The Banks’ $4 Trillion Stablecoin Problem

We’re back.

While posting under the pseudonym The Naked Collector, I realized the newsletter never had an official name. With a new design and broader scope, now expanding beyond crypto into the Internet economy, it feels like the right time to define it. The new name, Internet Economy, reflects this shift, from crypto-based stablecoin payments to AI agent credits to cultural markets, and everything in between.

Many newsletters end up repeating the same news, offering little original perspective. Instead of the 11th generic take on Polymarket’s $9B valuation, I aim to provide original commentary that connects past trends with emerging developments.

If you find value in this newsletter, I’d be grateful if you shared it with someone who might benefit from it.

While crypto markets remain as volatile as ever, we’re also seeing new battlegrounds emerge across crypto, payments, and AI.

These are the trends and ideas you should be paying attention to right now:

The Fight for New Payment Rails

Arc Invest predicts AI-facilitated online spend will reach $8 trillion by 2030 (I actually believe this will be way higher as it shouldn’t be limited to the realm of e-commerce). This is why agentic payment rails are being fought over by incumbents like Visa Intelligent Commerce, Mastercard Agent Pay, Google Agent Payments Protocol, and newcomers like Coinbase x402/stablecoins (including Cloudflare’s NET Dollar). The biggest questions here remain buyer intent and chargebacks, i.e., did the buyer intend to purchase the item, and what if the wrong or faulty item was purchased? The Google Agent Payments Protocol tries to solve the former while Visa thinks they have the edge in the latter (via Intelligent Commerce).

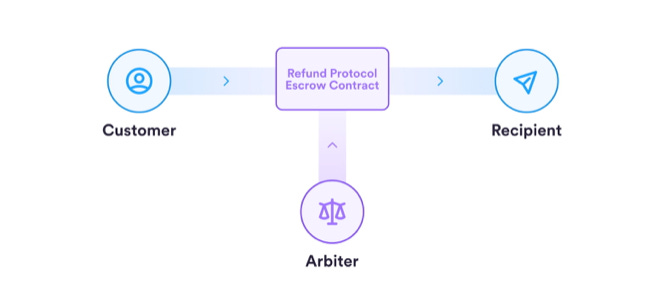

People were shocked to hear that Circle will likely introduce reversible transactions. This isn’t surprising.

They’ve been developing a Refund Protocol (essentially a third-party escrow smart contract that locks part of the funds before releasing them to the recipient). This then in effect makes the stablecoin transactions not instantly settled, questioning their value-add.

I believe there are four solutions to this problem:

Payments from stablecoin wallets will continue to go via Visa, Mastercard, Amex, etc. rails, and chargebacks will be their responsibility

Payment networks will de-bundle their risk and chargeback modules (as they already have with other parts via a growing number of APIs) i.e., chargeback-as-a-service

Circle (or Layer 1s like Tempo, Arc, etc.) copy the TradFi model and move away from instant settlement in favor of chargebacks

Independent, specialized on-chain arbiters and chargeback providers. Their role would be to specialize in adjusting the risk parameters similar to how DeFi curators like Gauntlet or Steakhouse adjust lending-related parameters. Heck, I could even see receivables purchasing and staking pools that pool buyer and merchant wallets together, where the rewards (or APY) come from bad actors (fraudulent chargeback requests on the buyer side, or merchants not delivering promised products) and are redistributed to the good actors. Being part of such insurance networks (e.g., a soulbound NFT is minted to participants) would create added trust for merchants and buyers and could even be mandated for transactions or discounts.

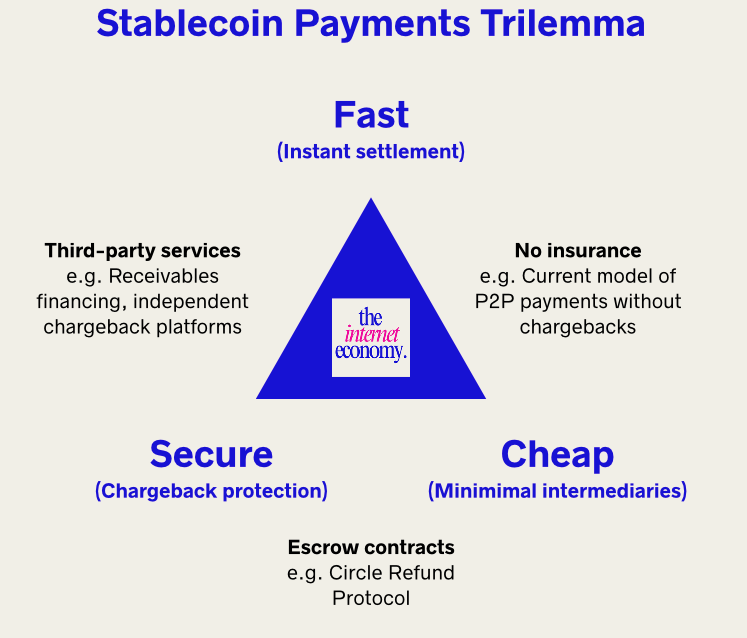

So far, there is no single elegant solution to solve this, and each intermediary introduces a fee and possibly additional time, moving us away from the promise of cheap and fast stablecoin settlement. Instead of the blockchain trilemma of decentralization, security, and scalability, we have the stablecoin payments trilemma of speed, affordability, and security.

The advantage the traditional card payment rails have is they’re able to pull funds from the merchant after the customer initiates the chargeback request, whereas stablecoin transactions (assuming not via payment cards) are push-only (they’re able to send but not pull regular payments e.g., chargebacks or things like subscriptions).

Before we lose all hope and ask “why don’t we just use regular card rails,” we can see the growing demand for A2A (account-to-account) and other payment methods that bypass the card rails. Motivation for that is similar to that of stablecoin payments: lower fees for merchants and consumers and more instant settlement. Crucially, it also prevents credit card fraud.

A2A also gives us a preview of how chargebacks might look in a non-card system. Where chargebacks don’t exist by default, we can look at the A2A (account-to-account) payment space. There, Visa introduced the Visa A2A Hub, a dedicated A2A solution for bill payments (e.g., utilities, rent) that includes formal dispute resolution processes, integrated fraud monitoring, and enhanced consumer protections. The protections won’t be as comprehensive, but neither will the fees.

It’s also unsurprising that APAC, the region of Alipay and WeChat, will be leading the charge of non-cash but also non-card transactions. This provides a good breeding ground for non-card experimentation.

The Fight for Legacy Payment Rails

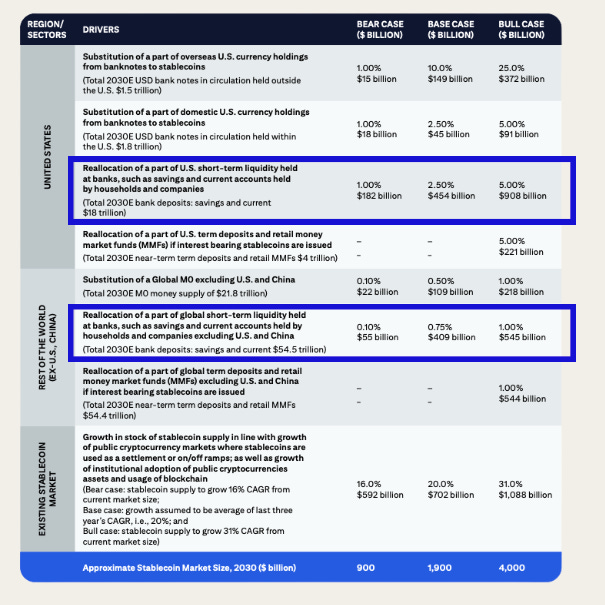

Stablecoins provide an advantage in two key areas regarding TradFi payment rails: cross-border and B2B.

For cross-border, correspondent banking and prefunding (storing idle funds in each of the geographic locations your business operates in) creates trapped liquidity in the range of $10-$27 trillion depending on the source. At minimum, stablecoin just-in-time payments via stablecoin orchestration platforms would add conservatively $400B in interest income ($10T × 4%; nostro and vostro accounts can earn yields, but if they do, it is often minimal) through money market funds alone.

The other area where stablecoins have a distinct advantage is B2B payments, especially B2B cross-border payments. Big companies with established banking relationships already have decent cross-border payment terms. However, smaller companies (SMBs/MSMEs), especially in LATAM, Africa, and Asia, stand to benefit a lot in cost and, crucially, speed savings. This, tied with stablecoin programmability that allows cash sweeping and automatic rebalancing (e.g., from cash to money market fund), will mean fintechs like Brex building on stablecoin rails will increasingly become the UI for small and medium-sized businesses.

Finally, an underappreciated trend is that traditional banks are touching less and less of the interchange (debit and credit card revenue share) revenue from stablecoin money movement, even if these happen on card payment rails. Stablecoin payment card providers like Rain are effectively sponsored by another fintech (Paymentology, their BIN sponsor). Traditional banks end up getting as little as 10% of the interchange fee.

For example a $100 transaction using the Rain card could look something like this:

Interchange Fee: $2.00 (2%).

Processor/BIN Sponsor (e.g., Paymentology): 20–40% → $0.40–$0.80.

Sponsoring Bank (if any): 10–30% → $0.20–$0.60.

Fintech (e.g., Rain): 0–20% → $0.00–$0.40 (or via separate markup).

Ultimately, Circle (or any other stablecoin) payment networks may not need to convert back to fiat, which means traditional banks also lose FX/processing fees. Visa has already debuted stablecoin settlement for merchants (Crypto.com, Worldpay, etc.). Simultaneously, payment service providers like Stripe have a) reduced the portion of fees traditional acquiring banks get from merchants and b) reduced the amount of funds that are held at traditional banks thanks to Stripe’s Stablecoin Financial Accounts.

So stablecoin providers are not coming just after traditional banks’ fees but also their deposits (see next section).

Where do we go from here?

Banks may try to buy or build orchestration fintechs once they sense sufficient product-market fit is reached

Banks may have to create their own stablecoins despite it not being in their best economic interest

Fees and margins will go down for cross-border transactions regardless of tech stack

Emerging markets retail customers and small/medium-sized businesses will be the main beneficiaries of these new payment rails

Privacy-preserving payments will emerge:

Infra level: Proprietary L1s (Tempo, Arc, etc.) and ZK L1s like Aleo (the first privacy-preserving stablecoin USAD was a partnership between Paxos and Aleo), or privacy-preserving Layer 2s like Payy.

Token level: Permissioned tokens like the Solana Token Extension and ERC-3643 standard

The Fight for Yield

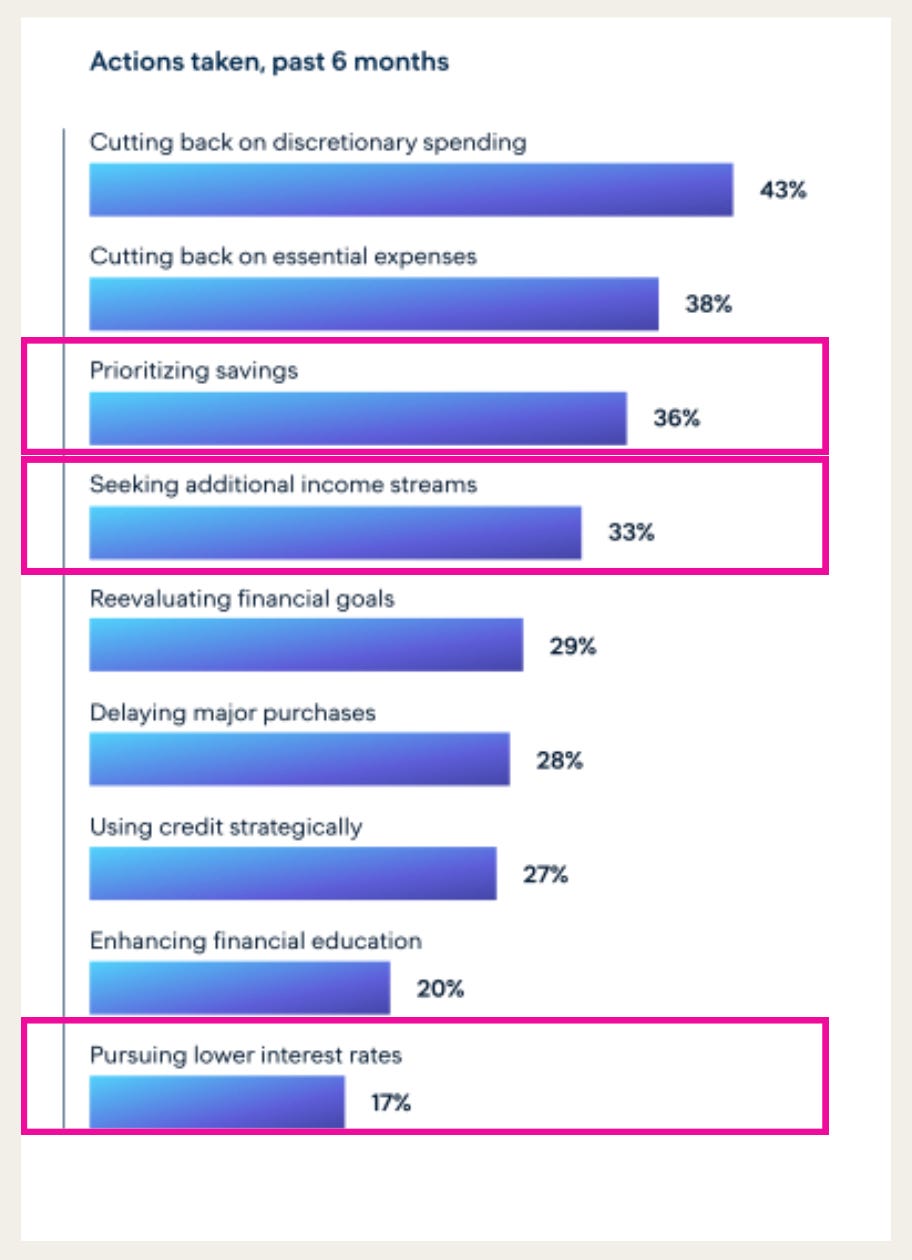

Not only are traditional financial institutions in danger of touching less of the payments flows, there is a non-trivial chance for deposit flight.

Citi’s base case (which I think is conservative) sees 2.5% (US) and 0.75% (excluding US and China), or $863B total deposits, fleeing from banks to stablecoins by 2030.

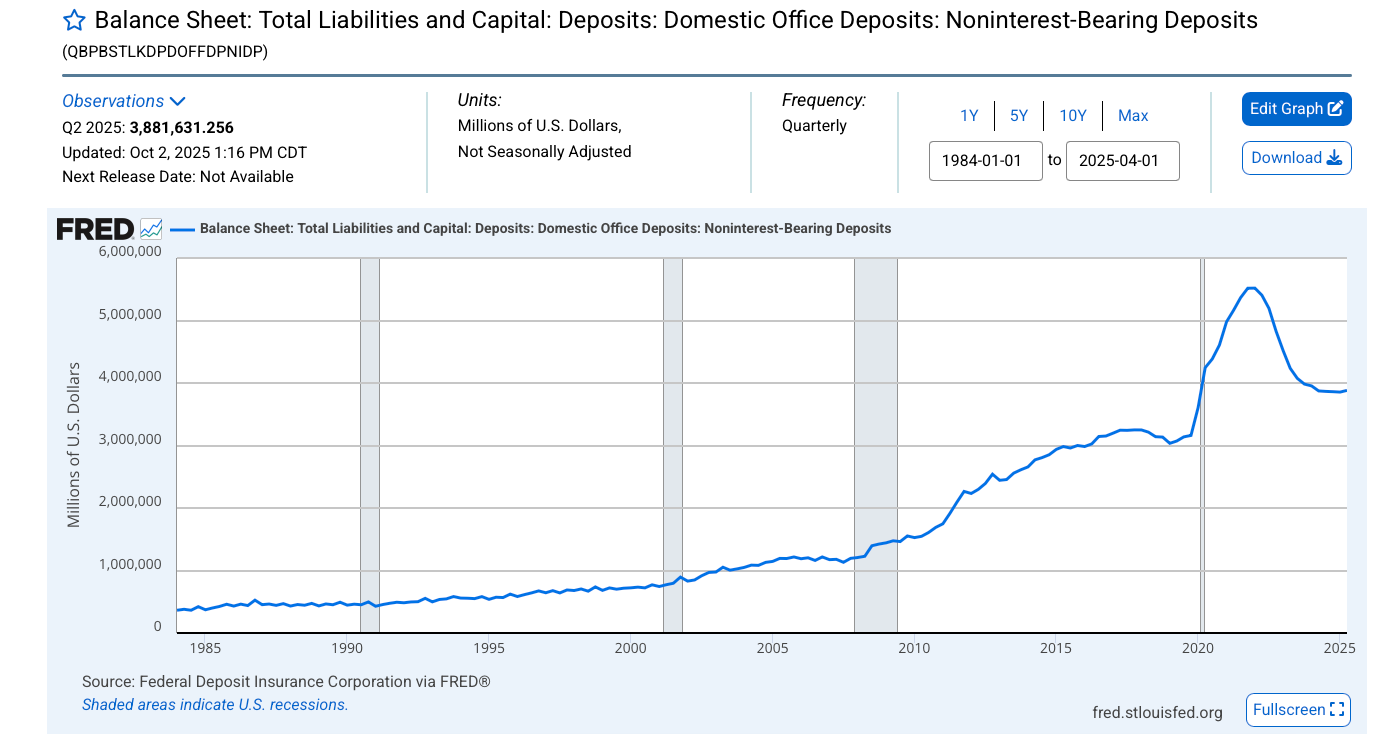

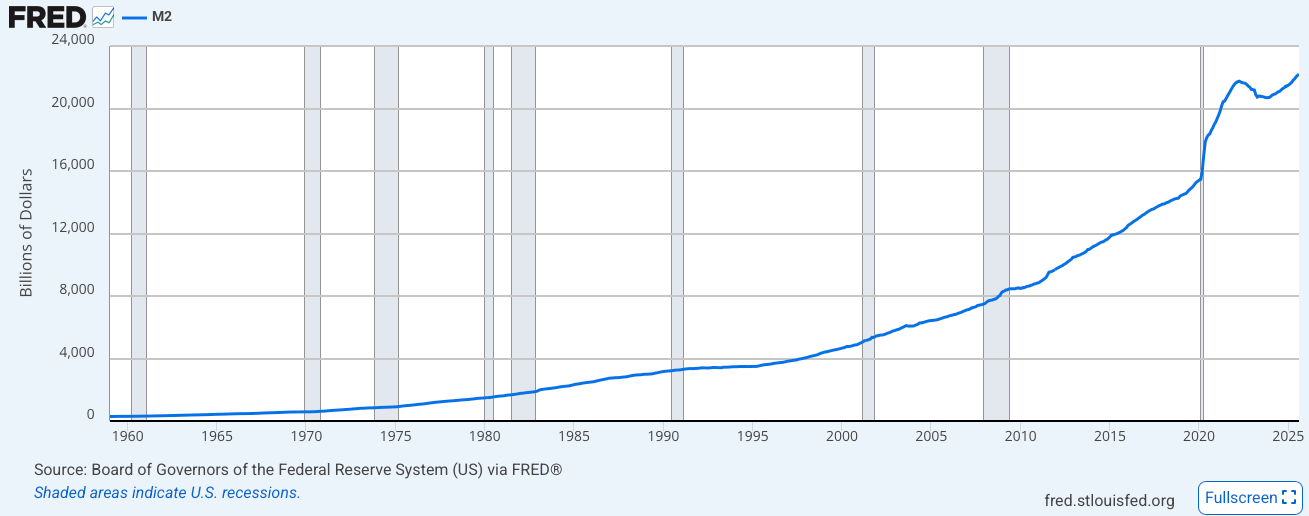

Why do I think Citi’s estimates are low? In the US alone, there’s almost $4 trillion in deposits that are accruing 0% interest while the money supply keeps growing, while retail customers are increasingly interacting with fintechs on the front end (digital banks and fintechs captured 44% of all new checking accounts opened in 2024).

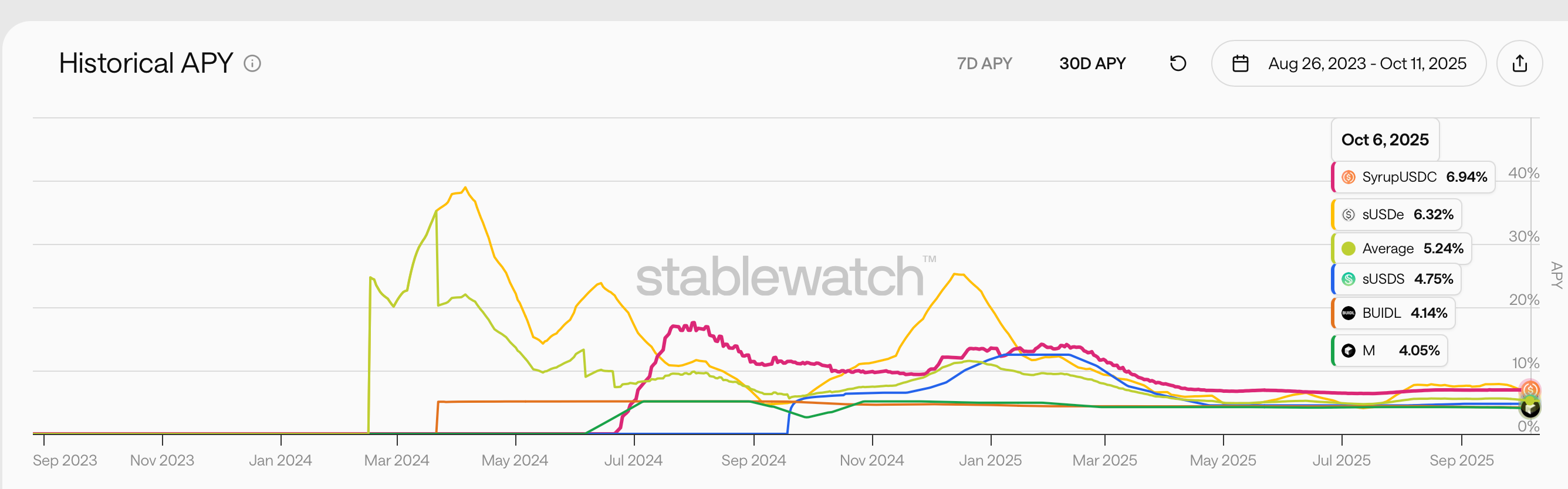

On the other hand, stablecoins give direct or indirect access to 4% yields. This yield is increasingly getting redistributed to the consumers.

On the yield front, I personally like to compartmentalize different stablecoins into three distinct buckets:

V1 → Yield to no one (Tether)

V2 → Yield to select group (USDC × Coinbase partnership)

V3 → Yield to everyone (USDe, M0, Agora, USDm distribute entire yield)

Even if reward distribution to end users is banned in the future, forward-looking fintechs can use those funds to subsidize customer experience, 0% fees, etc. Just like Tether, these fintechs don’t rely on transaction fees but on the size of the ecosystem (we’re already starting to see this with USDm and MegaETH). Crucially, this doesn’t just have to apply to blockchains subsidizing transactions but also regular fintechs (via the interest income on their own or consortium stablecoins).

Moreover, if DeFi is integrated thoughtfully, the 4% T-bill rate is just the minimum that users could get, which ultimately could differentiate Fintechs 2.0 from the Apples, Revoluts, and Robinhoods of the world, which already offer the 4% yield to their users.

Where do we go from here?

Higher yields through DeFi integrations → Coinbase already offers 11% yields to USDC holders via Morpho

Customer-facing AI yield agents → e.g., Mamo

Intent-based DeFi → e.g., Wayfinder AI

Back-end yield orchestration → e.g., Veda

Stablecoin yield subsidizing consumer-facing fees (FX, interest rates on credit, transactions, etc.)

New sources of yield

Delta-neutral trading strategies → Ethena was one of the pioneers here (instead of the limited and compressing T-bill yield of 4%, tokenizing yield from carry trade allowed them to secure a yield of 10% or more). Ethena imitators like Neutrl are entering the market. While 90% of Neutrl’s yields come from the Ethena-like carry trade, 10% come from getting assets at a discount via OTC deals.

Hardware-backed strategies → Now we see a new wave of stablecoins like USDai (yield from GPU hardware). It’s likely we’ll see a new wave of financial engineering (hopefully not as exotic as the Luna days) and riskier forms of funding stablecoins.

Growth of on-chain private credit → Access to on-chain private credit via players like Maple Finance (SyrupUSDC) and Grove (one of Sky’s Stars) gives higher yield opportunities.

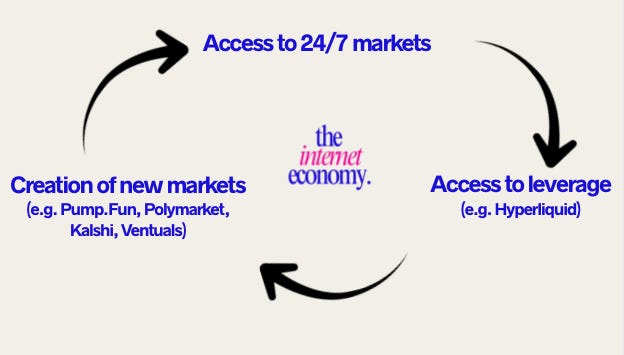

Hyperfinancialization: A threat and an opportunity

I think prediction markets are a great innovation. Not only do they give us more accurate predictions for outcomes, as we saw during the latest US election, which in turn can be used in financial markets for things like probability-weighted expected return and discount rates (hence the Polymarket-Bloomberg integration and recent ICE investment in the prediction markets platform).

I also think prediction markets could be a catastrophe for retail customers if not handled correctly. Uninformed retail can easily be taken advantage of by insiders.

I would classify this under three categories:

Access to 24/7 markets — DEXes and CEXes

Access to leverage — Hyperliquid, Lighter, Aster

Creation of new markets — Pump (memes and creators), Polymarket & Kalshi (outcomes), Ventuals (private company stocks)

So in summary, in the future we’ll have access to an ever-expanding range of 24/7 markets with infinite leverage (only slightly exaggerating).

(In fact, there’s an app on MegaETH called GTE that’s already trying to do this.)

Instead of competing for your attention, apps will now compete for your dollars (giving an alternative interpretation of the phrase “you are the product”).

The second-order effects of the hyperfinancialization of culture could especially hurt young, impressionable audiences. To avoid regulation in the future, we have to make crypto less zero-sum again. The key question is: how do we give fair access to the everyman and make markets less zero-sum? OTC deals, insider trading, and $10K trading bots are certainly antithetical to the values of crypto but persistent in TradFi markets as well. Proof-of-stake consensus mechanisms solved the incentive issue on the protocol level i.e., the incentives for selfish individuals to act unselfishly. It would do good if similar incentives could be applied to the app layer as well.

How Can Fintechs 2.0 Be Better?

Fintech 2.0s (built on blockchain rails) have five fundamental advantages over traditional financial institutions:

1. Better Economics for Consumers

Helping consumers save more through higher interest on deposits and cheaper fees. The wealth transfer from banks to consumers is real: instead of banks keeping all the yield from Treasury bills, stablecoins can pass that 4%+ directly to users.

2. Native DeFi Integration

Wallets (versus accounts) can directly plug into DeFi, expanding the in-app offering feature breadth and deployment speed that traditional rails can’t match. This means a fintech can add new yield sources, lending protocols, or trading pairs without years of regulatory approval and infrastructure buildout.

Access to delta-neutral strategies (Ethena), hardware-backed yields (USDai), and on-chain private credit (Maple Finance, Grove) that traditional banks simply cannot offer.

3. Revolutionary Credit Experience

Instant credit approval: The Rain stablecoin credit card is already becoming famous by offering instant credit by tokenizing and reselling its credit obligations. This opens up credit markets to the uncredited, although it does introduce some credit loss risks as well. As of 2025, there were only $500B in outstanding fintech-originated loans globally vs $18T in US household debt alone. That’s a massive gap, and tokenized credit is one of the tools that could help close it.

Self-repaying credit: Similar to Fluid’s self-repaying loans, I see the next evolution being self-repaying credit card interest (i.e., stablecoin yield repays credit card interest in real-time). Imagine your credit card balance earning yield that automatically pays down your interest charges.

4. Alignment with Younger Generations

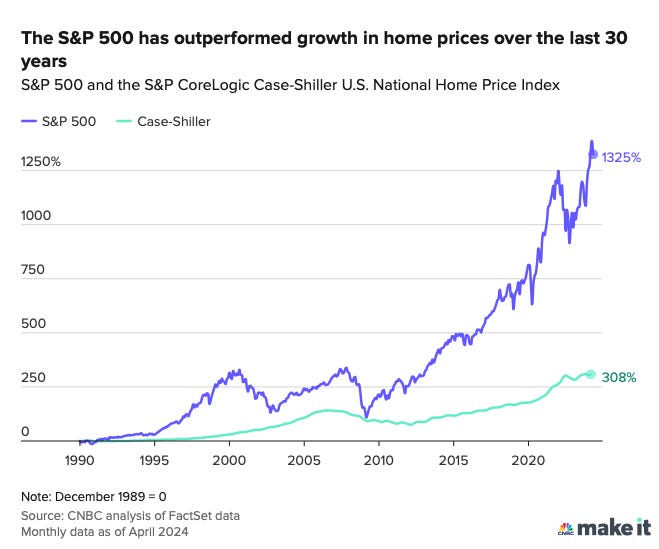

Arguably one of the remaining areas where traditional institutions are still beating fintechs is mortgages. However, mortgages are becoming less popular among younger generations, who instead prefer:

All-in-one-place access

Better yields

Social aspects

Access to crypto trading

And given how the S&P 500 vs. home price indexes have developed, who can blame them? Betting on stocks and not homes will surely continue to rise thanks to the AI boom.

What This Means: Three Waves of Disruption

Wave 1: Retail Flight

Superapp creation in the Western hemisphere just became that much easier thanks to stablecoin APIs.

This superapp could be the area of most promise in North America and Europe, where intra-regional money movement isn’t as big of an unlock for consumers as it is in emerging markets.

The building blocks are now available:

Stablecoin APIs (Bridge, BVNK) for payments and yield

Prediction market APIs (Polymarket, Kalshi) for everyday betting

Hyperliquid Builder Codes for immediate access to crypto trading

Whether this superapp comes bottom-up from Web3 wallets like Phantom, top-down from Fintech 1.0s like Revolut or Robinhood, or from entirely new players remains to be seen. All we know is the competition for control over the retail banking customer is increasingly in favor of fintechs.

Wave 2: SMB Flight

Small to mid-sized businesses (SMBs) have been famously underserved (and even remained unidentified) in part due to high servicing costs relative to returns by traditional banks, leaving room for fintechs like Revolut and Brex to swoop in.

Whereas before these fintechs relied on things like Visa APIs (e.g., Revolut’s famous multicurrency accounts), now they can plug into Bridge, BVNK, or other stablecoin orchestration APIs. The programmability of stablecoins also gives out-of-the-box treasury management capabilities like automatic cash sweeping, real-time FX, and yield optimization.

Traditional banks will have to join the race in providing better tools for their SMB client base or give up these underserved clients entirely.

Wave 3: Overall Deposit Flight

This is the existential threat to traditional banking.

The biggest advantage banks have is their cheap deposit base (they pay very little interest to depositors, often 0-0.5%, while earning 4%+ on those same deposits). Their entire business model depends on getting money for cheap and lending it out for more.

However, if depositors get access to the same end-yields banks do through stablecoins, there is real risk of deposit flight. This is why banks are lobbying against interest-bearing stablecoins it undermines their fundamental business model.

The Bottom Line

Fintech 2.0 unbundles the traditional banking value chain, redistributes the yield once captured by banks, and gives users direct access to financial primitives that were previously reserved for institutions. At the same time, it enables composable access to new markets through simple API integrations.

The question is no longer whether traditional banks will be disrupted, but how quickly they can adapt.

If you’re building in crypto or AI, feel free to reach out via Substack or LinkedIn.. I’d be happy to help you brainstorm ideas or connect you with potential investors.

Be at the forefront of the digital economy with the likes of UBS, H&M, FT, Solana Labs, Nike and many more. To receive new posts and support my work, consider becoming a free or paid subscriber.