Hidden DeFi Risks, DeFi’s Path Forward, and Why Stablecoin Cards May Lose

How on‑chain credit, stablecoins, and AI underwriting are reshaping (and failing to reshape) real‑world finance, from private credit and GPUs to neobanks and cards.

At the end of 2025, BlackRock TCP Capital wrote a $25 million loan to zero. Three months earlier, it had been valued at full par. The borrower was Infinite Commerce Holdings, an Amazon aggregator. The writedown, the second such wipeout in the same arm, contributed to a 19% NAV markdown across the fund. No gradual deterioration. No warning signal. A quarterly filing revealed the damage after the fact.

This is not a DeFi story. It happened entirely within traditional private credit, with all of its existing disclosure infrastructure. But it is exactly the right place to start, because it shows the gap between what blockchains promise and what we currently have: on a public ledger, the deterioration of that position could have been visible in real time, and today it is not. That gap between promised transparency and actual market structure is the thread that runs through everything that follows: DeFi, tokenization, stablecoins, and why distribution and yield still do not line up with the story we tell about “on-chain finance.”

I. What DeFi Actually Does

For those who still do not truly understand the topic: DeFi is a set of financial protocols running on public blockchains that allow anyone with a wallet to lend, borrow, and trade without a bank or broker in the middle. No account minimums. No compliance officer deciding who qualifies. Automated settlement on‑chain.

It has three functions worth taking seriously.

The first is democratizing access to capital markets. Anyone with a wallet can access and borrow via Aave, or create entirely new lending markets on Morpho without permission from anyone. Crypto‑native trading firms that get rejected by banks, not because of credit quality but because banks do not want sector exposure, can access global liquidity pools through platforms like Maple at rates between 6–12%, with collateral ratios of 120–170%. For borrowers that traditional credit will not touch, it is often the only option. Moreover, protocols like Fluid offer self‑repaying yield positions, USD.ai brings new collateral types on‑chain, and Gauntlet and Steakhouse run multi‑strategy vaults that automatically optimize across protocols. None of this infrastructure exists in traditional capital markets at anything close to this level of accessibility.

The second is creating more liquid capital markets. Thousands of participants lend from the same pool and redeem when they want. The yield‑bearing positions they hold, essentially IOUs, can be traded on secondary markets and used as collateral in other protocols. Capital becomes fungible in a way it simply is not in traditional capital markets, where many positions are illiquid, exits are slow, and each instrument is a bilateral negotiation.

The third is improving yield diversity. DeFi allows participants to explicitly choose their risk position within the same underlying asset, something that has no real parallel in traditional markets. Tranching lets you select fixed or variable yield. Looping, using your yield‑bearing position as collateral to borrow more, lets you increase leverage instantly. Ethena’s sUSDe basis trade packages the funding‑rate spread into a single instrument. The gold‑backed thUSD does the same for commodities. Ethena’s Strata product lets you select your yield tranche explicitly: senior, mezzanine, or junior, from the same underlying pool.

This is risk repackaging, not unlike what CDOs did in 2004. Pendle separates principal and yield into tradeable tokens. Stablecoins span a spectrum from T‑bill‑backed USDC to private‑credit‑backed syrupUSDC. Looping adds explicit leverage. Instead of three tranches, we now have tens of instruments representing different positions on the same risk curve.

The promise was that this time it would be different from 2008. Instead of having to be Michael Burry, manually excavating prospectuses to find what was inside a mortgage-backed security, any wallet holder could verify the composition of their position in real time. The yield repackaging and the transparency were supposed to arrive together.

The yield repackaging arrived. The transparency has not (yet).

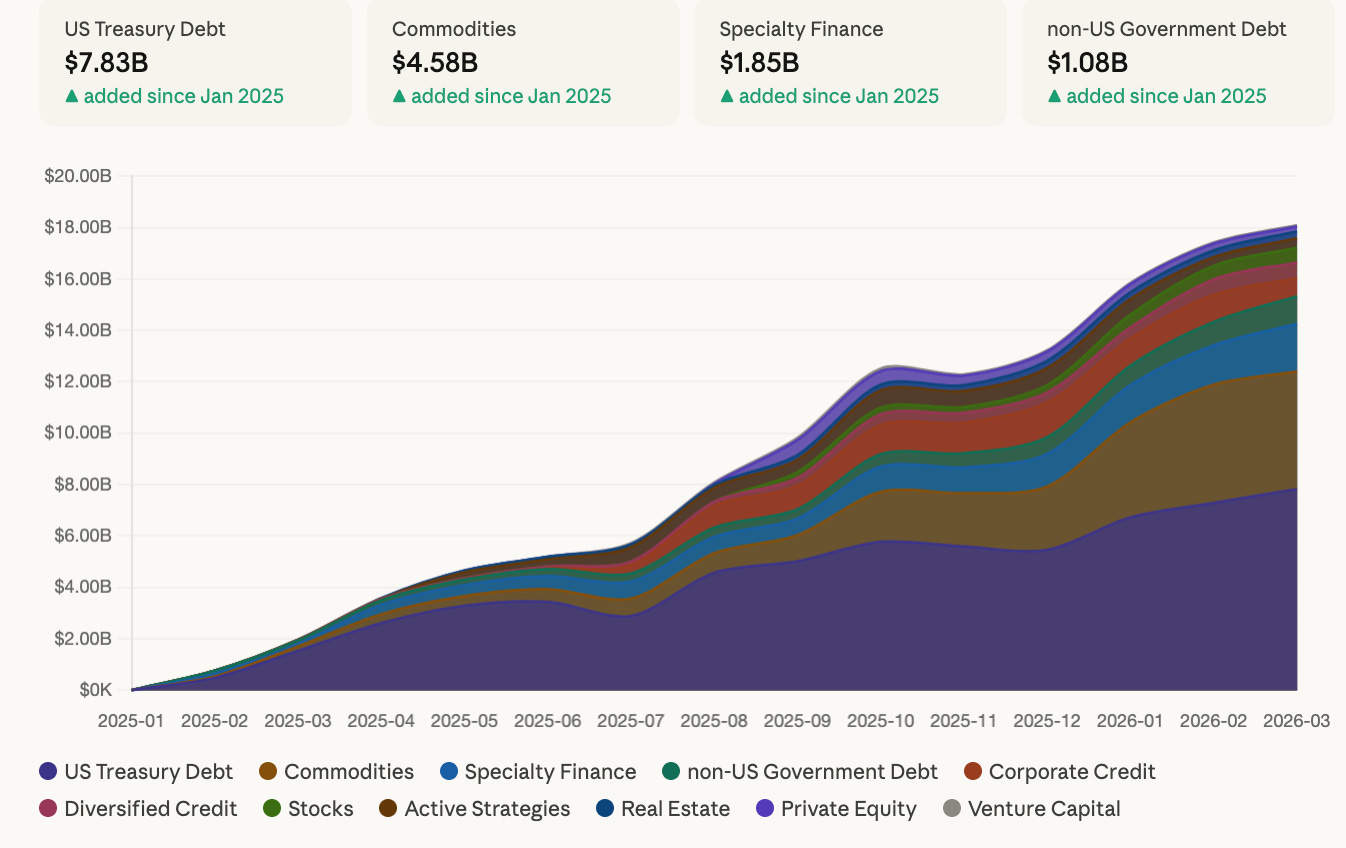

II. What Is Being Tokenized?

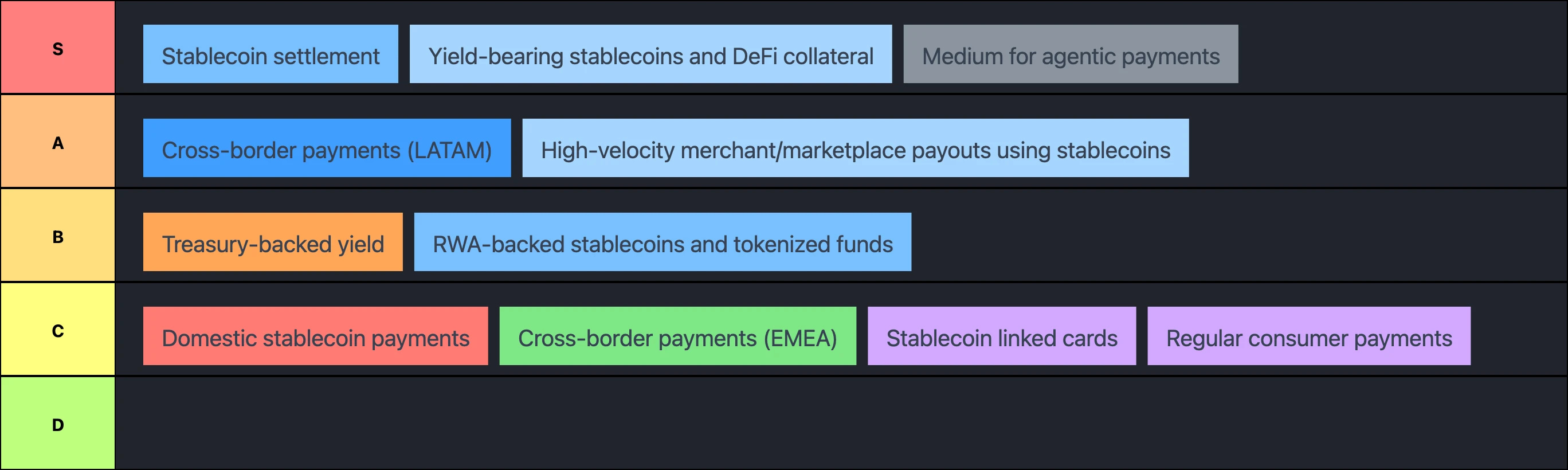

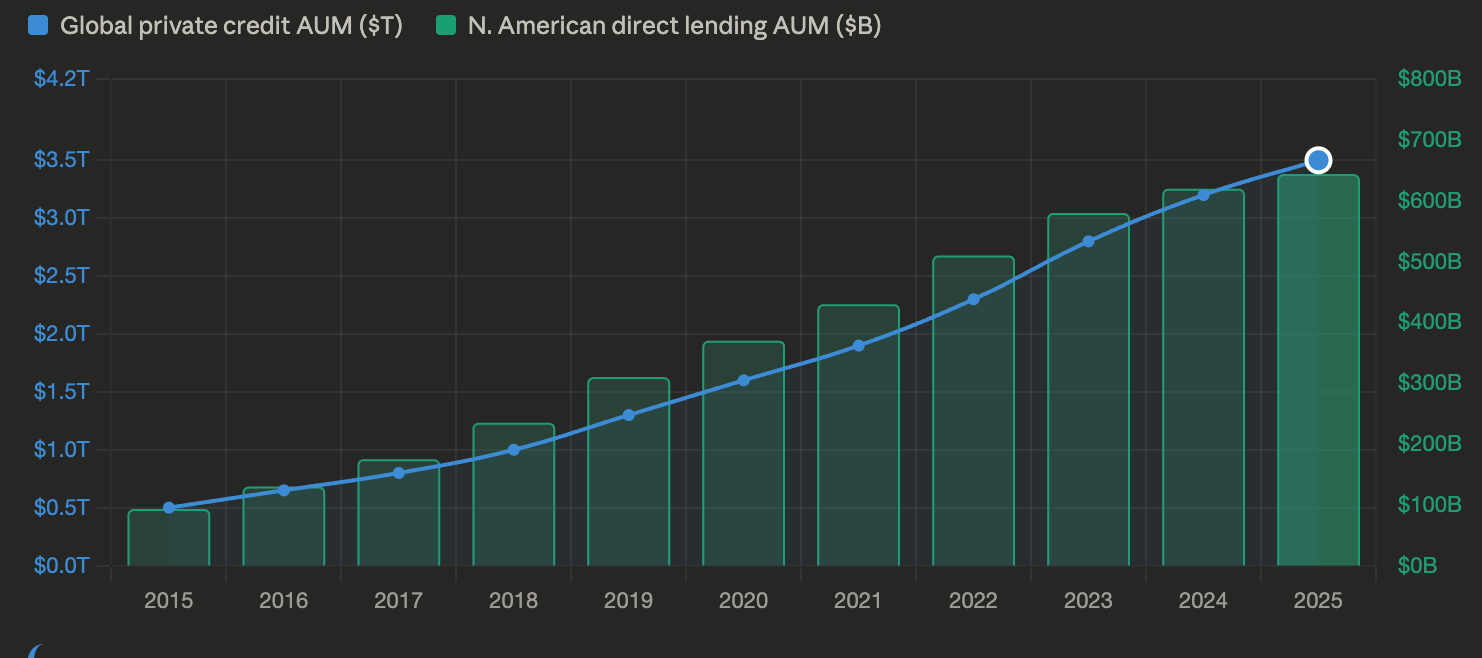

Capital flowing into tokenized assets has settled into a clear hierarchy since 2025. US Treasury debt has added the most in absolute terms, given the yield and safety. Commodities have added billions of dollars, driven almost entirely by renewed institutional interest in gold. The fastest‑growing segments in percentage terms, however, are corporate credit and diversified credit like Figure’s HELOC product, Apollo’s ACRED, and Arca’s Stable Return fund.

One distinction matters enormously and gets glossed over in almost every conversation about tokenization: some of these assets are represented on‑chain, not originated there. Figure’s HELOC (a tokenized home‑equity line of credit) is only represented on‑chain, but you can still use it as collateral on Kamino. The underlying capital‑markets infrastructure (the underwriting, legal enforceability, and servicing) remains off‑chain and centralized. The blockchain is functioning as a ledger, not a lending system.

III. The DeFi and Stablecoin Distribution Problem

A DeFi lending protocol’s economics are a function of four variables:

AUM × collateralization rate × utilization × borrow fees + establishment fees on new loans.

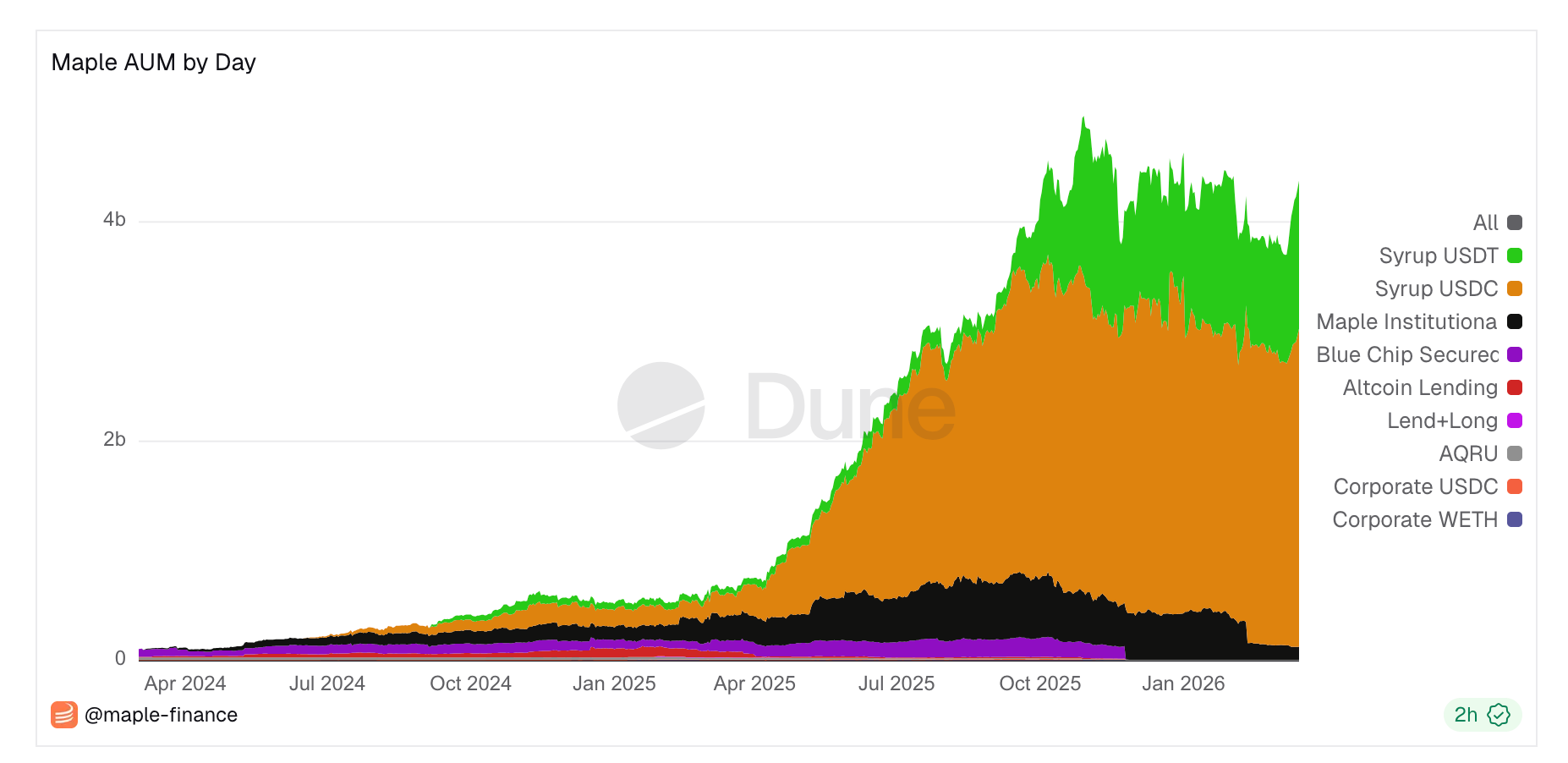

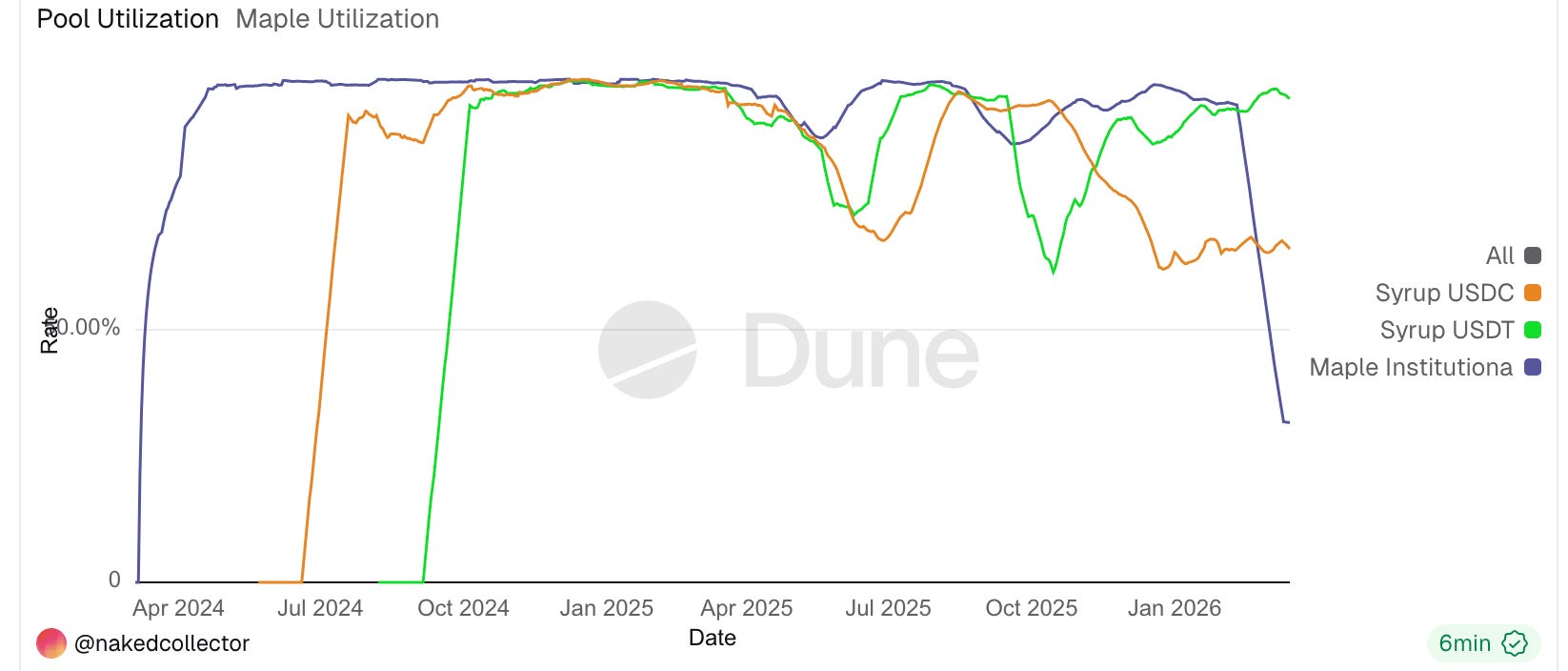

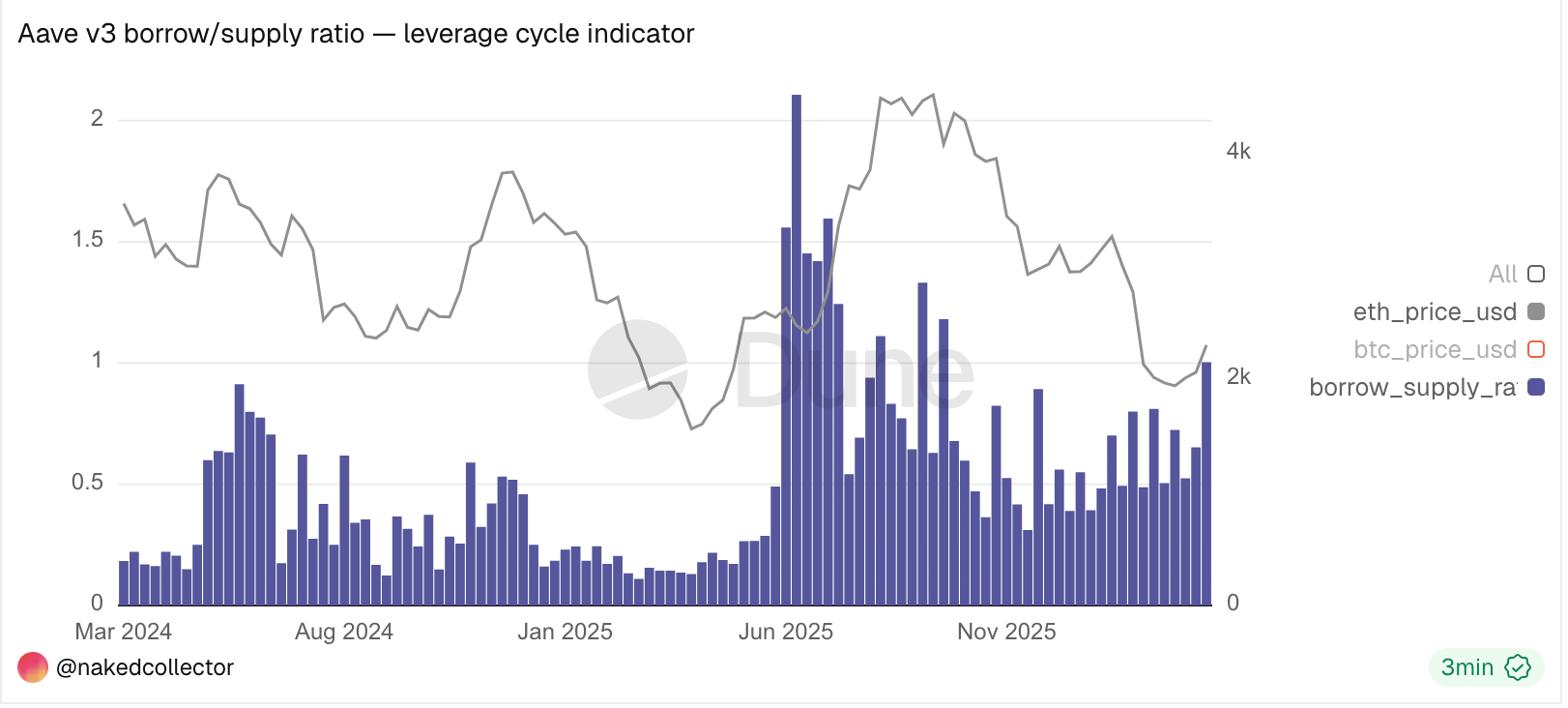

The lever that most directly determines health is utilization. And utilization is falling or plateauing even as headline AUM grows.

As retail and crypto‑native demand for borrowing gets tapped out, the next frontier is TradFi institutions. However, there are issues with this.

Maple’s data makes this visible. Total AUM has grown significantly, driven by syrupUSDC expanding rapidly into retail, but institutional pools have been relatively flat as a share of the whole. syrupUSDC’s AUM reached around $3 billion in 2025 with lower utilization than smaller, more specialized pools, while other syrup products frequently operated near full deployment. In other words, AUM growth driven by retail deposits has not been matched by institutional borrower demand.

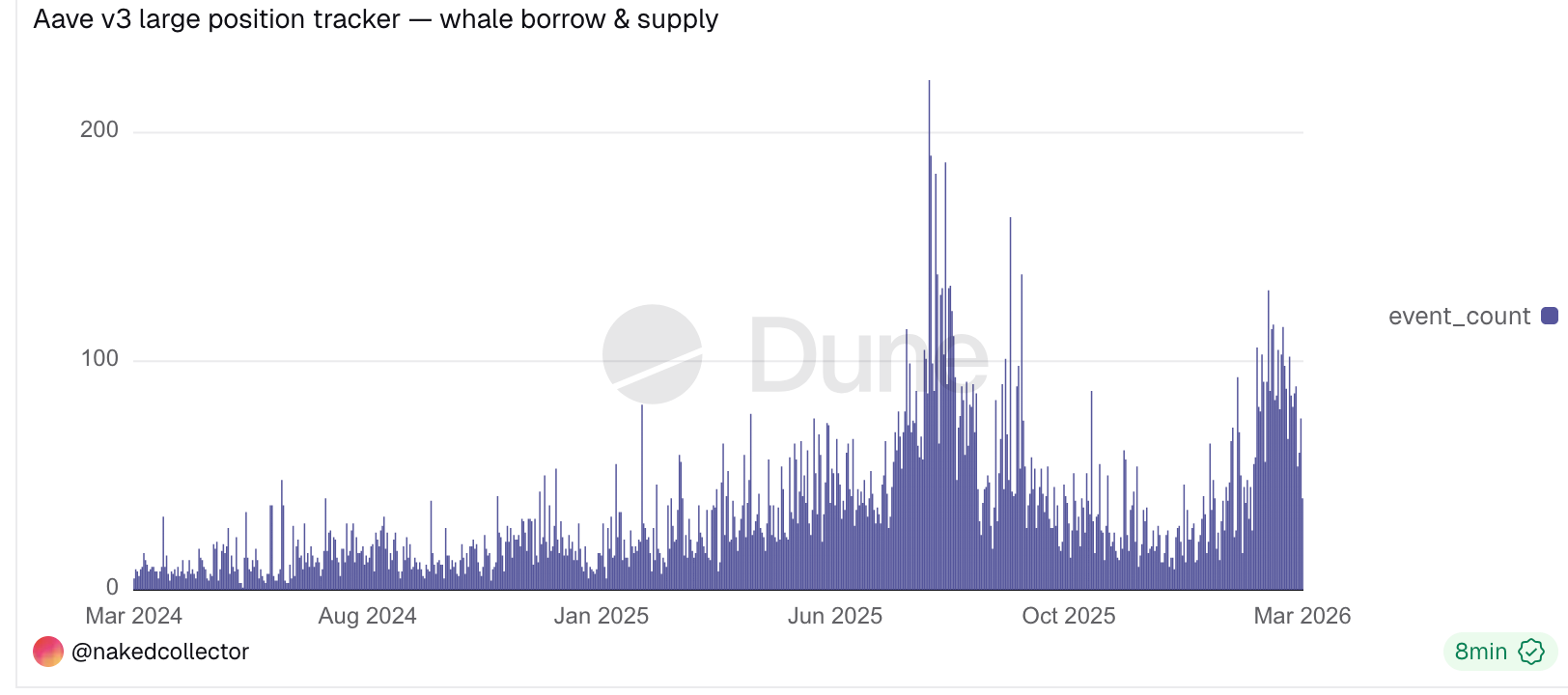

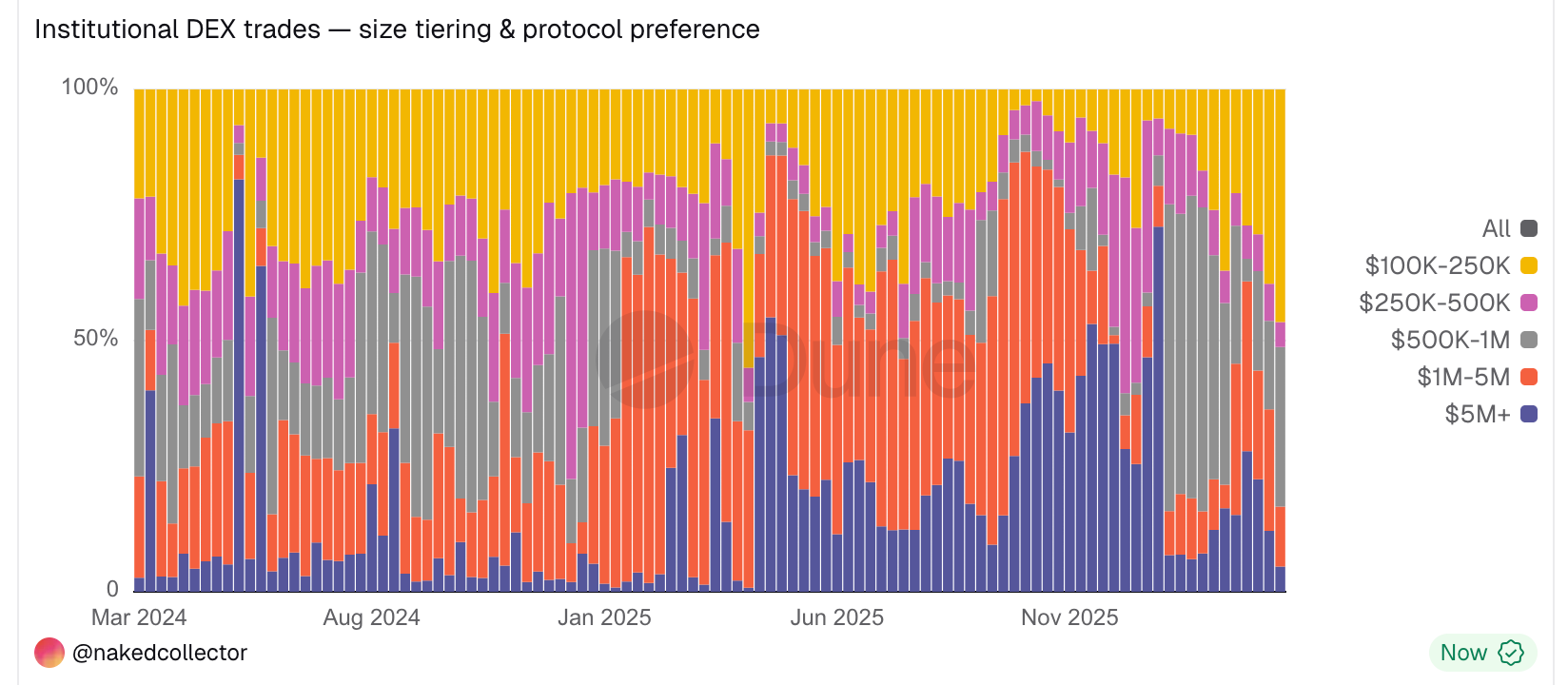

Miners no longer want to borrow at scale. Large funds and family offices no longer need to, because there may be better risk‑return opportunities elsewhere. We see a similar trend in Aave’s institutional borrowing platform, Aave Horizon, where large on‑chain positions and DEX trade data confirm that institutional borrowing demand is no longer growing as it once did.

For this reason, DeFi protocols are in a search for marginal demand from borrowers who are less tied to crypto cycles. Protocols are turning to neo‑finance companies, bank partnerships, and private‑credit originators to fill this gap.

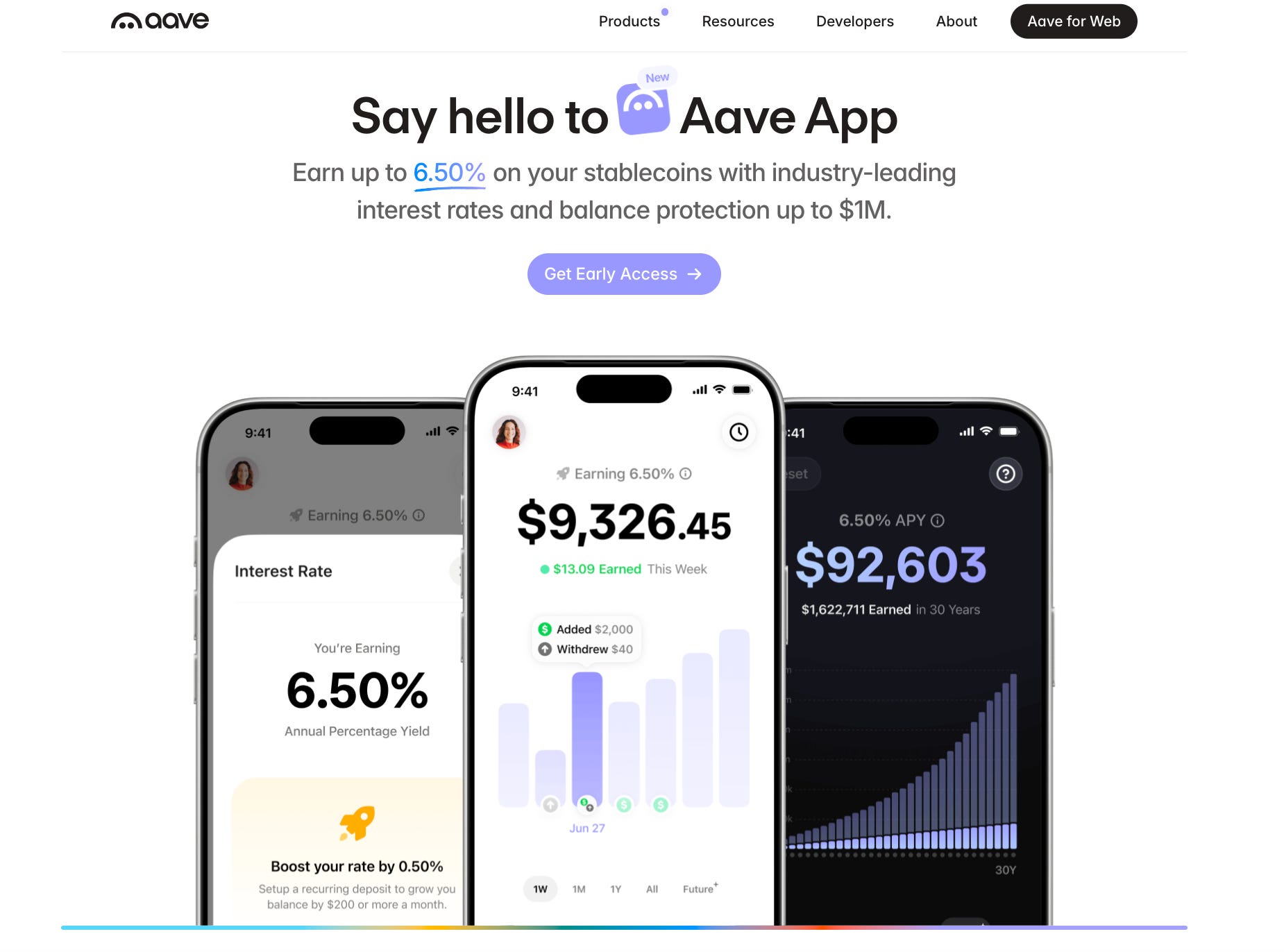

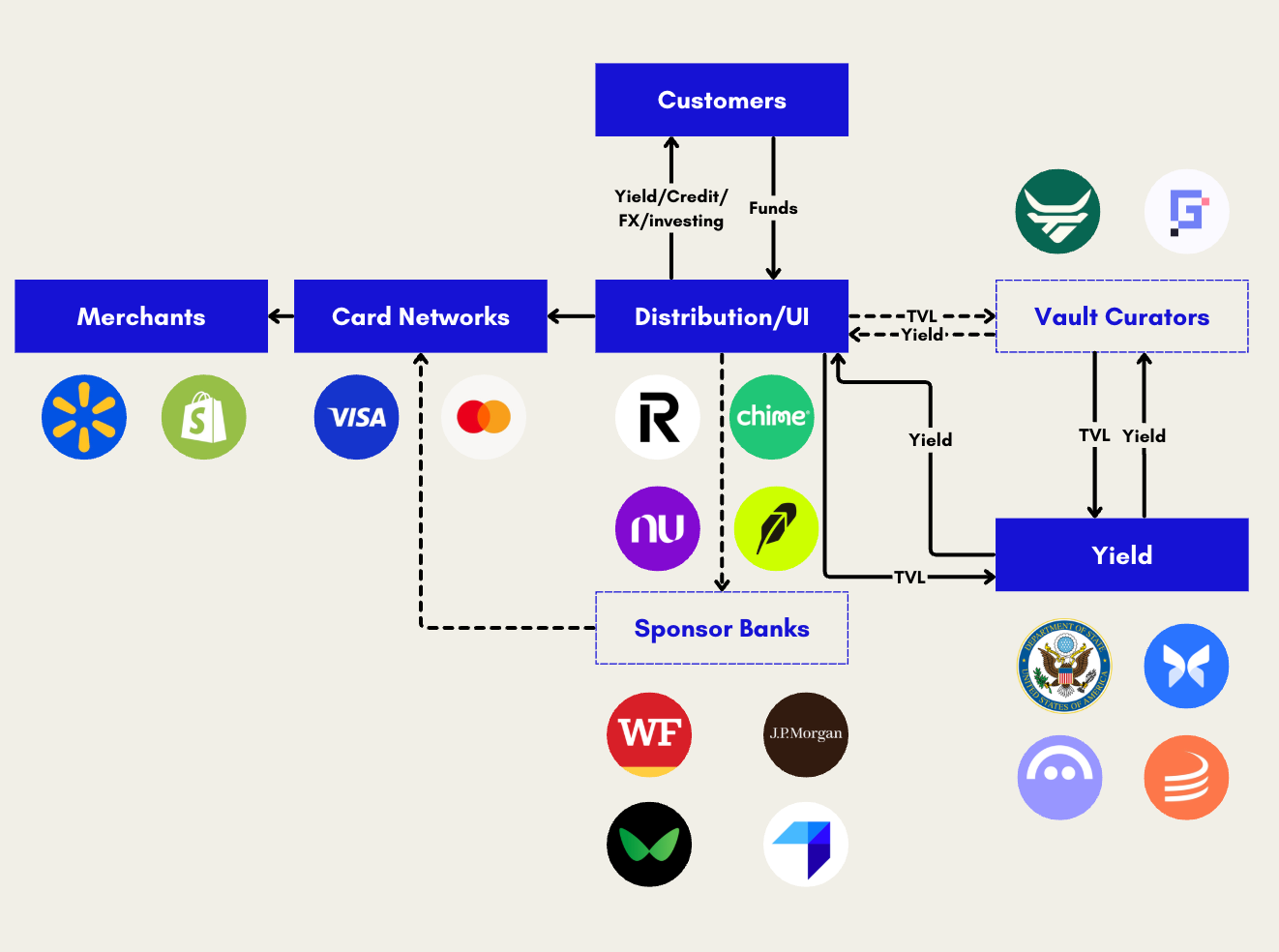

But reaching those borrowers requires consumer distribution infrastructure, and that is precisely what DeFi has never built. Aave has wound down several consumer‑facing products and is currently trying again with Aave App, which it is clearly pushing on its homepage over its prosumer DeFi dashboard.

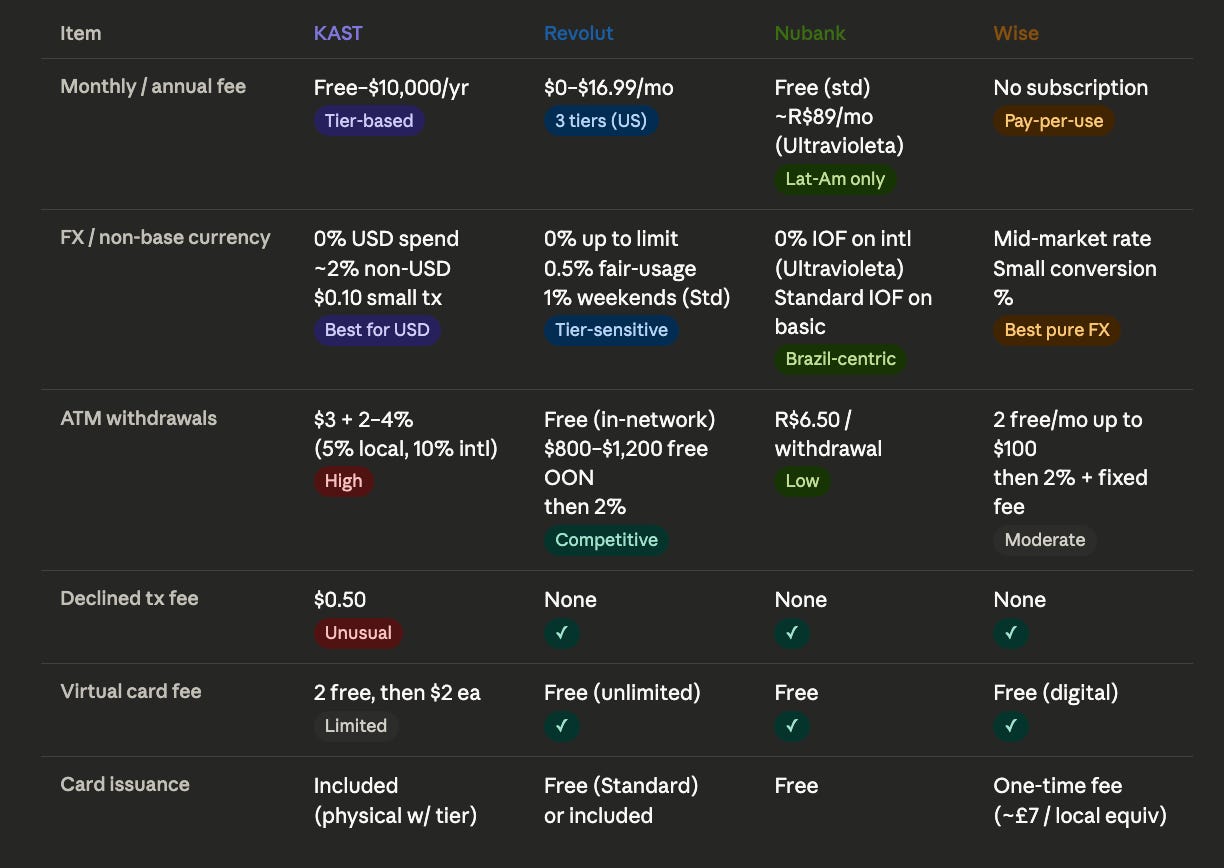

This is also the reason why crypto credit cards have been all the rage among many DeFi (and other) protocols, including Ether.fi, Coinbase, MetaMask, 1inch, and Plasma. However, this does not solve the distribution issue; it has become more like table stakes than meaningful innovation. Crypto payment cards are not a new idea and have seen only limited adoption. The biggest beneficiary is Visa and sponsor banks, not the new stablecoin neobanks.

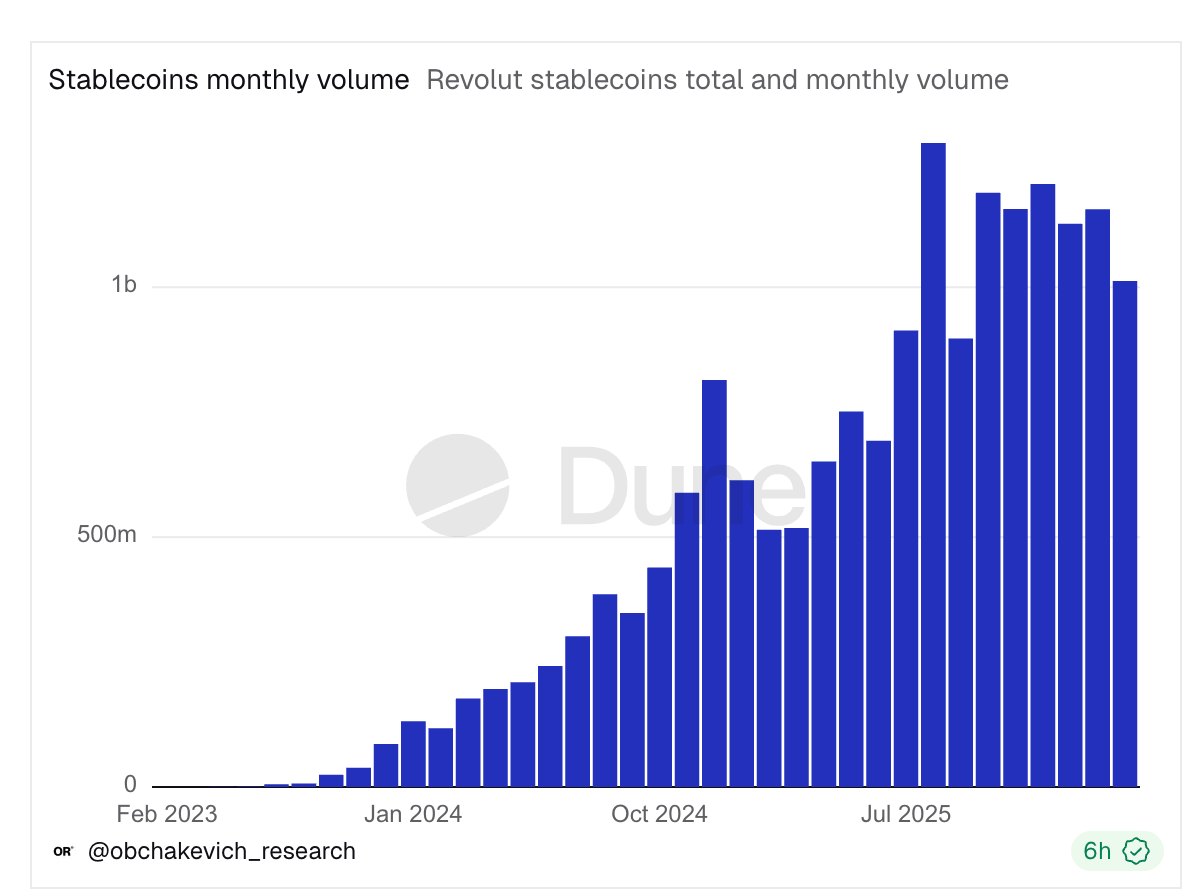

While there are debit/credit card reward nerds who compare card rewards, they are few and far between. Moreover, these cards are not likely to outcompete modern neobanks like Revolut, even with slightly higher APYs. Revolut already shares around 4% APYs with its card users and can negotiate strong packages for its users: free subscriptions to things like the Financial Times, Perplexity Pro, and NordVPN, zero FX fees, robo‑advisors, and sophisticated business‑card software. It has processed over $10 billion in stablecoin volume, versus KAST’s roughly $5 billion annualized.

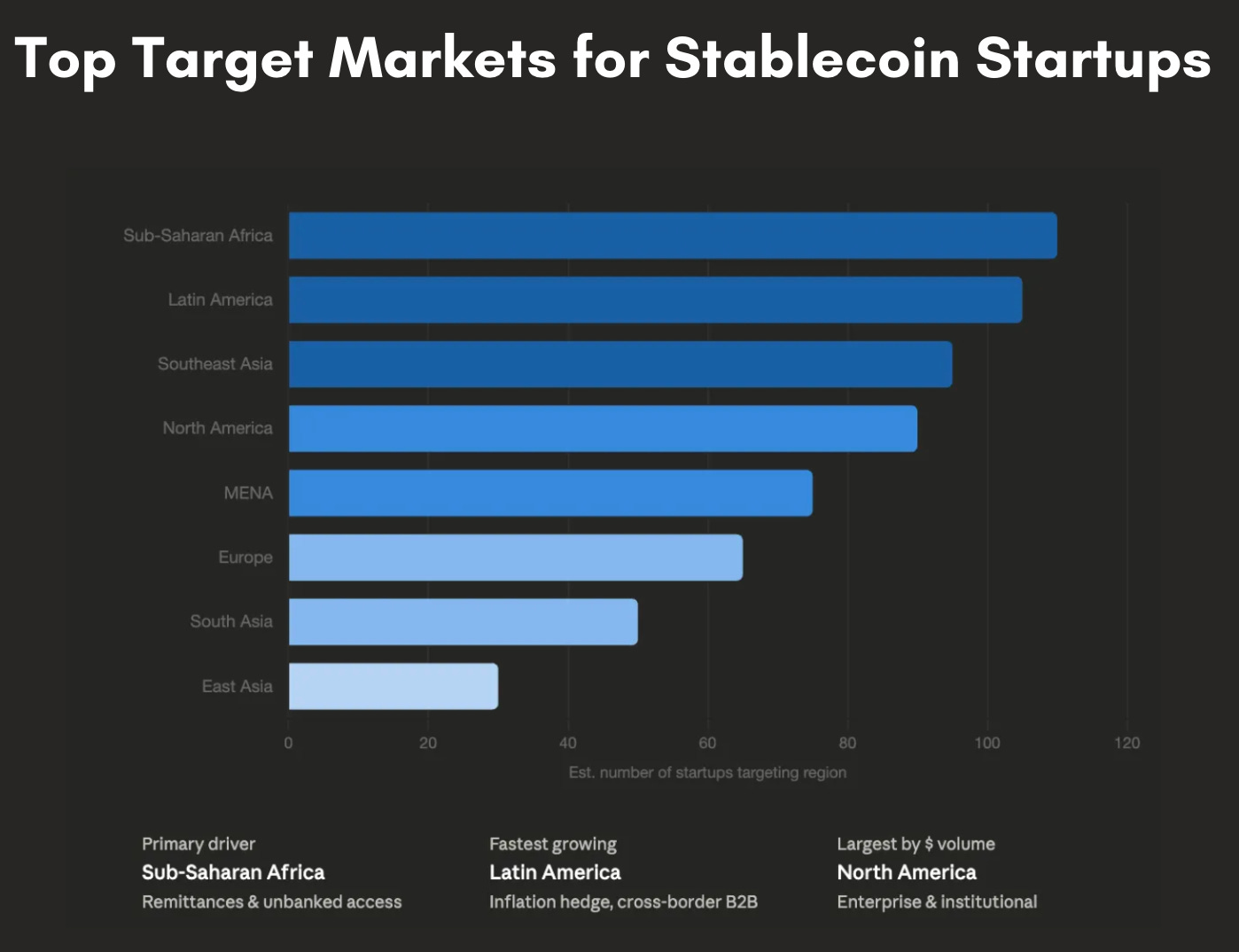

The point is that without becoming an all‑in‑one app, having a card will not meaningfully increase deposits, outside a limited set of reward hackers. This is why, while most stablecoin startups are founded in the US or Europe, players like KAST and Tether are all looking primarily to the Global South. Not only do they not have to compete with entrenched neobanks to the same degree (though Nubank is an exception, and Revolut has made inroads into Mexico, Colombia, Argentina, and South Africa), they also do not have to compete with relatively well‑functioning domestic payment schemes in Europe and the US, where it is not obvious that stablecoins win on speed and cost.

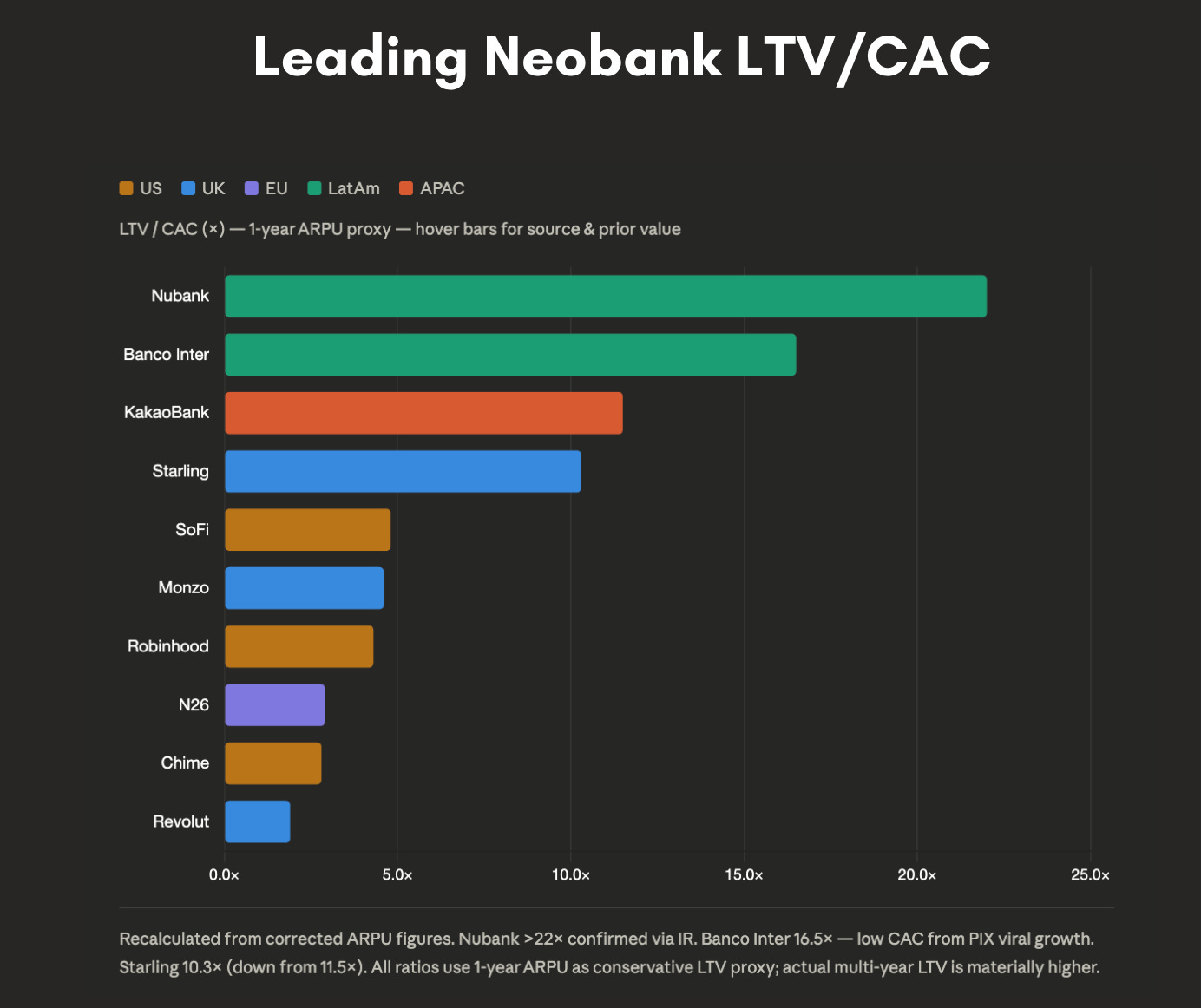

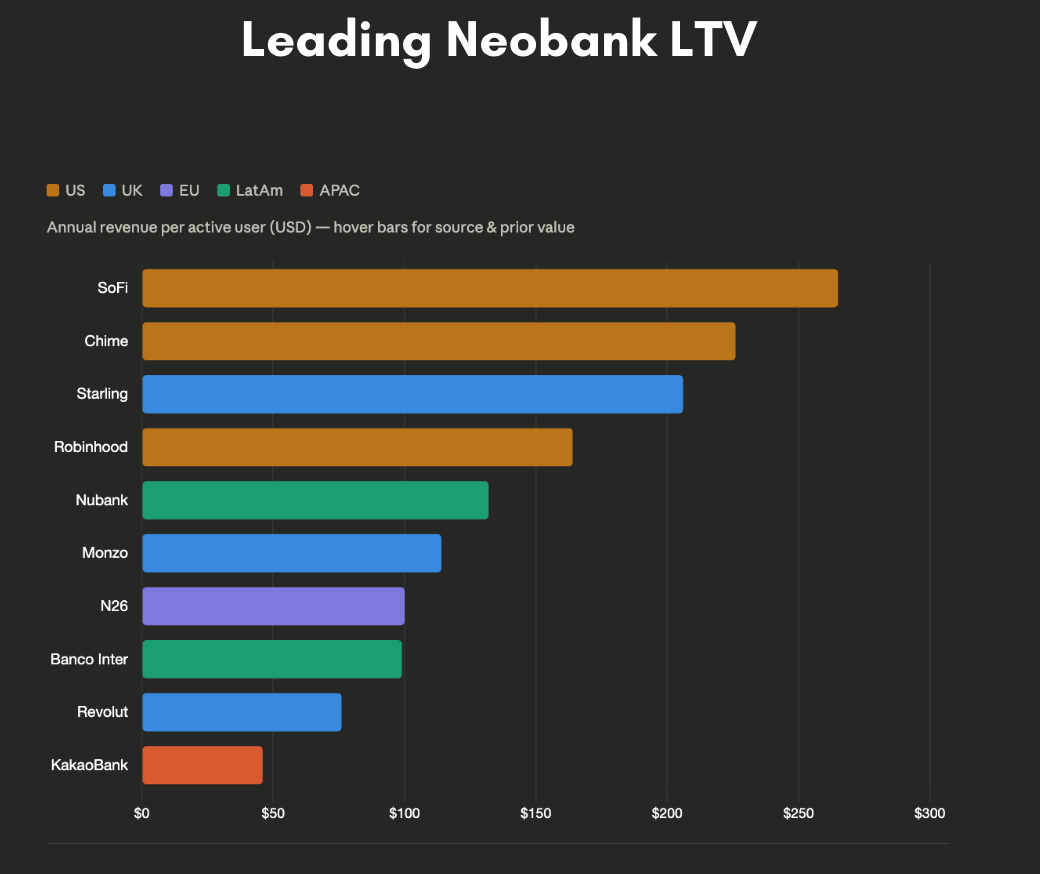

The Nubank Cinderella story is appealing. Its LTV/CAC is roughly 10x that of Revolut, driven largely by much lower customer acquisition costs. It holds around 58% of LATAM neobank customers but likely generates 80–85% of the region’s neobank revenue. In places like LATAM, the high LTV/CAC ratio is driven by low CAC rather than unusually high LTV.

This poses two questions for stablecoin companies entering the region: (a) how much more in CAC will it cost to pry customers away from Nubank, and (b) if several stablecoin companies start going after LATAM clients, how much will CAC rise?

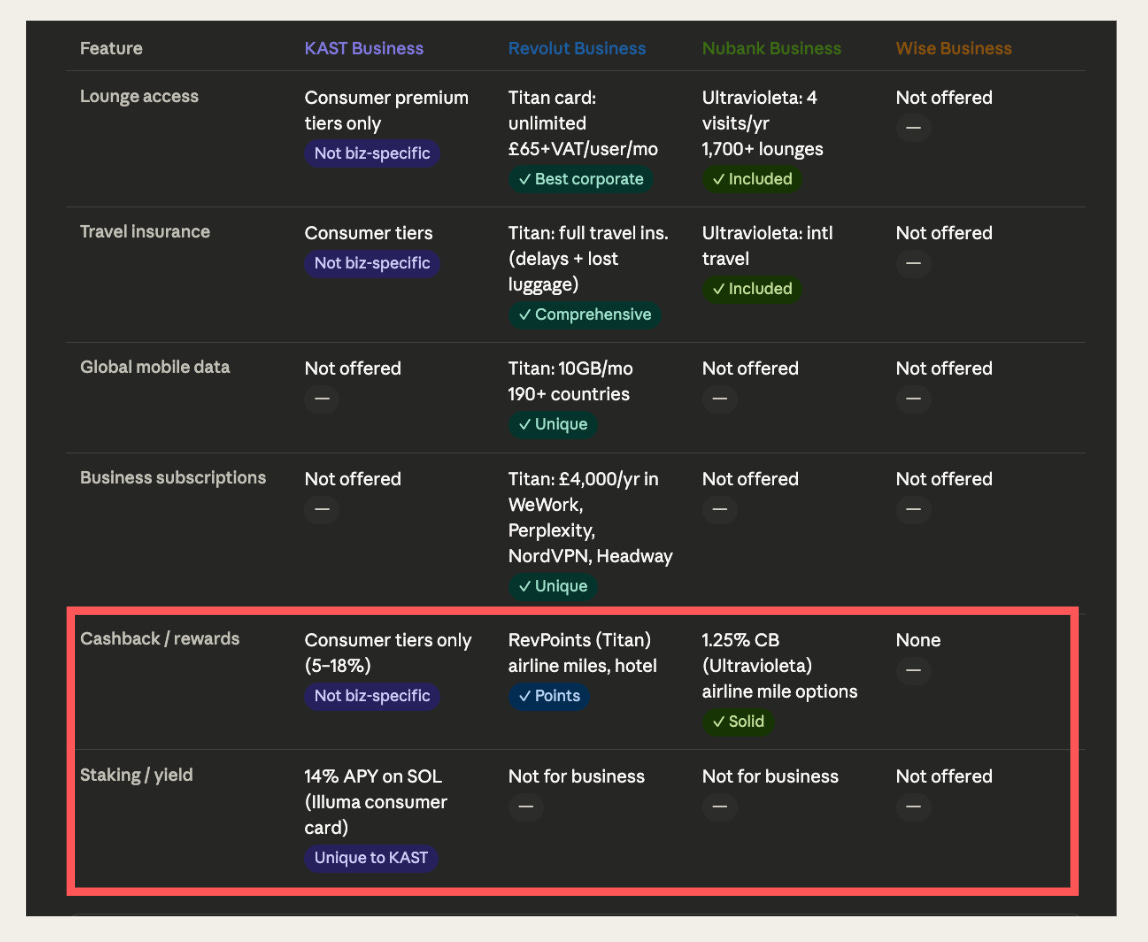

The beauty of DeFi for these entrenched neobanks (as opposed to stablecoin startups) is that curators like Gauntlet and Steakhouse make it simple for them to earn the same yields that stablecoin cards like KAST use. Down the line they could even spin up their own Morpho vault, pass on 100% of the yield to customers, and treat it as a loss leader. Taking a cut of such services (including yield) is a key revenue strategy for stablecoin startups or networks like Plasma, while incumbents can undercut those fees. It is not inconceivable that entire blockchains, like Tempo, could act as loss leaders to Stripe. Chris Dixon (cdixon) has long argued that stablecoins and stablecoin transactions will become public goods, which is plausible.

Moreover, incumbent payment cards are objectively better products than stablecoin ones and likely have better margins, because they spend less on brand recognition and have banking licenses.

So if incumbents have better distribution and lower marketing costs, more mature ecosystems of services, and decent yield, how can stablecoin startups compete?

The realistic differentiators are:

Easier off‑ramps for crypto traders and investors (but competition is catching up).

Slightly higher yield via DeFi and token incentives (though token rewards are speculative, and most stablecoin card issuers do not even have a token yet).

Higher cashback.

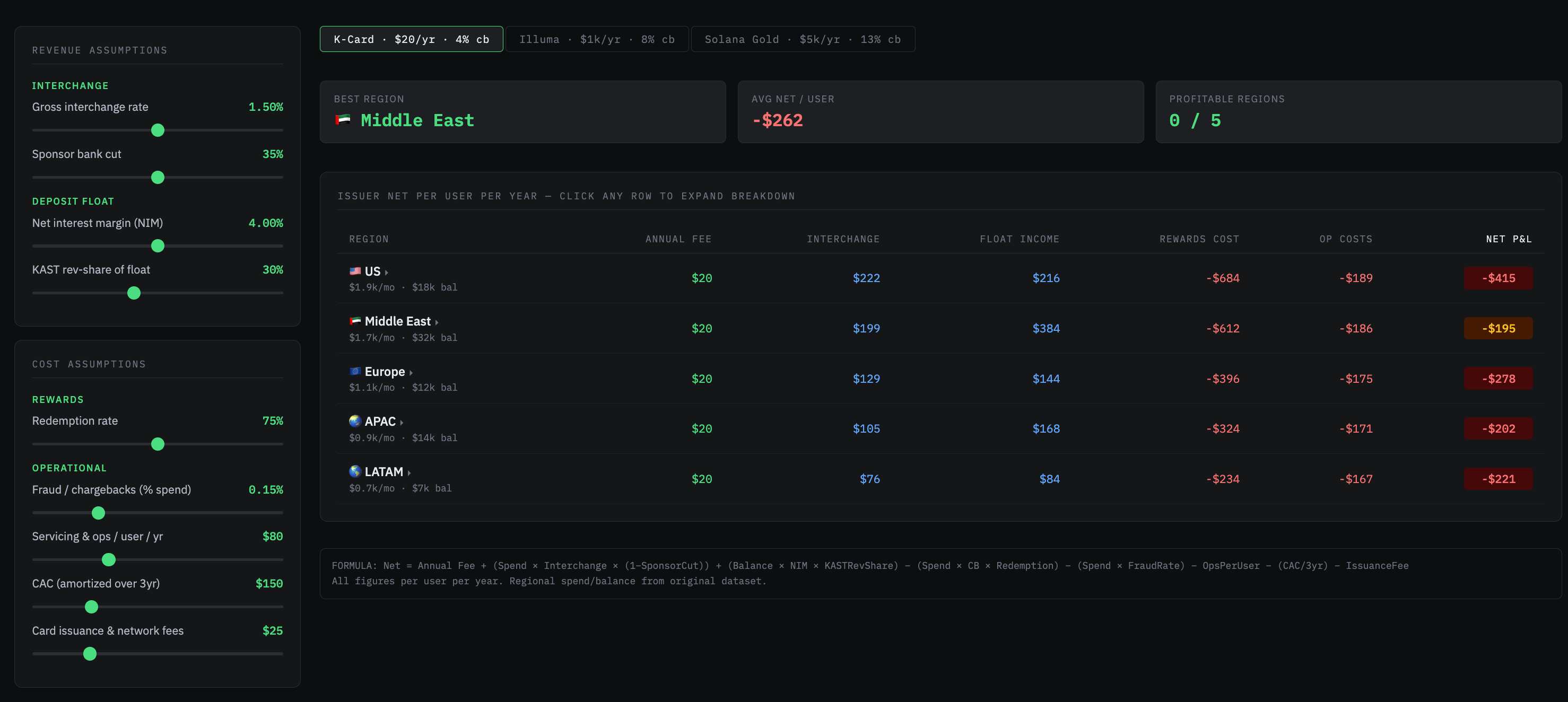

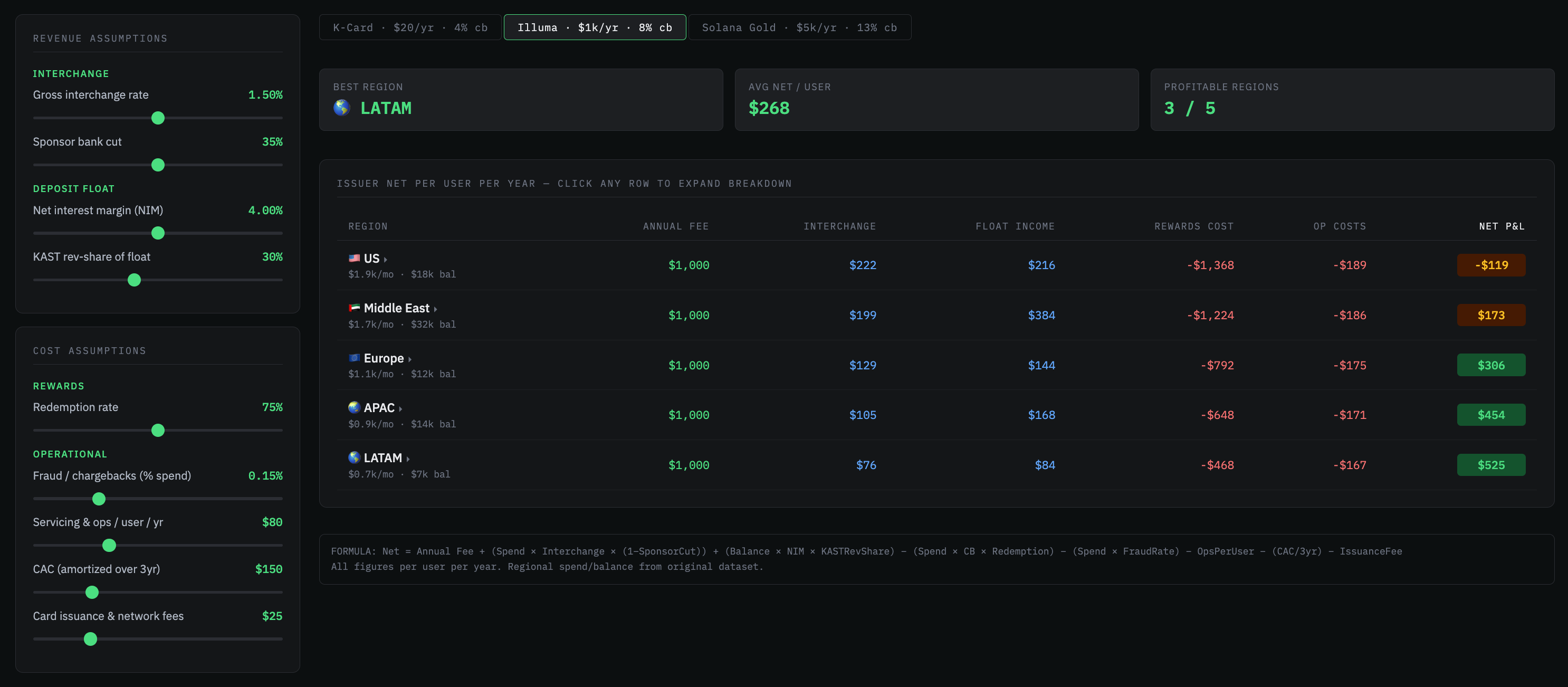

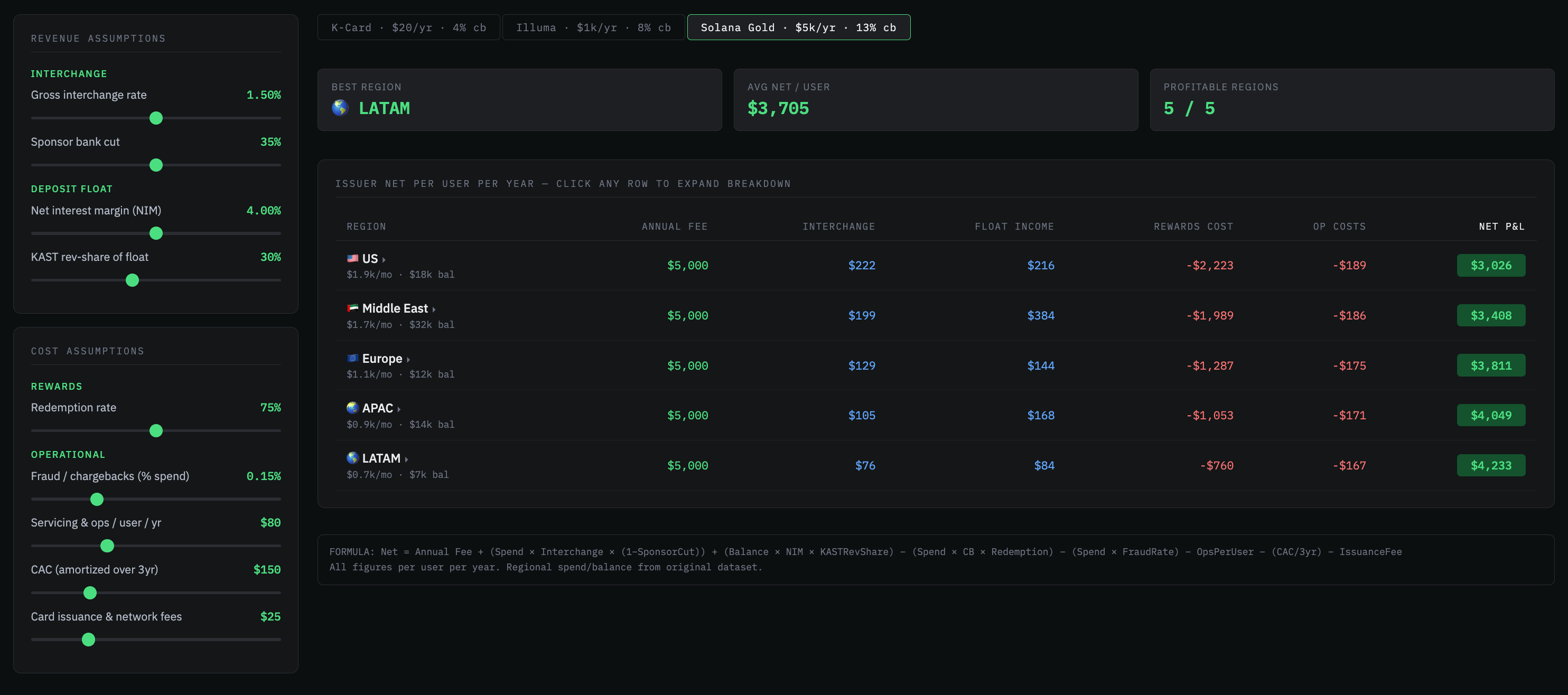

Delving deeper into KAST’s unit economics, KAST makes money in three main ways:

Capturing a portion of KAST Earn yield (undisclosed cut).

Taking 1–2% interchange fees (outside Europe), of which 20–50% go to its sponsor bank; by contrast, Revolut, N26, and Monzo have banking licenses and keep this spread.

Charging miscellaneous fees like FX and declined‑transaction fees (both unusual for neobanks).

Modeled (below) across its three cards (entry, mid, and high end), with optimistic assumptions, the takeaways are:

To maximize profit per cardholder, KAST would want users to deposit a lot and spend less; cashback is a loss leader when it exceeds net interchange.

To maintain profitability, KAST is incentivized to withhold as much yield as possible, which pushes it down the risk curve if it still wants to beat neobank yields.

Higher‑tier cards are more profitable; the entry‑level K‑Card is effectively a loss leader.

LATAM and APAC are the most profitable regions for KAST.

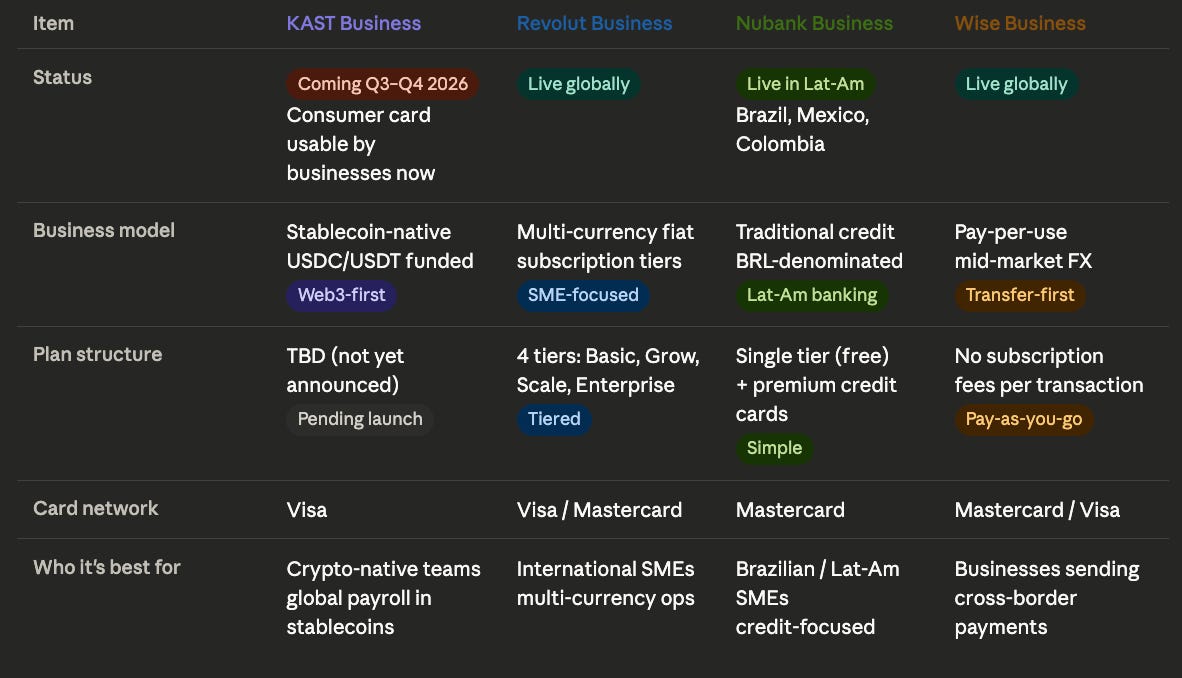

Unlike incumbents, KAST also does not have business or credit cards, the highest‑LTV product categories. Around 85% of Nubank’s revenue comes from credit products.

To offer credit cards in Latin America, KAST would need banking‑level licenses per country, substantial capital, and enhanced risk systems, beyond its current fintech/sponsor‑bank model.

The once‑strong moats are dwindling as well. DeFi yields may get competed away as incumbent banks plug into curator vaults, and DeFi yield has always been downstream of one thing: on‑chain trading activity. Ethena’s basis trade depends on funding rates produced by leveraged traders. Borrowing demand at Aave and Maple correlates directly with how much trading is happening. When trading volume is high and volatile, the whole system runs. When it drops, every yield source downstream feels it.

Crypto on‑off‑ramping’s oligopoly is being attacked from both directions. From the crypto‑native side there is increased competition from MetaMask, Coinbase, Ether.fi, and Phantom. From the incumbent neobank side we see names like Robinhood and Revolut; competition is becoming saturated.

Higher fees work when you are the only game in town serving high‑net‑worth crypto investors and traders in wealthy geographies; once you go to the Global South and face economies of scale, this no longer works. Economies of scale matter for Visa transaction fees too. KAST likely has higher fees than its larger competitors due to lower volumes.

Crypto remains structurally important, but stablecoin players whose only value add is crypto on/off ramps will not succeed in the long term.

The only ways they can succeed are:

Giving away generous token incentives while somehow avoiding a collapse in token price, which history suggests is unlikely to be sustainable.

Offering genuinely differentiated APY from more exotic asset pools or income streams (sequencing fees, MEV, niche strategies), instead of simple USDC yield that is accessible to anyone. Here, vertical integration is more competitive than horizontal aggregation. Think Maple offering unique APY only to its cardholders, or a future Pump.Fun card allocating cashback directly to daily memecoin runners instead of paying out in depreciating dollars. Next‑generation stablecoin payment startups will likely offer APY sourced from venues like Hyperliquid, HIP‑3, and Polymarket trading strategies.

This naturally pushes them down the risk curve and toward outcomes like Stream or Goldfinch, where private‑credit risk and operational risk combine in ways that are hard to see until something breaks.

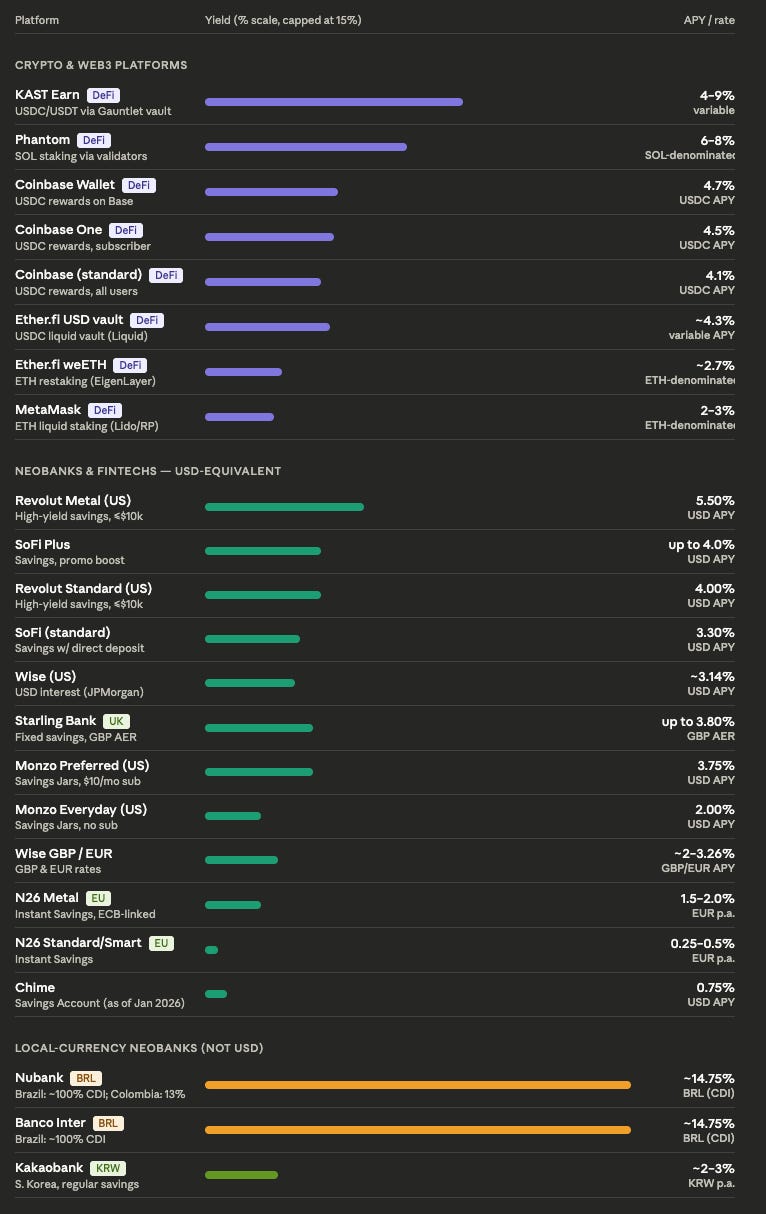

The bottom line is that yield is the decisive commodity, whether it is for DeFi protocols, DeFi curators, stablecoin payment cards, or bank savings accounts. DeFi protocols like Maple and Aave will live and die by the APY rates they can sustainably offer. Morpho seems more impervious as a pure platform where DeFi natives and Wall Street veterans can spin up custom pools, though it too will suffer if DeFi yields fail to materialize.

It is no surprise that financial institutions like Apollo are starting to wrap their tentacles around Morpho. It is plausible that Apollo will one day launch on‑chain private‑credit pools that are genuinely on‑chain rather than just represented there.

Ultimately there are two paths DeFi protocols and stablecoin platforms can choose: (1) trying to become a superapp, hoping that category‑invention benefits outweigh the distribution handicap (Aave, KAST, Phantom), or (2) becoming the middleware layer and hoping incumbents do not circumvent you (Morpho, Rain, Gauntlet).

IV. New Yield Categories

With AI and prediction markets funneling speculative capital away from leveraged crypto trading, it is clear DeFi needs to expand its sources of yield.

Private credit and other alternative markets (like GPU‑backed loans) are good steps in that direction. The more DeFi touches the “real” economy, the more sustainable it will be in the long run

Private credit is one of the fastest‑growing yield categories in DeFi. It offers higher yields: Maple’s current USDC APY is around 4.2% versus Aave’s 2%. Someone might note that 4.2% APY on what is essentially private credit versus 4.3% Treasury yields is a horrendous risk‑return trade, which it is. However, there are a few factors that make the future of on‑chain private credit potentially exciting: (a) democratization of access, (b) composability (use as collateral for loans and trading plus the ability to increase leverage via looping), and (c) capital formation for an underserved market.

I have covered a) and b) extensively before, however, capital formation for an underserved market is an interesting opportunity as well.

Skeptics would posit that private credit is currently a “borrower’s market,” with credit spreads tightening, a rise of covenant‑lite structures, and increased PIK usage. This means there is no rush for decent‑quality businesses to apply for loans sourced on‑chain if they can go to Apollo or a bank on similar terms.

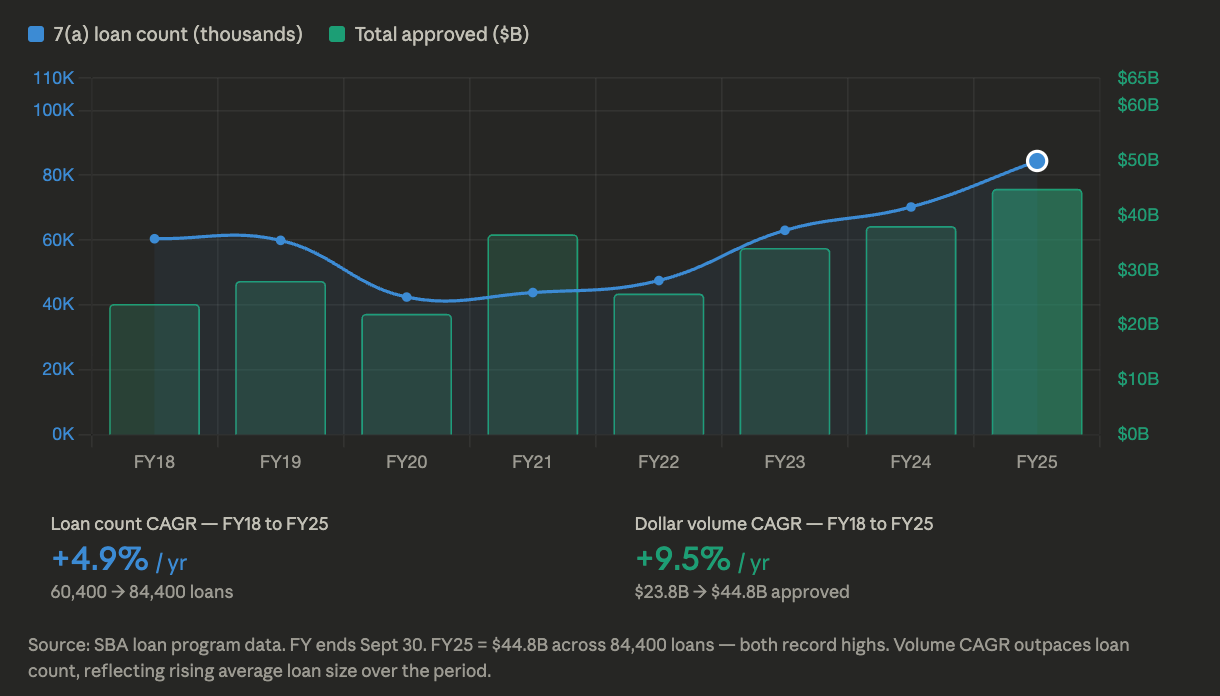

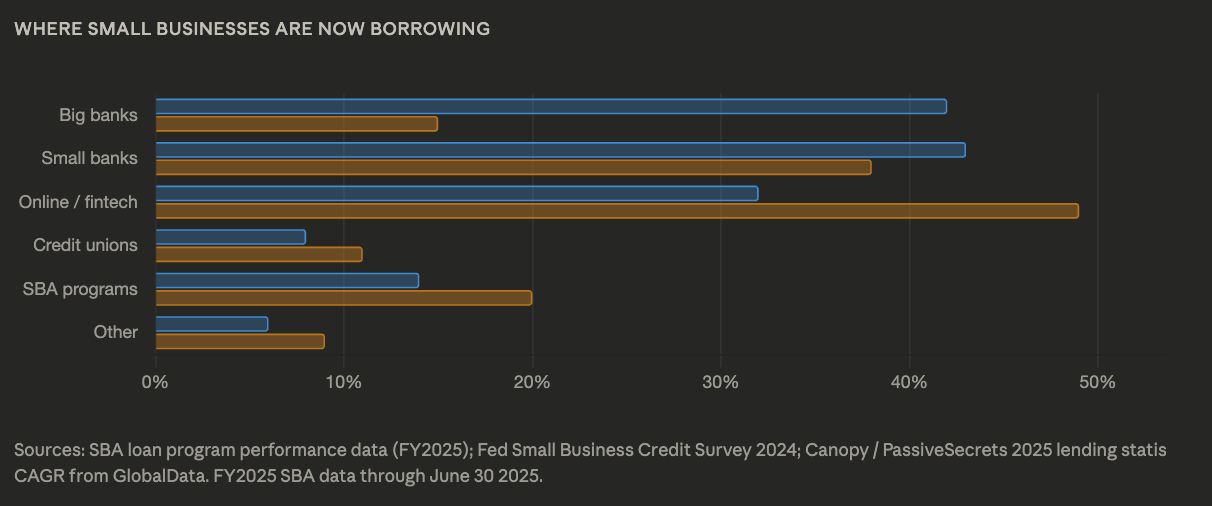

However, there seems to be a gap in the small‑business loans market. In 2024, only around 15% of small‑business loan applications were approved by banks, and roughly 44% of small businesses did not even apply for these loans.

Hence, small businesses are increasingly shifting to fintech players. Ease of use, higher approval rates, and speed are some of the reasons.

This is where Maple and other private‑credit operators should and can play. For instance, USD.ai found a completely underserved market in GPU‑backed loans for emerging AI companies. Whether GPUs make for good collateral is a separate question, but USD.ai has made tens of millions of dollars in loans to dozens of counterparties. Peanuts in the grand scheme of things, but an interesting proof of concept.

Crypto has always served and created infrastructure for “outsiders.” In its current iteration, this means a user could be onboarded in Africa via a stablecoin wallet and then contribute directly to GPU‑backed loans in Silicon Valley, sidestepping Wall Street and the traditional financial system completely.

While trading has been the golden goose of crypto thus far, these “real economy” applications are more exciting. In the former, value concentrates from the many to the few; in the latter, it can be distributed from many to many.

However, for private credit to scale on DeFi rails, the operational math is challenging. Rough calculations suggest a firm needs 20–50 staff per 100 loans annually, capping these firms at roughly $1–5 billion AUM. Maple, for instance, currently has around 50 staff and approximately $4–4.5 billion AUM, implying a practical limit of about 100 loans per year. In other words, CeFi (centralized finance) does not scale in the same way that DeFi or even stablecoins do. However, there might be a solution closer than you think.

V. Transparency Gap in DeFi

While DeFi’s biggest advantage is its transparency, it still has a way to go.

Fully on‑chain DeFi arguably has great transparency (with some exceptions), but things break down when there is an off‑chain component in the flow. Overall, while DeFi was supposed to solve the transparency issue that would prevent another 2008‑type financial collapse, it has not yet done so.

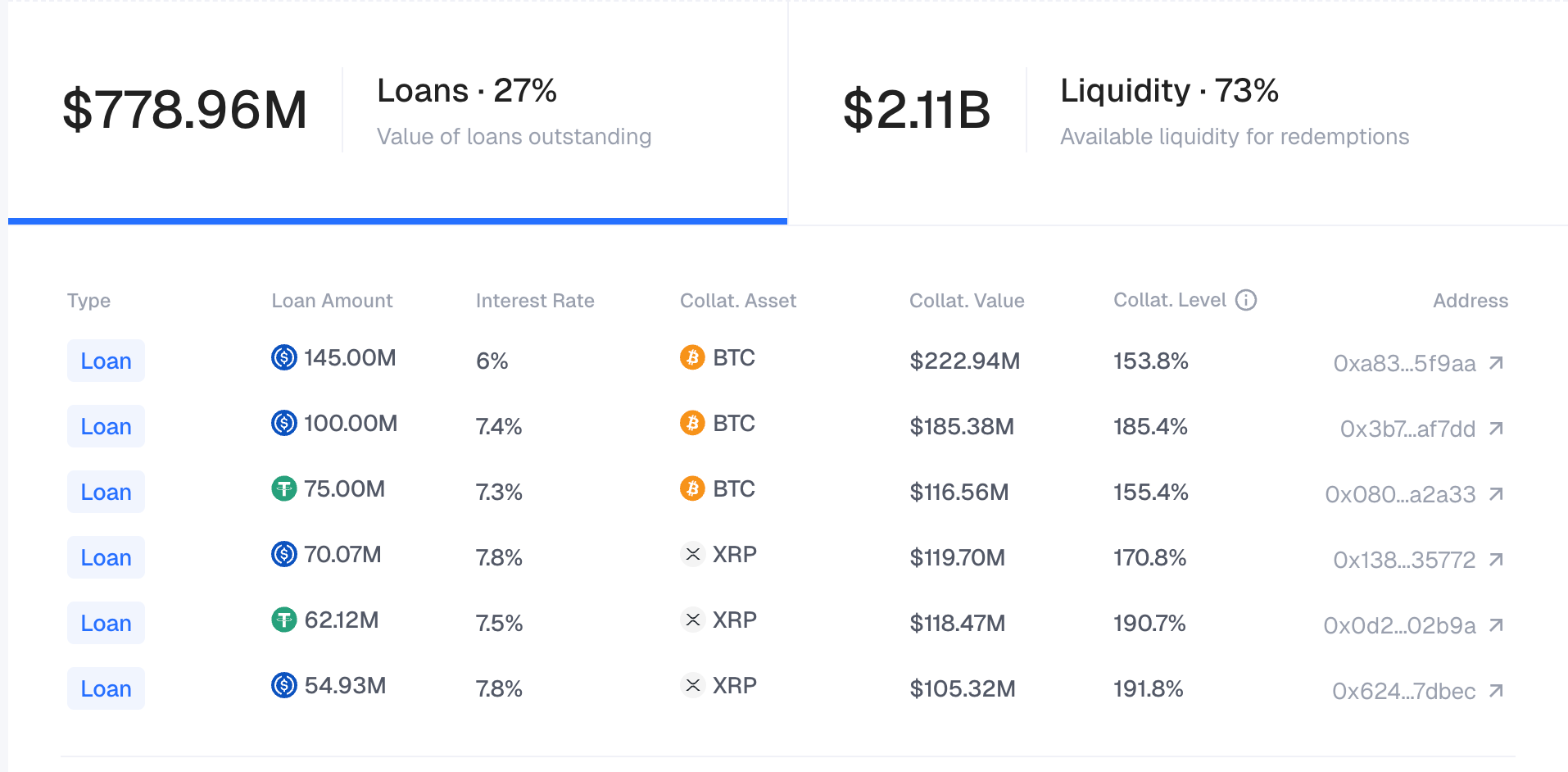

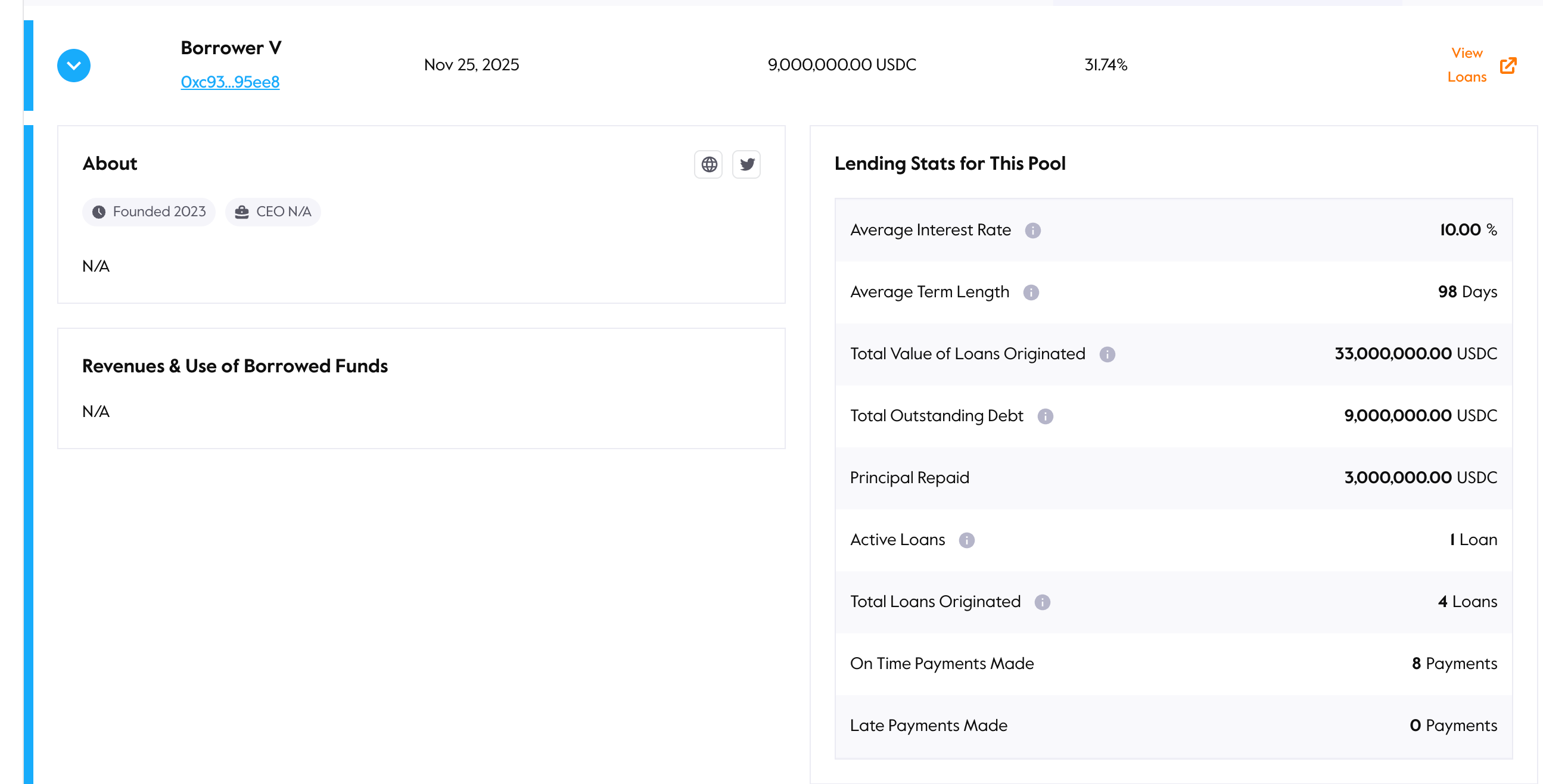

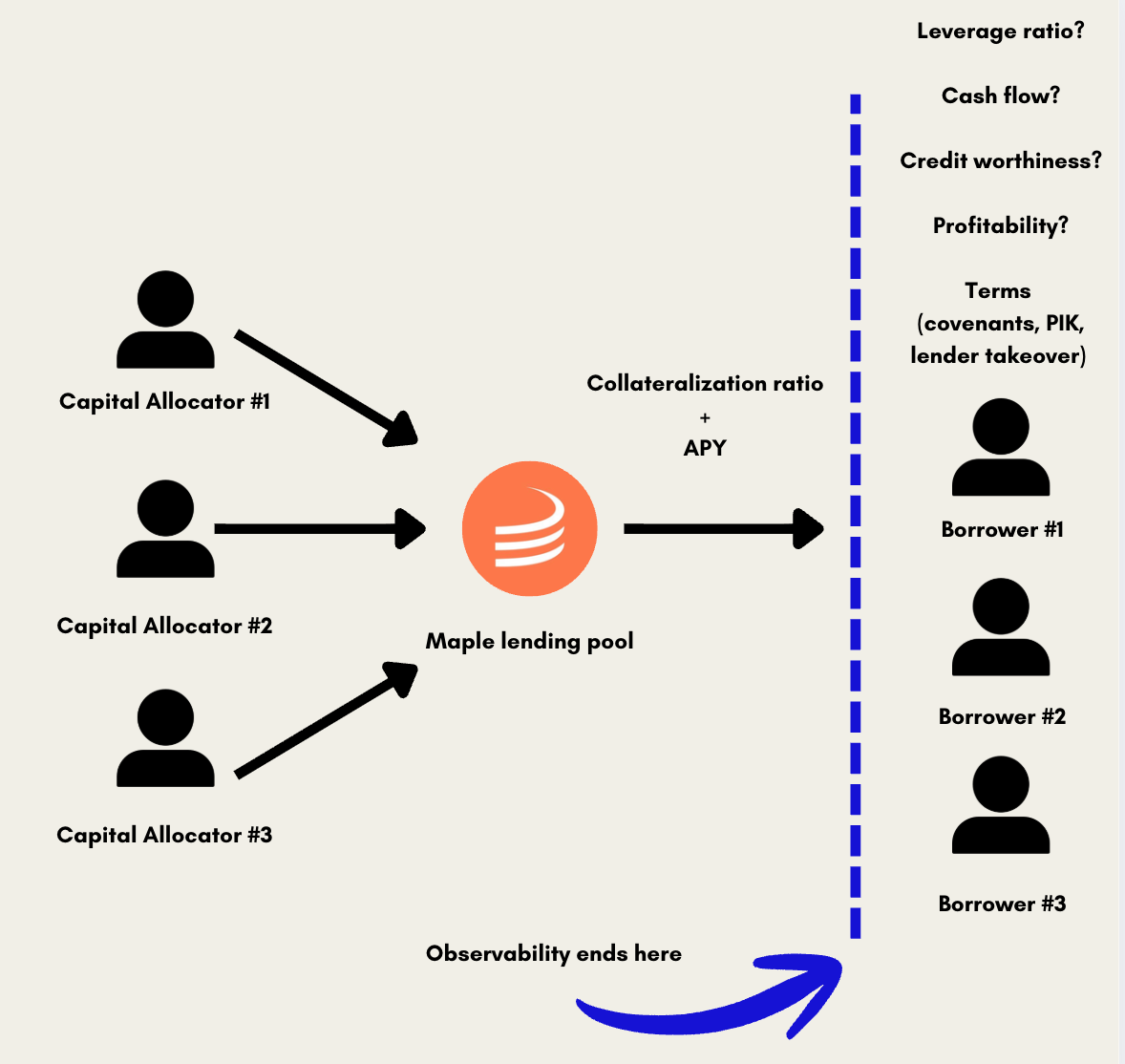

For instance, you can see that a wallet received a loan from Maple. However, you cannot see who that wallet belongs to, what the loan terms are, whether covenants exist, or what the collateral actually consists of. We only know the collateralization ratio, which is a step in the right direction.

However, visibility ends exactly at the point where it would matter most. You have to trust that underwriters have done their due diligence.

The problem with private credit is both an incentive and information issue. Lenders and borrowers may benefit from lack of transparency: they can adjust distressed loans discreetly via hidden amendments, extensions, or PIK interest. There is a reason businesses choose more expensive private credit over cheaper high‑yield bonds for funding.

If the counterparty is a trading firm, the risk is that borrowed capital is repeatedly rehypothecated rather than used in a real underlying business, as the Elixir–Stream episode showed. Capital can be borrowed at one rate, redeployed into slightly higher‑yield venues, and then pledged or lent again, stacking apparent yield and intermediaries on the same collateral. By the end of that chain, there may be no genuine activity or asset underpinning the returns, only a fragile spread that vanishes when too many lenders try to redeem at once.

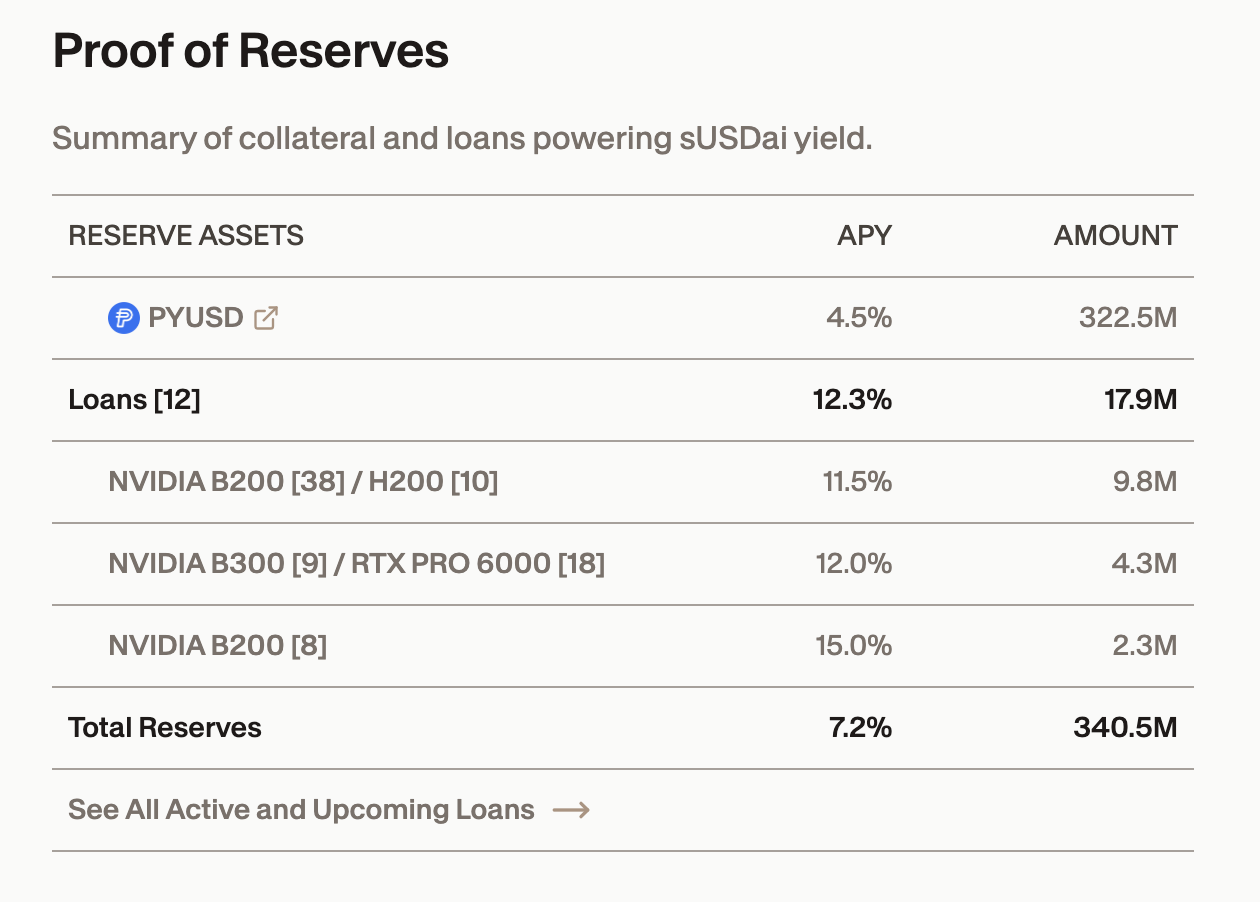

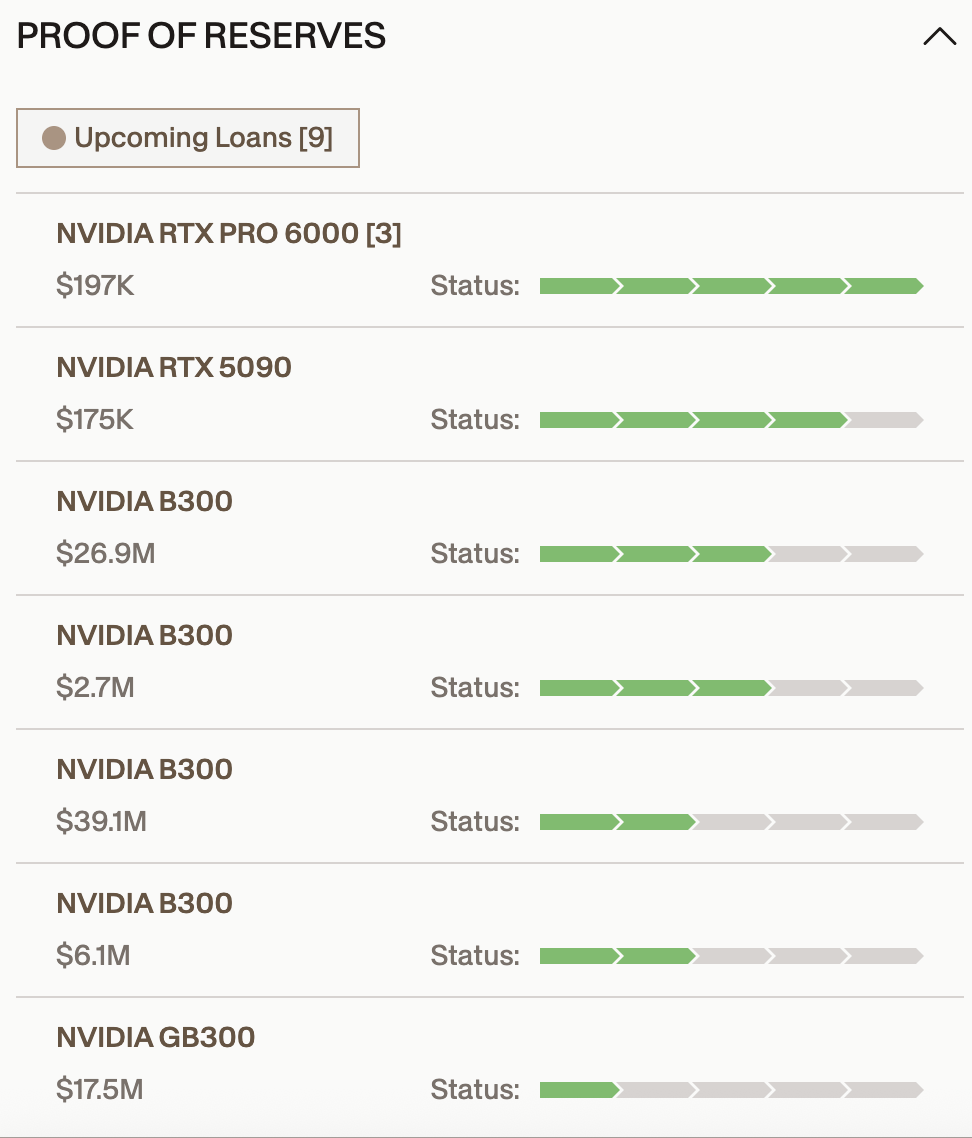

Maple’s dashboards are a bit more opaque, but there are also encouraging examples like USD.ai’s transparency dashboards. Their proof‑of‑reserves views show live collateral, active NVIDIA GPU loans at 11.5–15% yields, with individual loan status visible in real time. That is genuinely better than a quarterly filing. But due to the nature of private credit, these loans are still largely a black box.

Another promising solution is on‑chain rating agencies like Credora, but they still do not answer the question of who exactly the capital is going to.

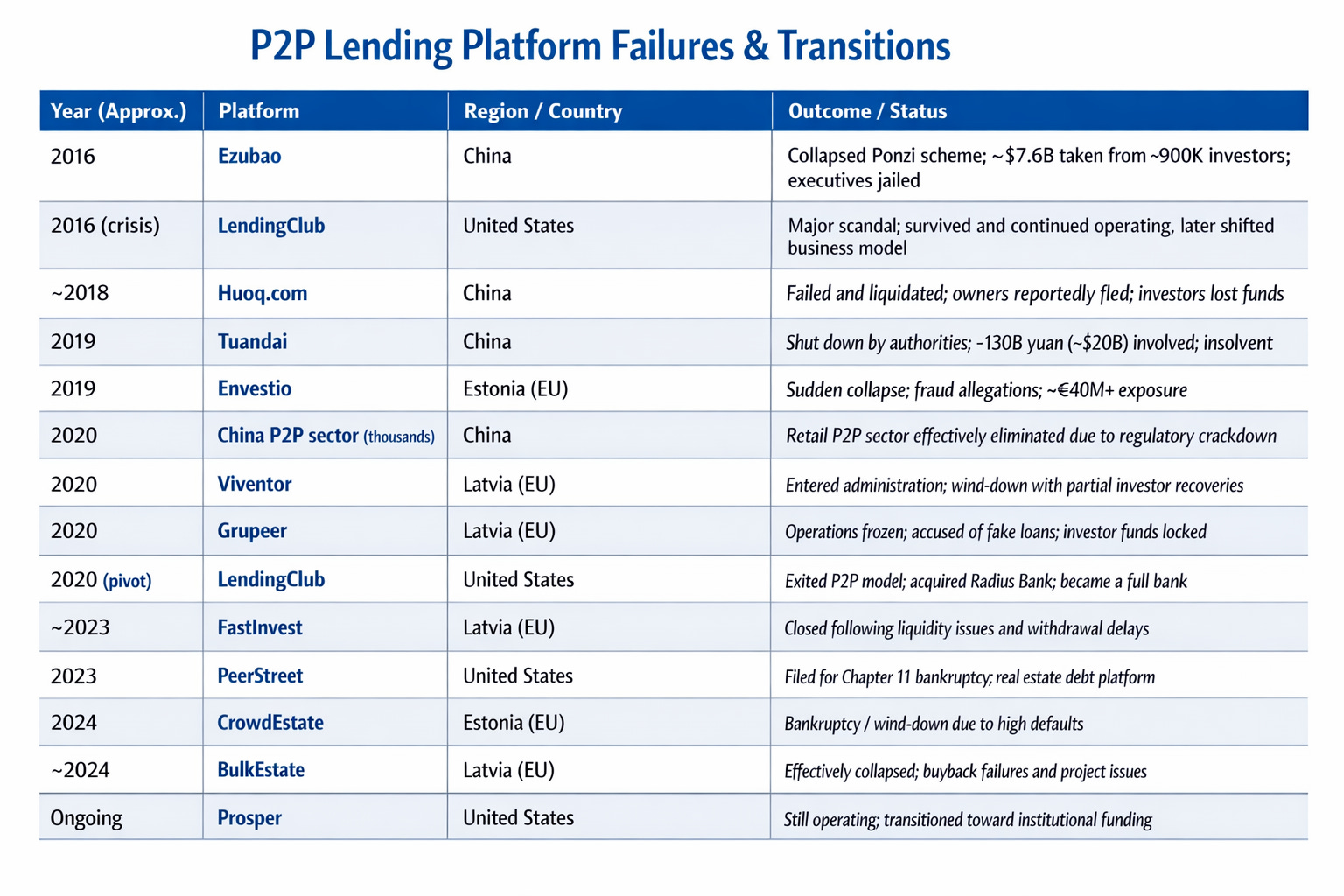

The current iteration of fintechs and on‑chain lenders is the first serious attempt at serving the underserved lending market. Countless P2P lending firms have shut down over the years mainly due to liquidity issues and opaqueness. We should not repeat the same mistakes this time around. Transparency would be a step in the right direction.

VI. AI-Powered Credit

Private credit is a centralized endeavour with underwriters as the bottleneck to new deals and decisions. The fully decentralized DeFi version of this has not been feasible at meaningful scale for good reason. Technically, a DAO could receive debt applications and allocate based on token‑holder votes. The issue is low DAO voting participation and lack of domain expertise. More tokens do not equal more expertise.

AI will help in two ways: better packaging of investment decisions and improved information flow.

First, AI agents could process a large array of deals and give clear outputs to vote on, transforming pedantic things like loan structuring into things like default risk, industry risk levels, opportunity cost, and estimated risk‑adjusted returns. While agent development will still require a centralized dev shop, even this can be democratized using tools like Claude Code. The capital‑allocation “DNA” of a DAO can be codified into agent instructions. Those instructions can be voted on by token holders in proportion to their stake. While this does not solve turnout, it gives more understandable signals to vote on. Periodically, the agent’s “DNA” can be updated to reflect the changing token‑holder base.

Second, maybe more crucially, a layer of agents under a senior underwriter could negotiate loan terms, settle positions, service the loan book, collect interest, and manage the full credit lifecycle. The outcome is that a platform like Maple can manage multiples of its current volume without proportional headcount growth. The infrastructure to build this exists today.

Taken to its conclusion, this enables private‑credit risk models that update hourly and post on‑chain. Credit agents from lenders and borrowers interact directly, giving lenders real‑time visibility into counterparty health. The transparency gap is not a data issue but a reporting/effort issue. The data exists at the company level. It is a tooling and incentive problem, and AI agents are the most credible solution to it currently available. If anyone wants to build this, you are interested.

All of this shifts the math from opaque decisions like “should we lend to this counterparty,” which requires expertise most holders do not have, to “what kind of lender do we want to be,” which is a question any holder can engage with meaningfully, and where each DeFi protocol can differentiate itself.

VII. How DeFi Wins and Loses

The historical analogy worth keeping in mind is Visa in the 1970s. When Dee Hock built Visa, he was not selling a centralized financial product. He was selling an open acceptance network. The assurance that a card would work anywhere, with any merchant, without the issuing bank needing a direct relationship with each counterparty. The network’s value derived entirely from its openness. Exclusivity would have killed it.

DeFi’s structural equivalent is composability. The assurance that any asset, any protocol, and any yield strategy can plug into the same infrastructure without permission. That is the moat TradFi cannot replicate on permissioned chains, because permissioned chains require someone to grant permission, which means the network is only as open as whoever controls access decides it should be. Composability compounds in ways permissioned systems structurally cannot.

As discussed, DeFi wins by being first to genuinely new asset classes, not re‑tokenizing what TradFi already handles efficiently, but bringing net‑new asset classes on‑chain: GPU compute, reinsurance, DePIN networks, and AI agent economies, before traditional capital markets have the infrastructure to reach them. The first mover in a new asset class has a window before institutional capital arrives and compresses yields. That window is the opportunity. DeFi also wins through funding the long tail of borrowers and projects that traditional credit ignores, the original promise of banking the underbanked at scale.

DeFi loses if it becomes a yield‑extraction machine for Wall Street. The pattern is predictable and has precedent. DeFi innovates → Wall Street observes → Wall Street builds a compliant permissioned version → Wall Street pulls its capital into that version. JPMorgan’s Quorum in 2016–17 was the first attempt. It failed because institutions could not agree on governance, but corporate chains today may be running the same playbook, depending in part on whether they democratize validation (for example, Canton’s small validator set). DeFi’s institutional capital base migrates to a walled garden most cannot access. This is not constrained to DeFi either; neobanks like Robinhood are building their own prediction markets on off‑chain rails.

The second loss condition is more gradual. Competition for depositor capital forces protocols to offer higher rates to stay competitive. Higher rates require moving down the risk curve. While introducing new underserved asset classes on‑chain comes with inherent risks, a race to the bottom can cause DeFi protocols to become sloppy. Moving down the risk curve could eventually produce a blow‑up that resets confidence across the category. The Ethena situation was a relatively innocuous preview of this, Elixir less so.

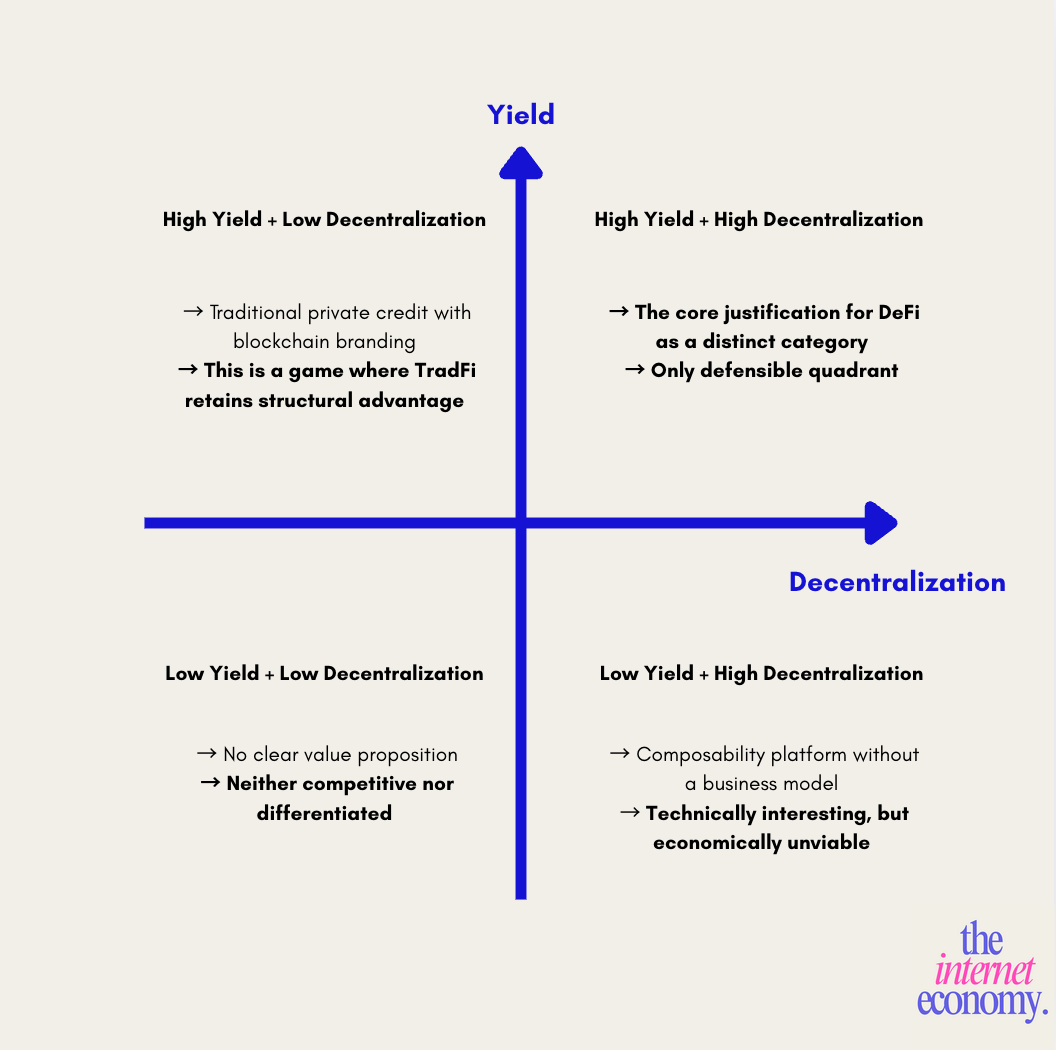

The matrix that determines the outcome is yield against decentralization. High yield with high centralization is traditional private credit with blockchain branding, and TradFi wins that game on its own terms. Low yield with high decentralization is a composability platform without a business model. The only position that justifies DeFi’s existence as a distinct category is high yield with genuine decentralization, backed by the transparency infrastructure that makes that risk legible to the people taking it.

If you are working on any of these problems, you should reach out.

Work With Me

I advise protocols, funds, and financial institutions on DeFi market structure, tokenization strategy, and the intersection of AI and on-chain capital markets. If you are evaluating where to position in this space, building infrastructure that touches any of the dynamics described here, or trying to explain this market to institutional stakeholders who need a clearer frame, reach out.

LinkedIn: https://www.linkedin.com/in/jurgis-pocius/

Email: jurgis@evoaai.com

If this was useful, forward it to one person who should read it. If they are not already subscribed, the link is below. Every issue is an attempt to be early and specific about where the internet economy is actually going, not where the consensus says it is.

Read by teams at Solana Labs, Delphi Digital, Collab+Currency, 1kx, Multicoin Capital, and by operators at Prada, Dior, Nike, JPMorgan, McKinsey, HBS, and other leading funds and traders.