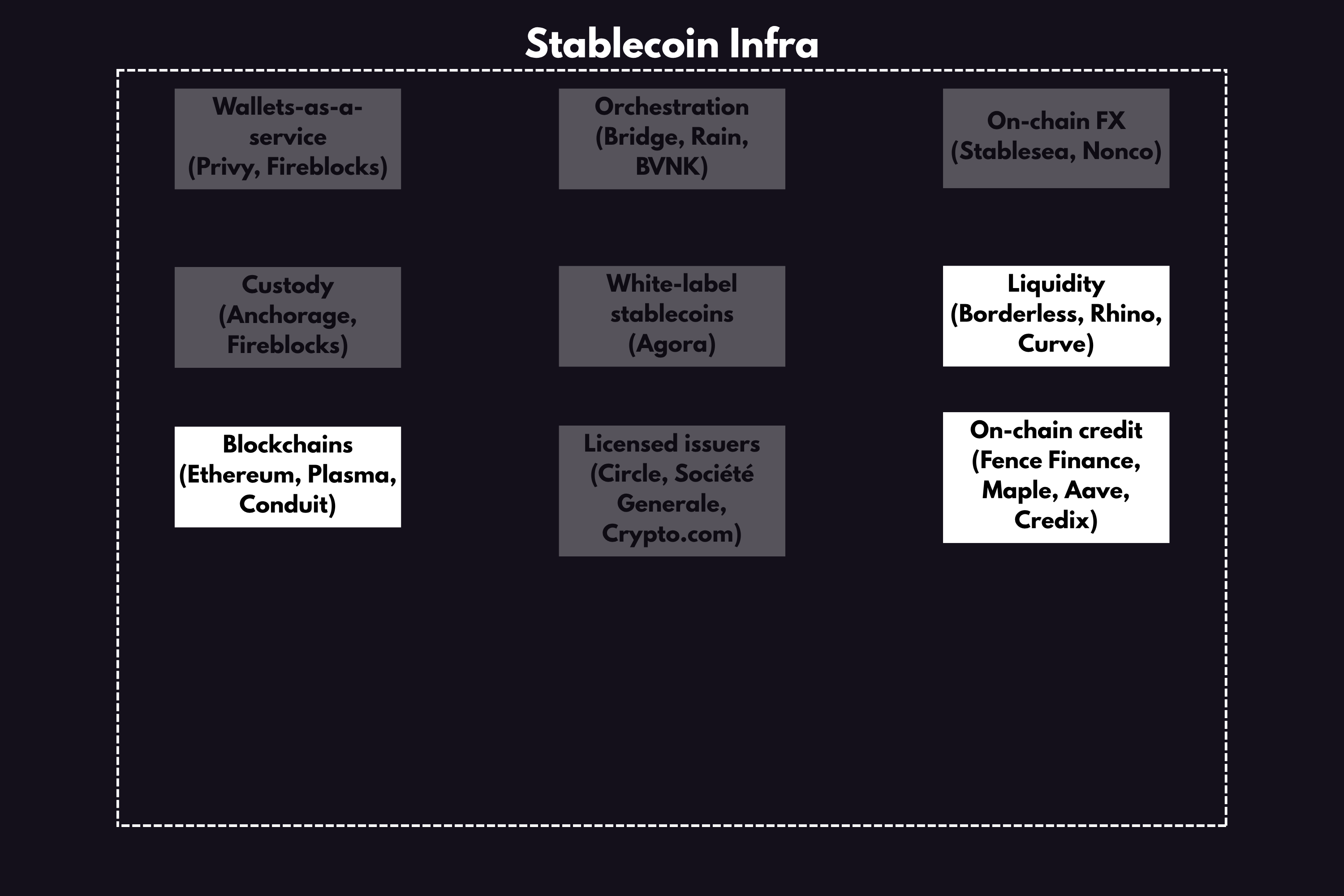

As an investor in liquid tokens (already publicly tradable tokens), the key is to find tokens that benefit from, and ideally front-run, the narratives in different token categories.

The highlighted boxes are where most current liquid investment opportunities lie.

For instance, on-chain FX sounds a lot like what Curve and Convex have been doing for years now.

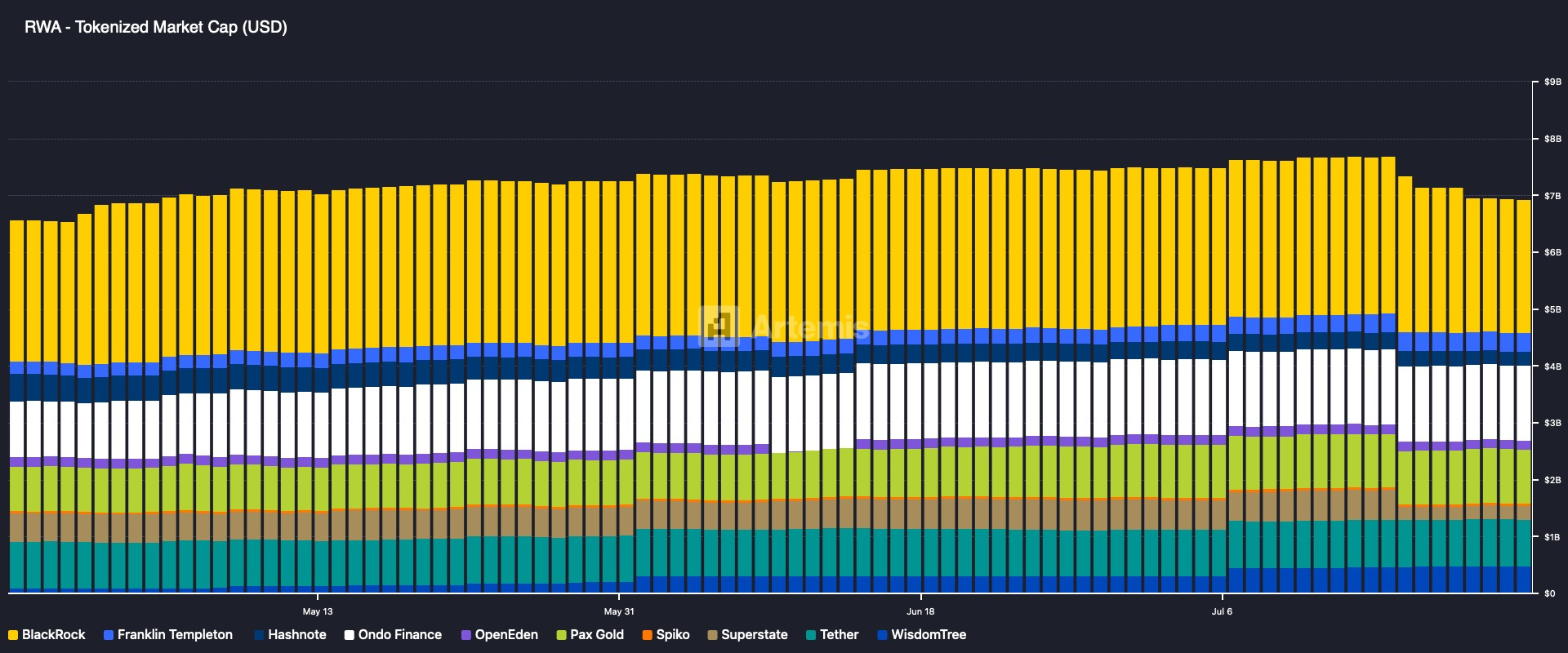

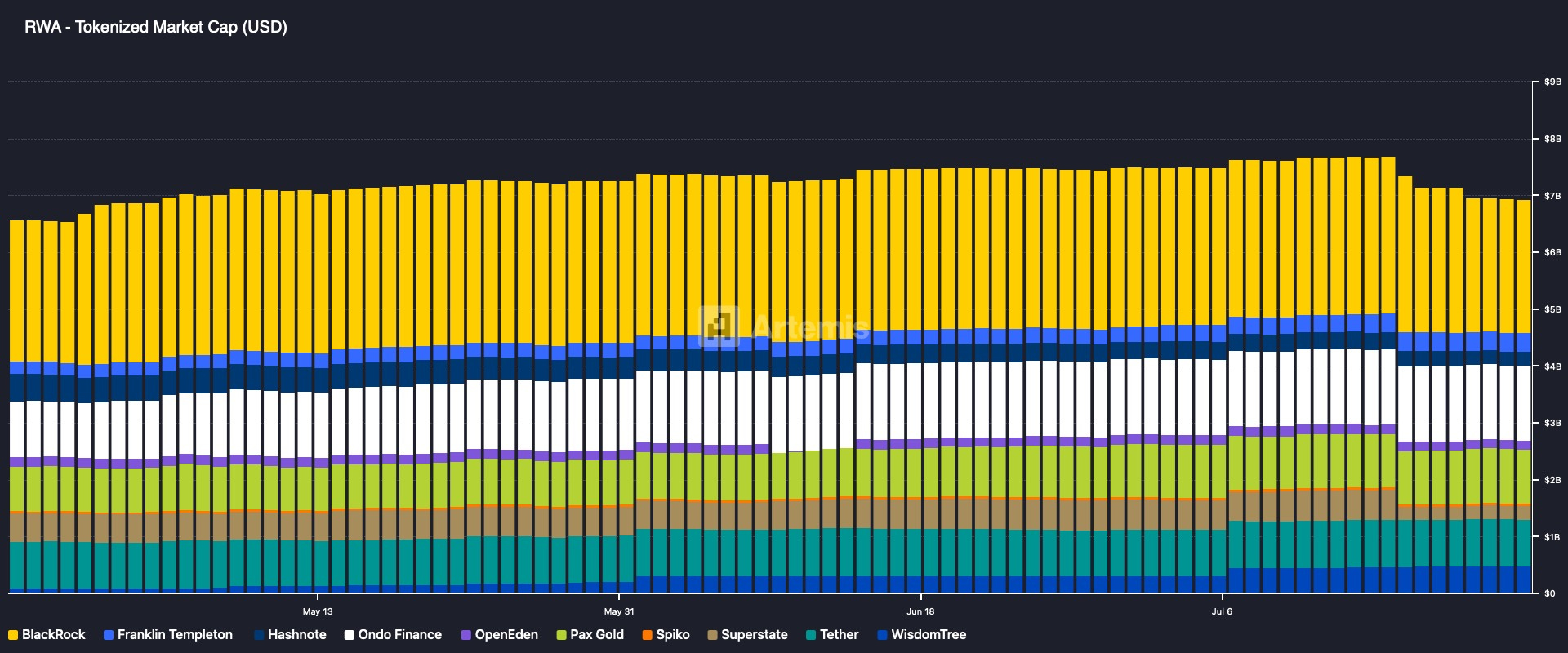

For stablecoin and RWA blockchain rails, think: are there any high-throughput L1 or L2 chains that could be used to build stablecoin on?

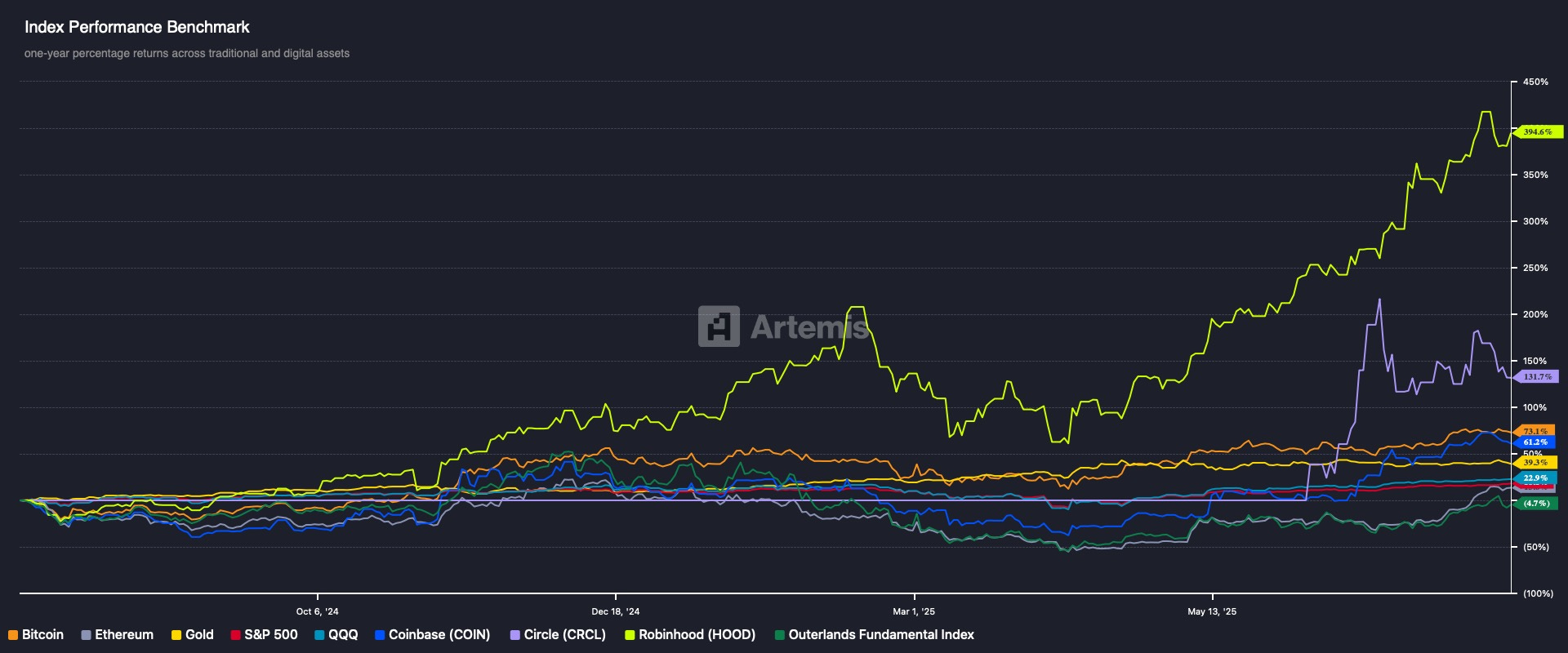

We saw how much SEI pumped just from being a finalist in the race for Wyoming’s stablecoin blockchain. Aptos was the other finalist. (Perhaps they read my coverage on both of them :))

Arbitrum pumped from Robinhood using the chain for tokenized stocks.

Plasma (Tether’s upcoming L1) is another obvious choice due to Tether’s distribution (however, it’s not a liquid token yet).

Ondo launched an L1 that tokenizes institutional-grade real-world assets.

Ethena partnered with Securitize (a leading real-world asset tokenization platform responsible for tokenizing funds for BlackRock, KKR, Hamilton Lane, and Apollo) to launch the Converge L1 blockchain.

On the institutional DeFi and yield side, we have protocols like:

Maple – Institutional-grade lending with high yields

Aave – The golden standard and is increasingly leaning toward institutional lending (white-label deal with Kraken’s Ink platform).

Morpho – Creates new lending markets for any assets, which could cater to more exotic, long-tail assets.

And more.

The key here is to buy these before big announcements, instead of chasing rallies.

Stocks have also become a way to invest in crypto innovation, as more and more crypto companies list there first. Ironically, the most pure-play stablecoin investment, Circle, was first available for stock market, not crypto, investors. Coinbase and Robinhood are also investable. In fact, Robinhood has been among the best-performing TradFi plays this cycle.

Kraken's ICO is also something to watch out for.

Another option (albeit my least favorite at the moment) is to invest in crypto treasury plays—i.e., companies that buy cryptocurrencies with their corporate treasury. These are essentially leveraged plays on the underlying crypto assets (BTC, ETH, SOL, HYPE). However, these have idiosyncratic risks like fund structure, which may cause investors to lose despite the underlying asset going up.

Investor (Venture Capital)

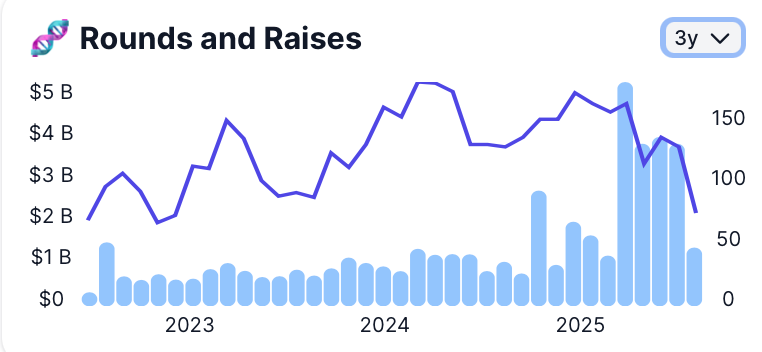

Many VCs have more ways to invest in the stablecoin boom. It’s no wonder we’ve seen a three-year high in fundraising rounds.

Some of the more interesting protocols that recently received funding:

Some of the more interesting protocols that recently received funding:

Paradigm led the $50M Series A for Agora (white-label stablecoin service)

On the DeFi front Kuru (a non-chain orderbook exchange protocol I mentioned in October) raised $11.6M led by

OpenFX – FX infrastructure for real-time cross-border payments

Limitless — Prediction markets Strategic round led by Coinbase Ventures

Mirage – Self-repaying stablecoin loan powered by perps

Veda – Stablecoin yield backend for institutions

3Jane – “Yieldcoin” backed by a pool of credit lines to crypto users and AI agents secured against future yield. Credit lines are underwritten against verifiable proofs of credit scores, onchain/CEX/bank assets, and cash flows.

Conduit Pay – Infrastructure platform for stablecoin-based payments

Codex - Stablecoin L1

Dragonfly has led quite a few interesting investments in the stablecoin space, making 11 investments since March 2025, from stablecoin L1s to perps on Monad.

Takeaways

While stablecoins and RWAs often get bundled together, a good mental model to think about them is this:

Can I trade it?(RWA, AMMs, private credit) or

Can I move it? (Payments).

For stablecoin companies, the key question is: will they become the new for-profit payment rails, or will they become a public good? Venture funds like Dragonfly seem to bet on the former, while a16z’s Chris Dixon believes the latter.

The value proposition for users is that stablecoins are cheaper and faster. To remain cheaper, they by nature have to have a margin lower than those of incumbents. On the other hand, payments can be the loss leaders for the ultimate cash cow, which is yield from tokenized treasuries. In this case, scale matters.

Another point is that increased stablecoins will chip away at the market share from cash. Or perhaps this will go the way of courier services, where expedited delivery fetches a premium.

Whichever the case may be, it seems that this has been the 0 to 1 moment among TradFi we’ve been waiting for years.

Opportunities abound everywhere you look.

Be at the forefront of digital assets with the likes of UBS, H&M, FT, Solana Labs, Nike and many more. To receive new posts and support my work, consider becoming a free or paid subscriber.