Is Luxury Dying?

Inside the 2026 Landscape

Unless otherwise noted, all figures in this report are based on desktop research and sourced from official financial reports.

The global personal luxury goods market is at an inflection point. After a decade of almost uninterrupted expansion, interrupted only briefly by COVID, the industry saw its first meaningful contraction in 15 years in 2024–2025, with the market stabilizing at around €358 billion in 2025 (flat to -2% year-on-year). Approximately 50 million luxury consumers have exited the market since 2022, effectively wiping out the aspirational buyer segment. Within this contraction, a brutal divergence has emerged: Hermès and Prada are gaining share, LVMH and Richemont remain resilient, and Kering is in structural crisis.

This report examines the seven houses that define the current luxury landscape: LVMH, Hermès, Chanel, Kering, Richemont, Moncler, and Prada, through the lens of financial performance, strategic positioning, and forward-looking catalysts. It is written for investors, operators, and strategists who want clear insight into where the industry is heading and which houses are positioned to lead.

More than a Cyclical Contraction

The most alarming data point is not revenue decline; it is the erosion of the customer base. Between 2022 and 2025, the active luxury consumer pool shrank from roughly 400 million to about 330 million. This is not a cyclical pullback. It reflects:

Aggressive price inflation (2020–2023): Cumulative price increases of 40–60% across the industry have priced out aspirational buyers, likely permanently.

Value-perception collapse: More than half of surveyed luxury consumers say quality no longer justifies the price.

Generational shift: Gen Z advocacy for luxury brands continues to decline as spending rotates toward experiences, wellness, and cultural objects.

Resale cannibalization: A luxury resale market of roughly €35 billion, growing at 10–11% annually, offers a more accessible entry point and undercuts full-price demand.

Where We Are Now: Brand Performance

Hermès’ positive Q4 2025 earnings were no surprise to anyone following the sector, but the industry overall is in a period of growing pains driven by weaker Chinese demand and the disappearance of the aspirational consumer.

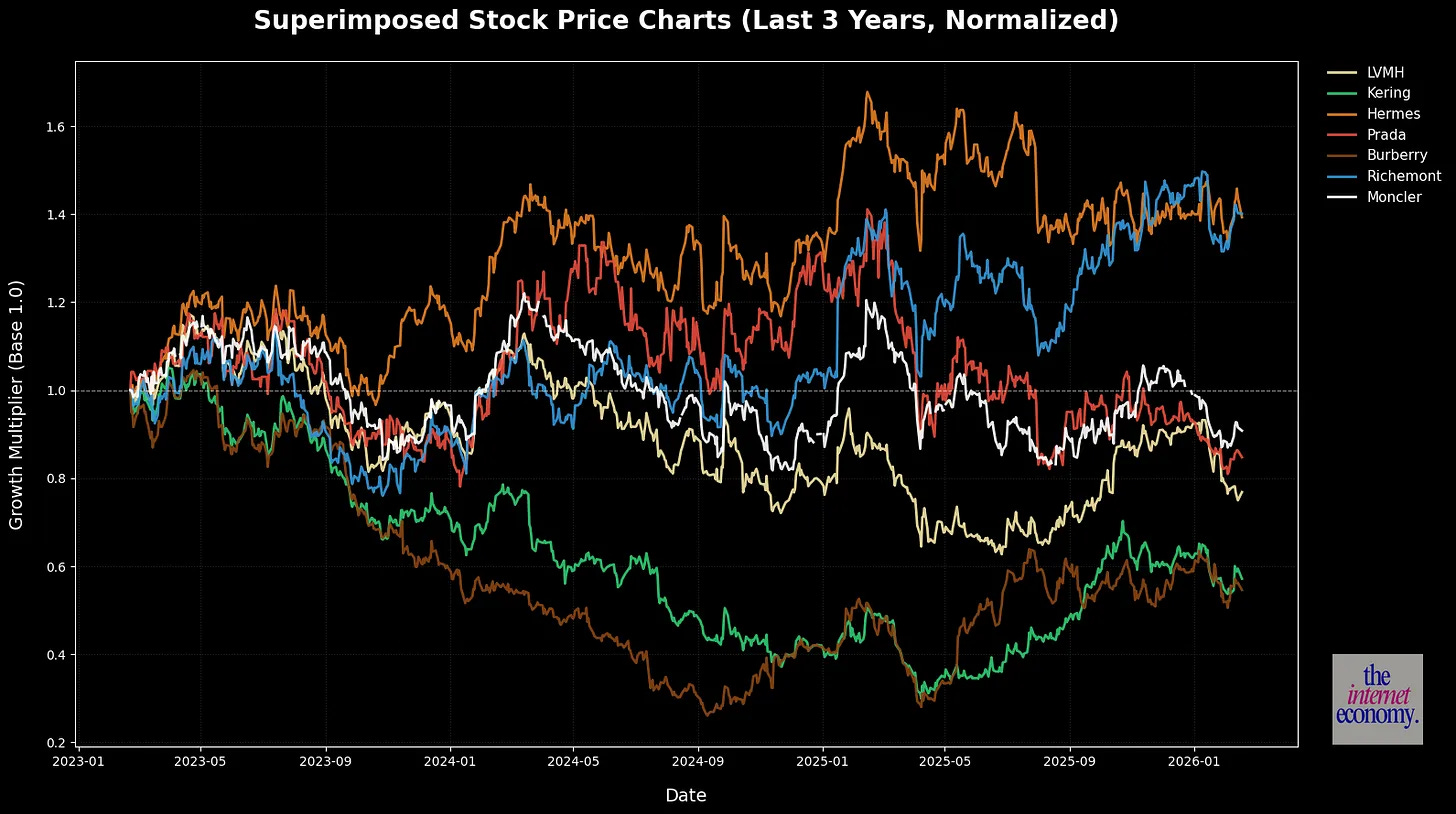

On public markets, Hermès and Richemont are the clear winners, the only major names whose share prices are in positive territory since January 2023.

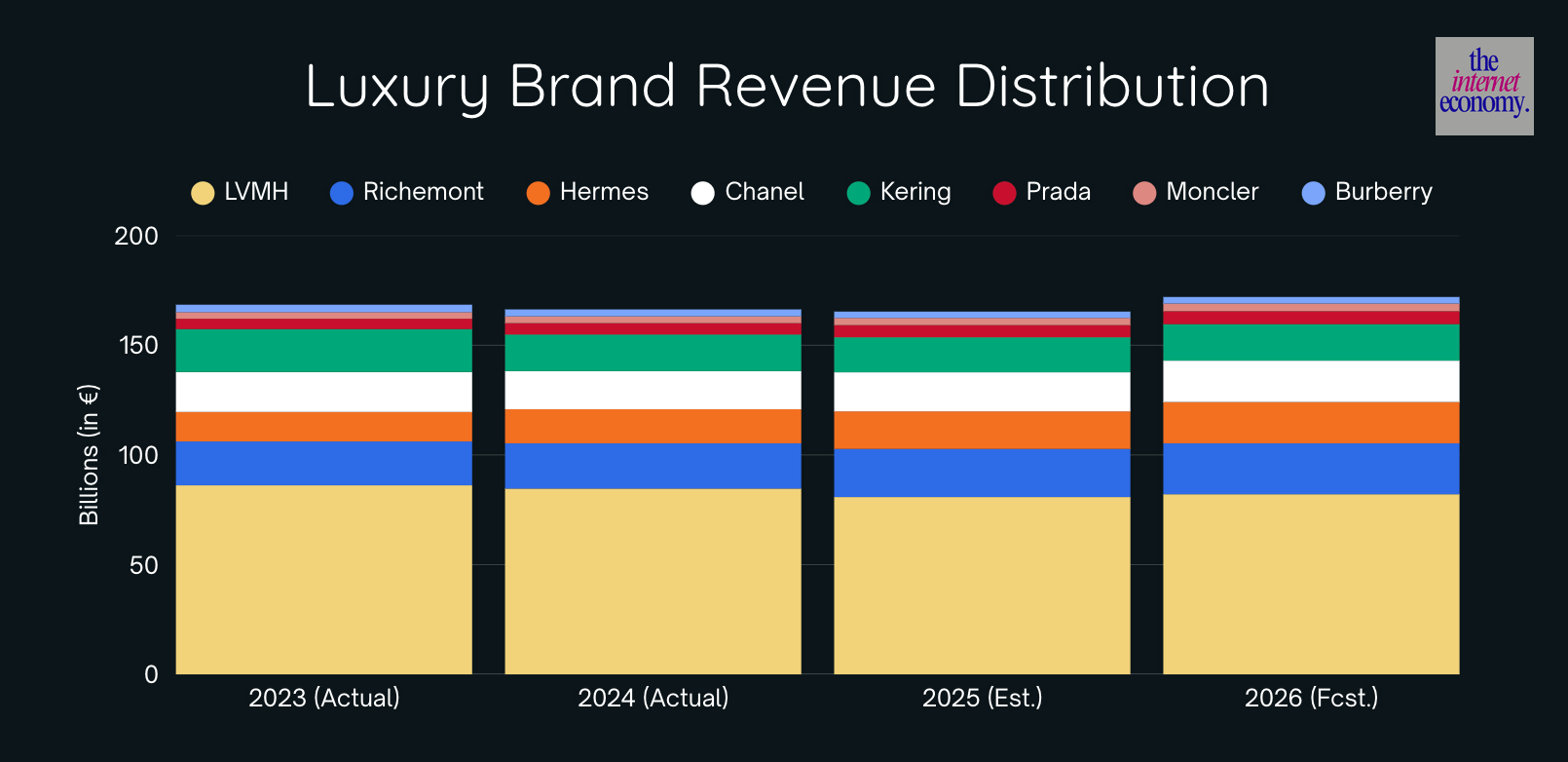

In terms of scale, LVMH still dominates, accounting for roughly half of the large-cap luxury group universe by revenue. Kering, Chanel, Hermès, and Richemont each sit at around 20–25% of LVMH’s size.

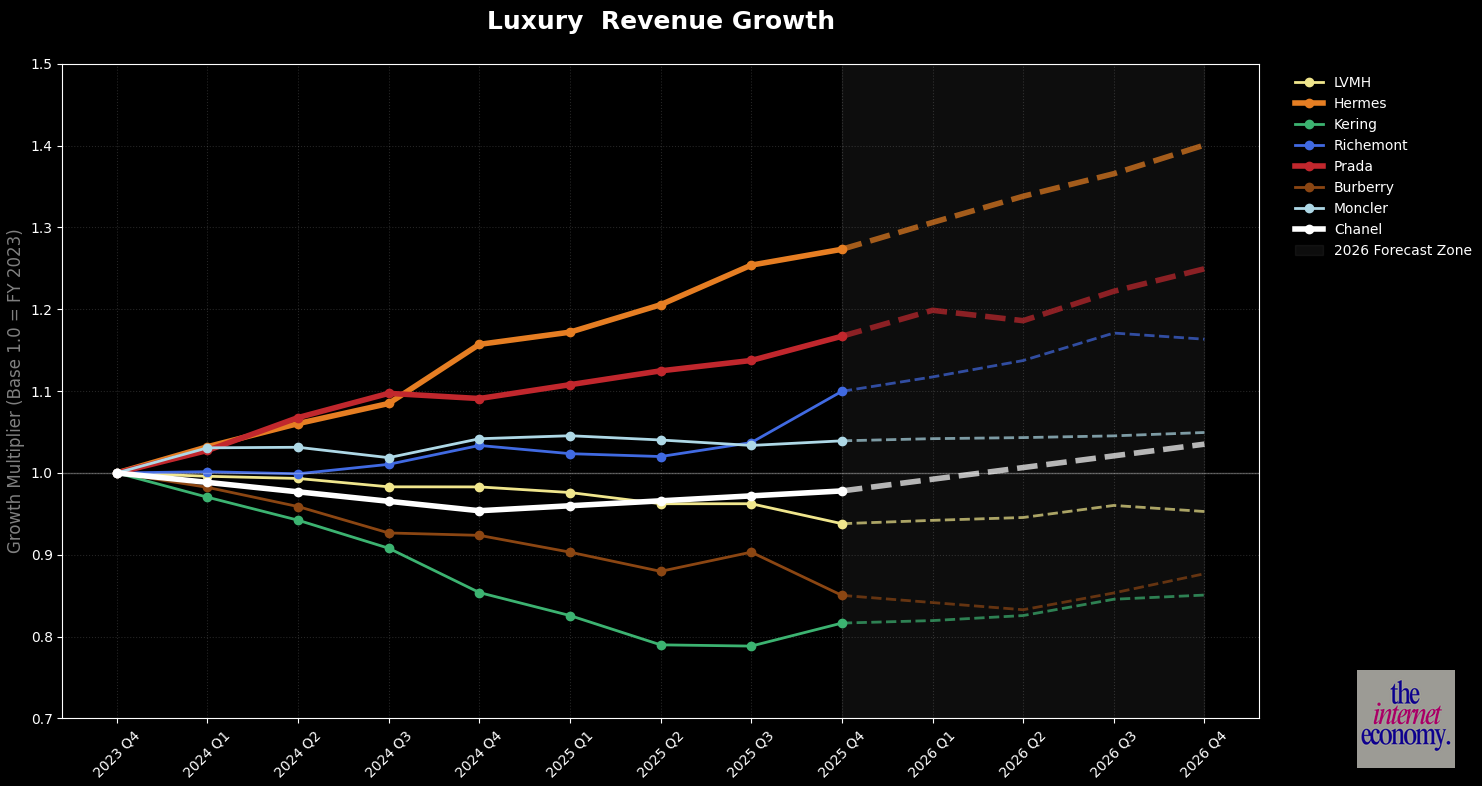

Revenue growth tells the more interesting story. LVMH is slowing, while Hermès and Richemont continue to grow. Prada and Moncler follow. For the rest of the major houses, growth has decelerated sharply and, in many cases, turned negative.

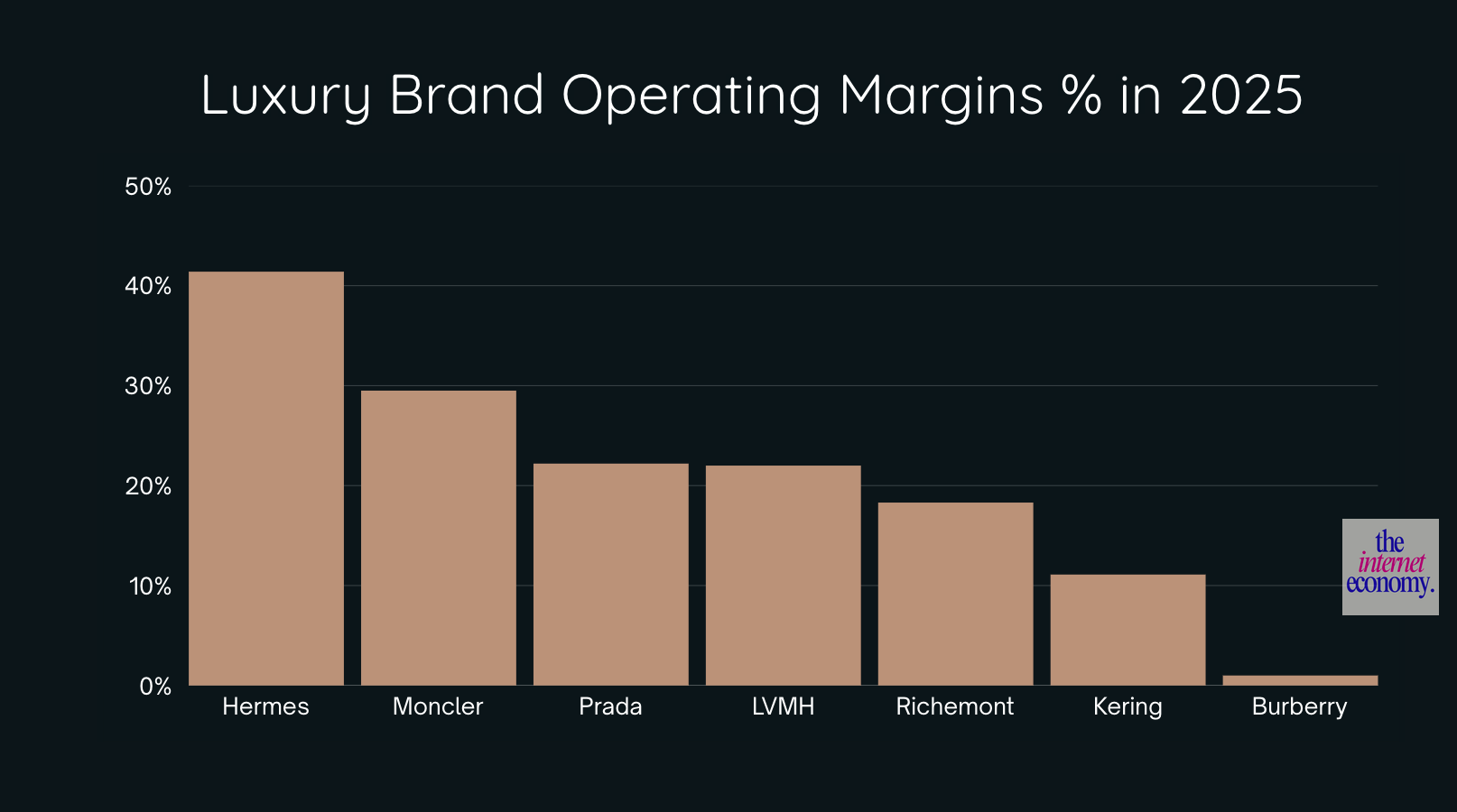

Hermès’ operating margins (around 41%) tower above the rest of the sector. Richemont, by contrast, sits mid-pack despite strong top-line performance, in part because of a roughly 74% increase in gold prices over the past year, which weighs on margins for gold-intensive jewelry maisons.

What’s Working, What’s Not

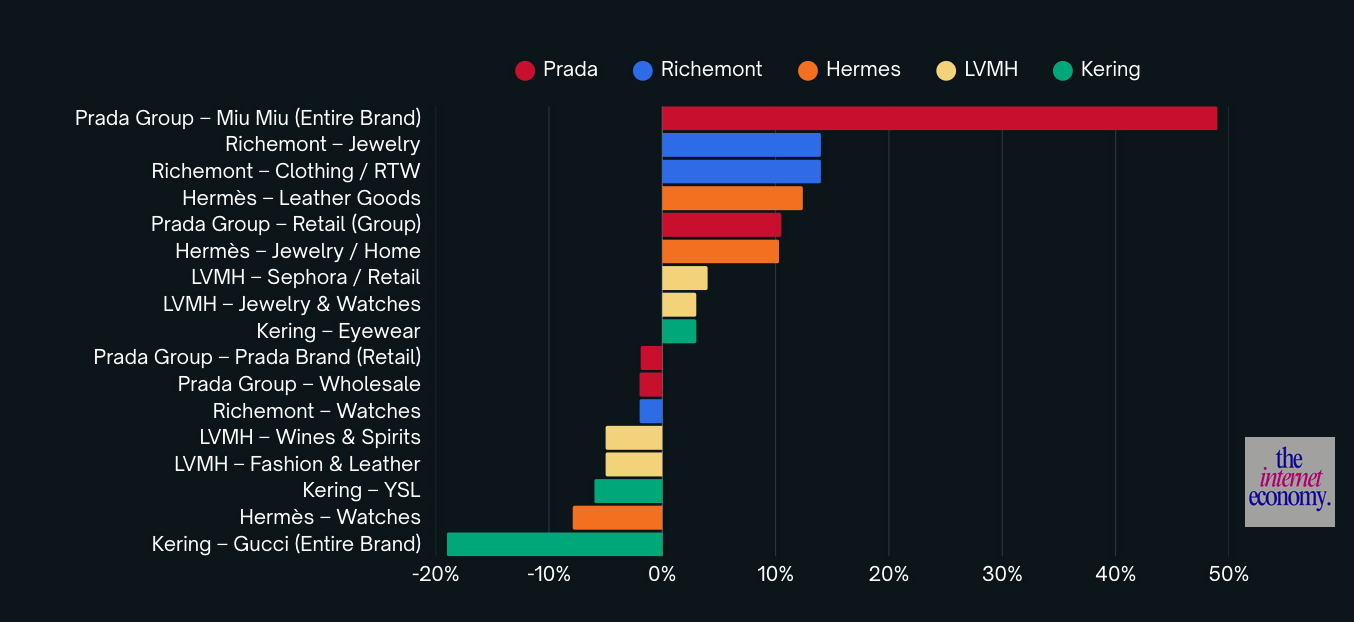

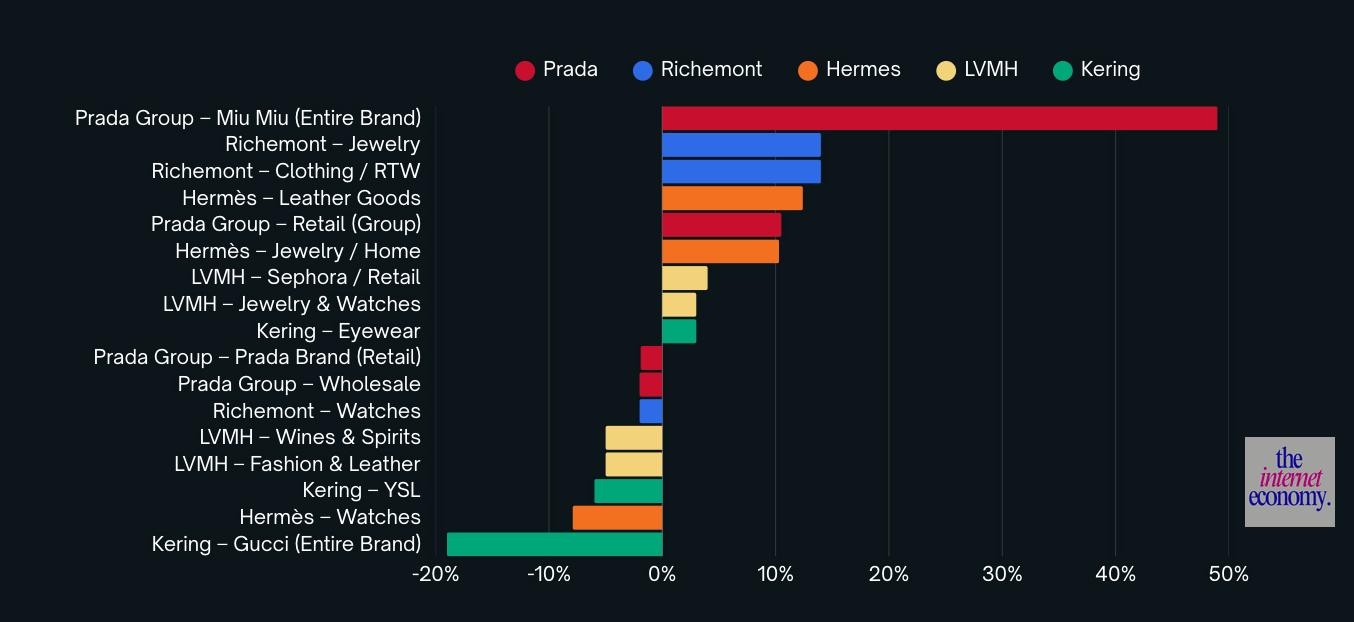

Zooming into categories exposes the underlying pattern.

What’s doing well:

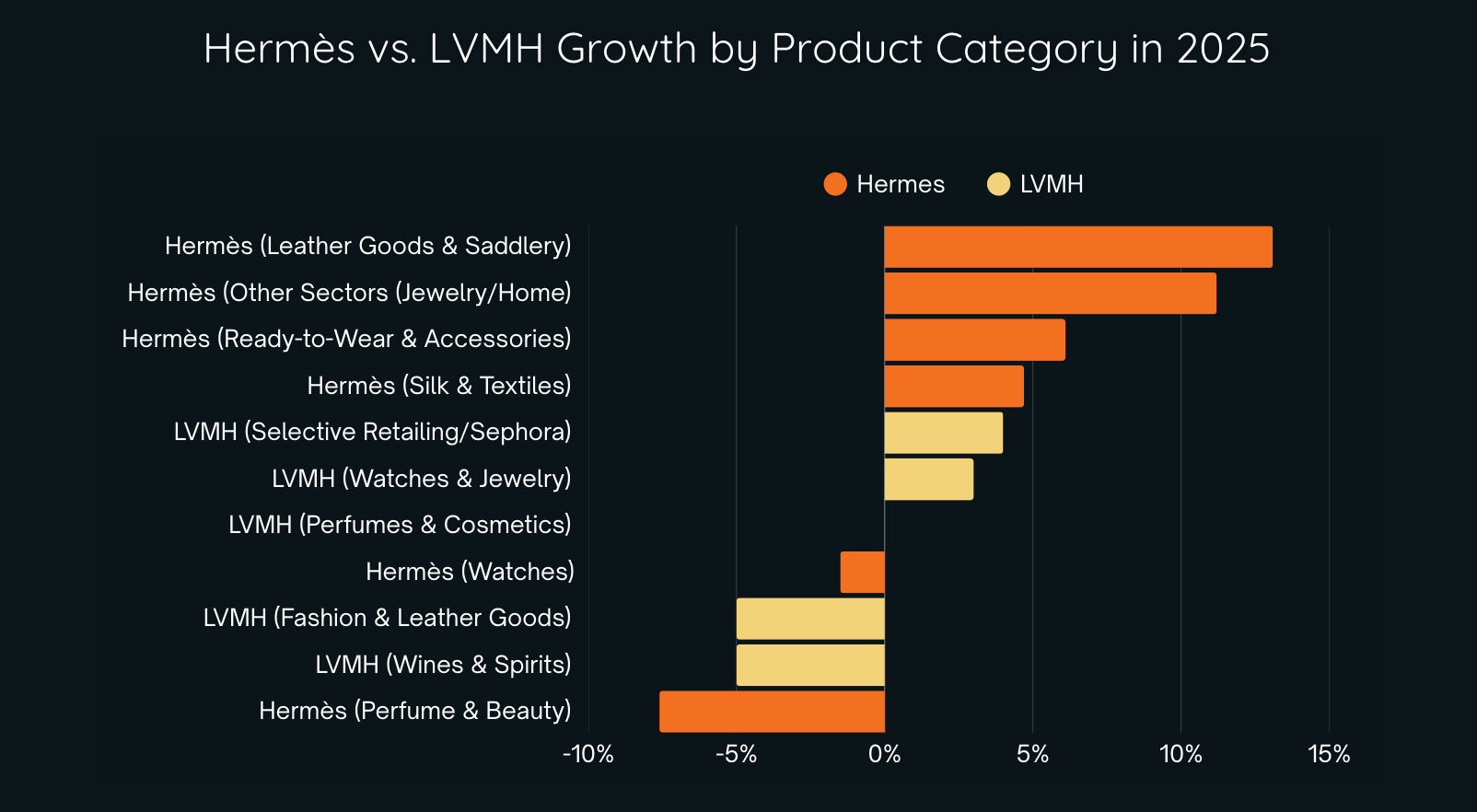

Hermès’ leather goods have maintained desirability

Miu Miu, now roughly 30% of Prada’s revenue, has become a magnet for younger consumers.

Ultra-luxury jewelry: Richemont’s jewelry maisons (especially Cartier) and LVMH’s jewelry division led by Tiffany & Co. have outperformed, proving that true high-end, “wearable asset” products still command demand.

What’s not:

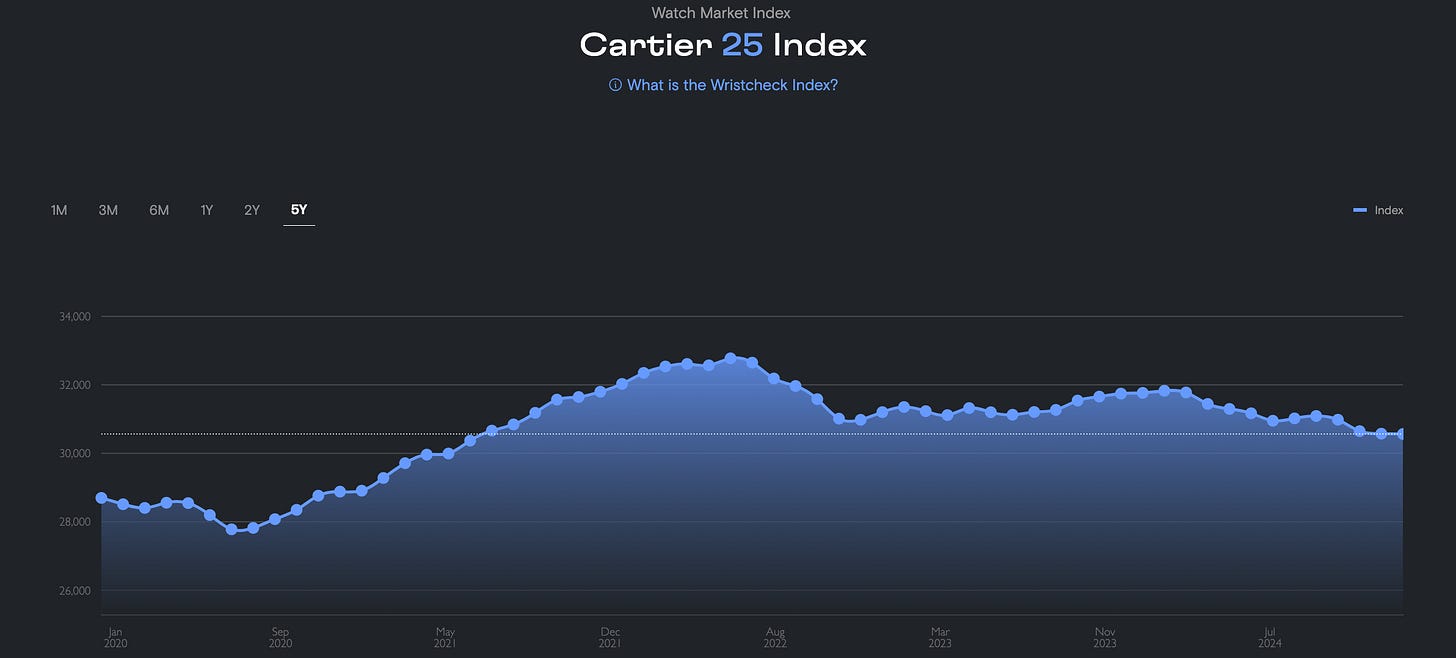

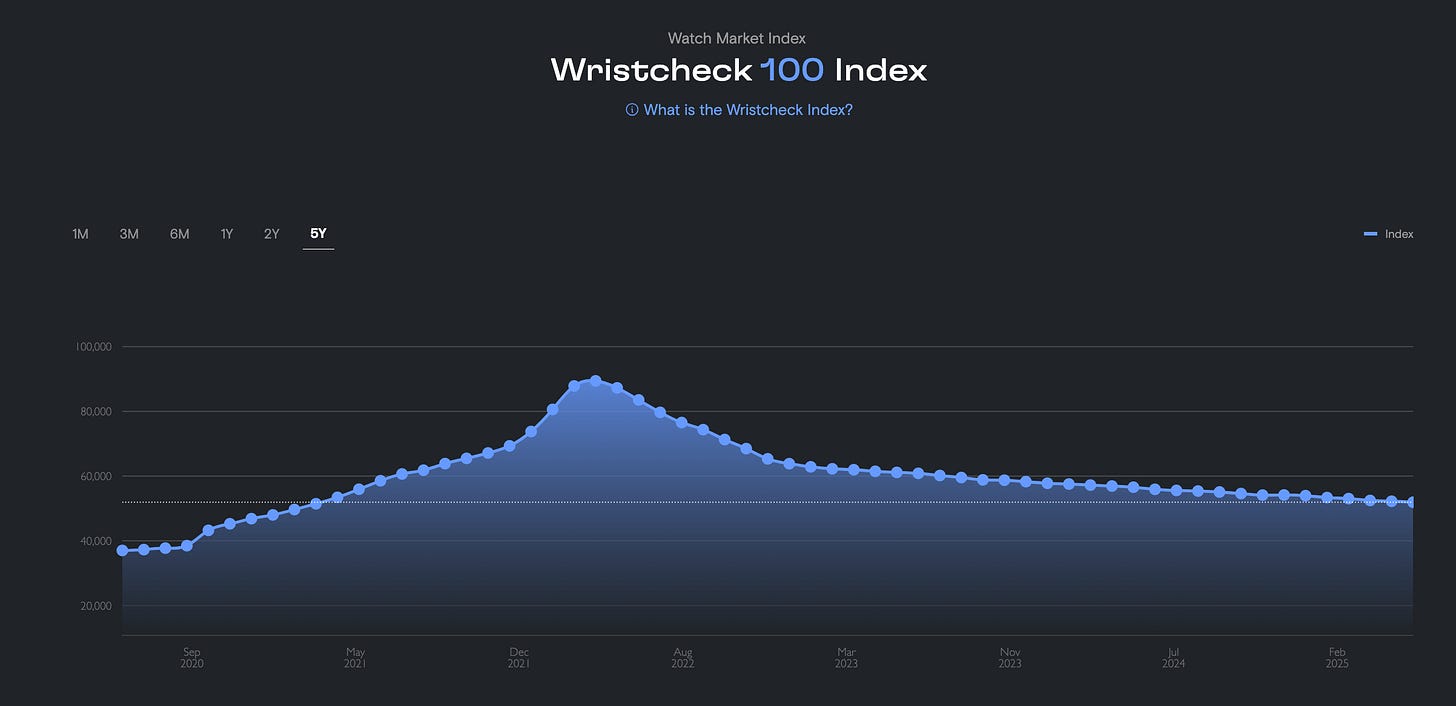

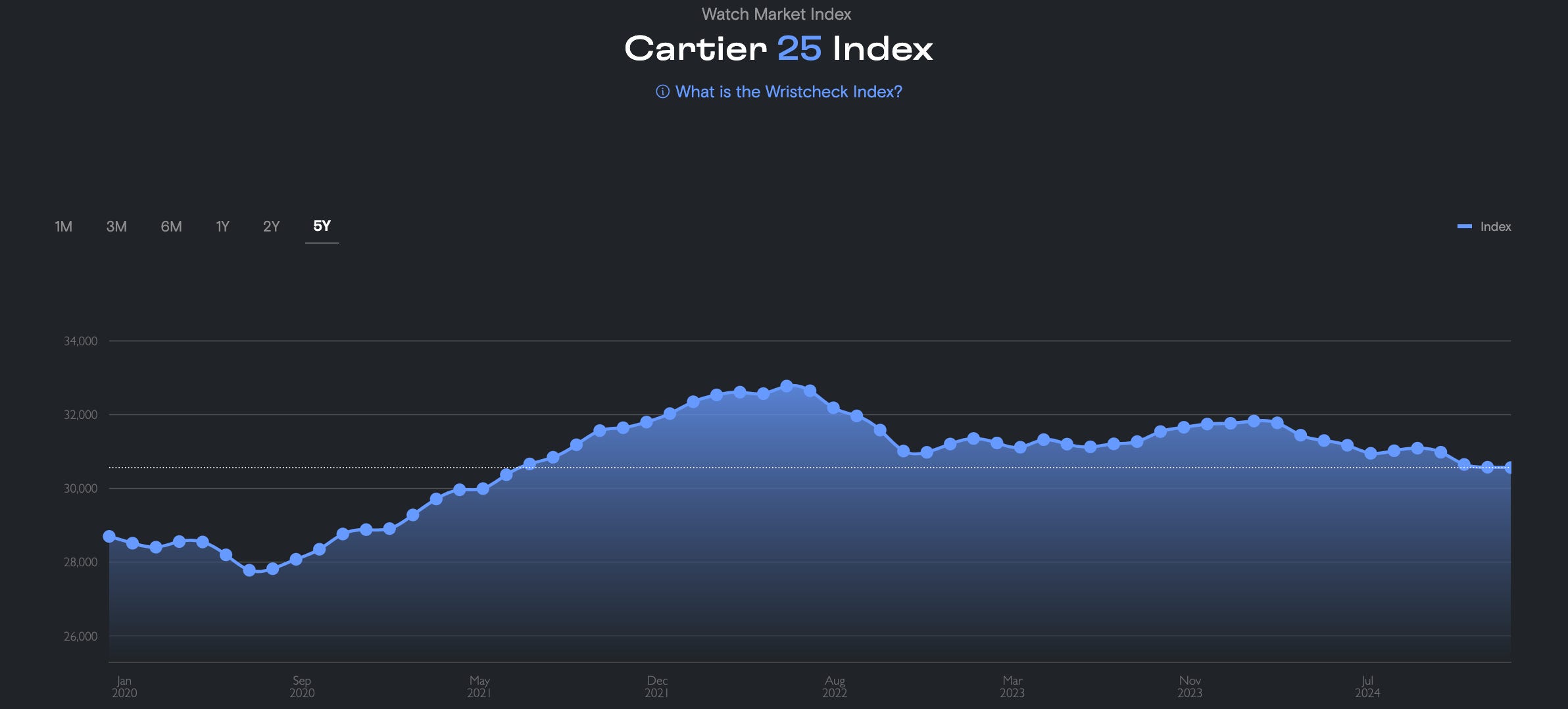

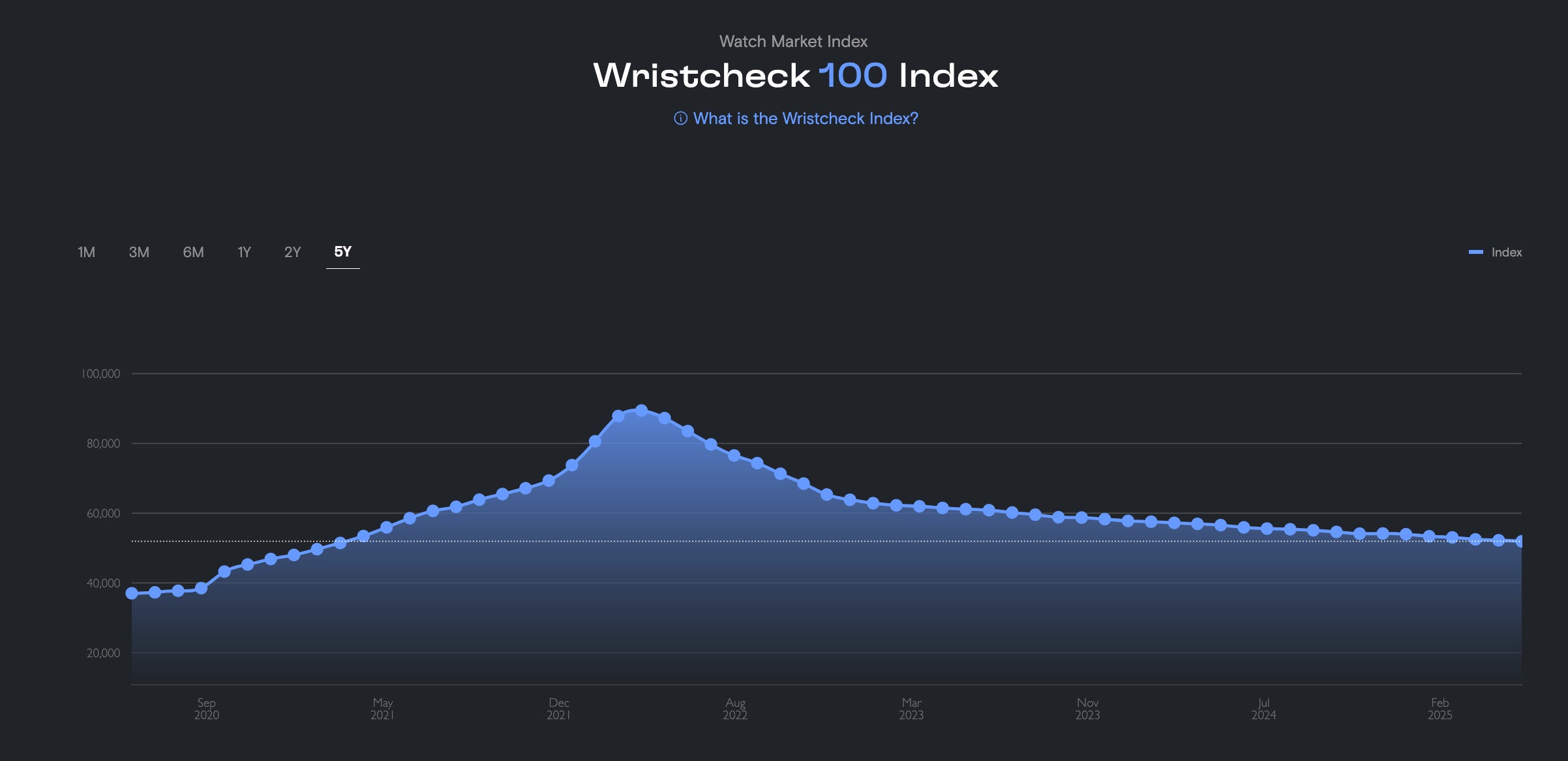

Watches as speculative assets: The post-2021 speculative boom in watches has deflated, with prices correcting across the board. Yet even here, there is divergence: iconic models like the Cartier Tank have held value far better than the broader watch index.

Overextended fashion brands: Gucci’s roughly 19% annual revenue decline recalls its overexpansion in the 1980s and underlines the danger of trend-chasing and logo fatigue.

Revenue growth by product category. (Source: The Internet Economy, 2025 financial statements)

Cartier Watch Index (Source: Wristcheck)

General Top 100 Watch Index (Source: Wristcheck)

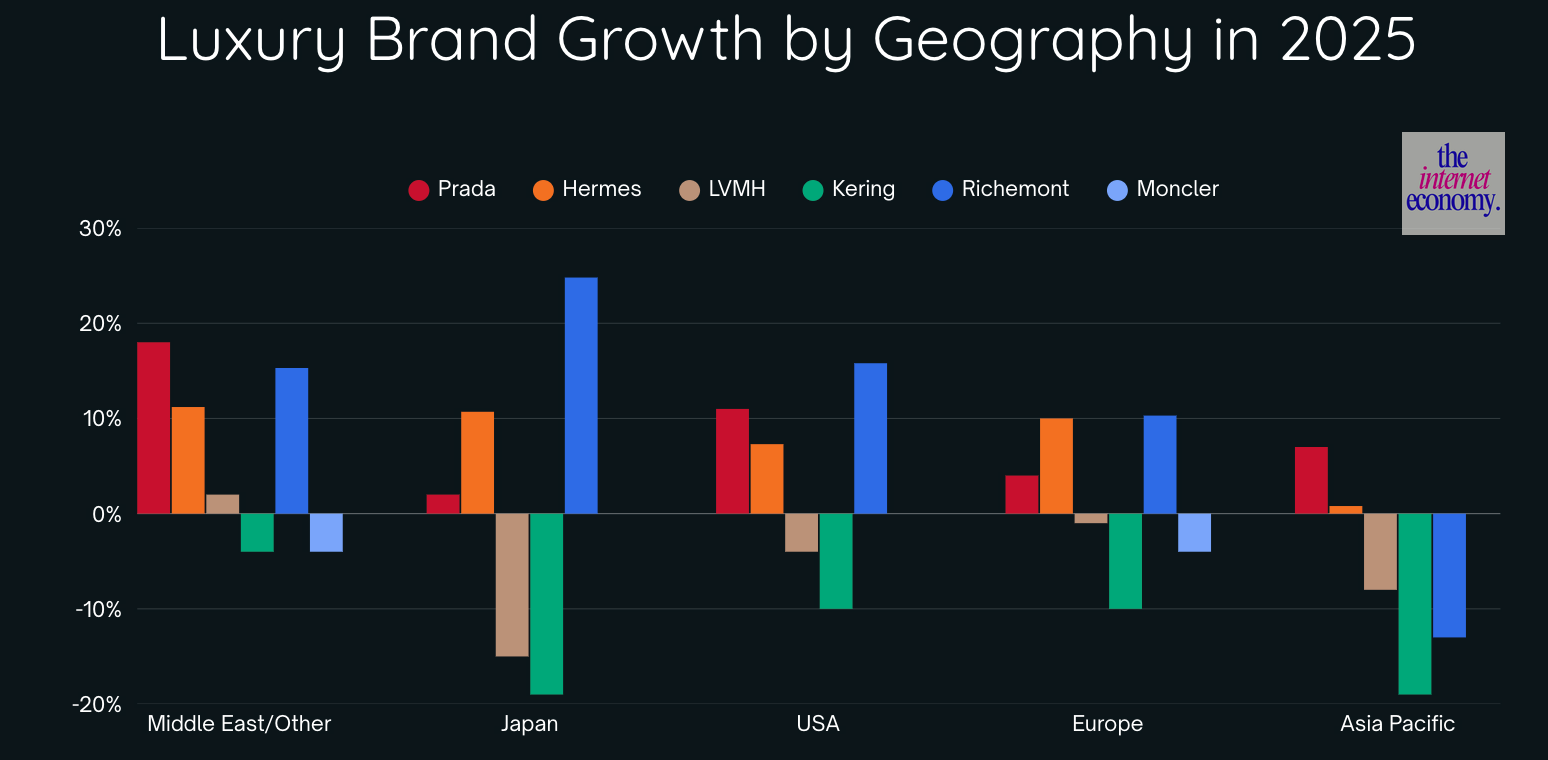

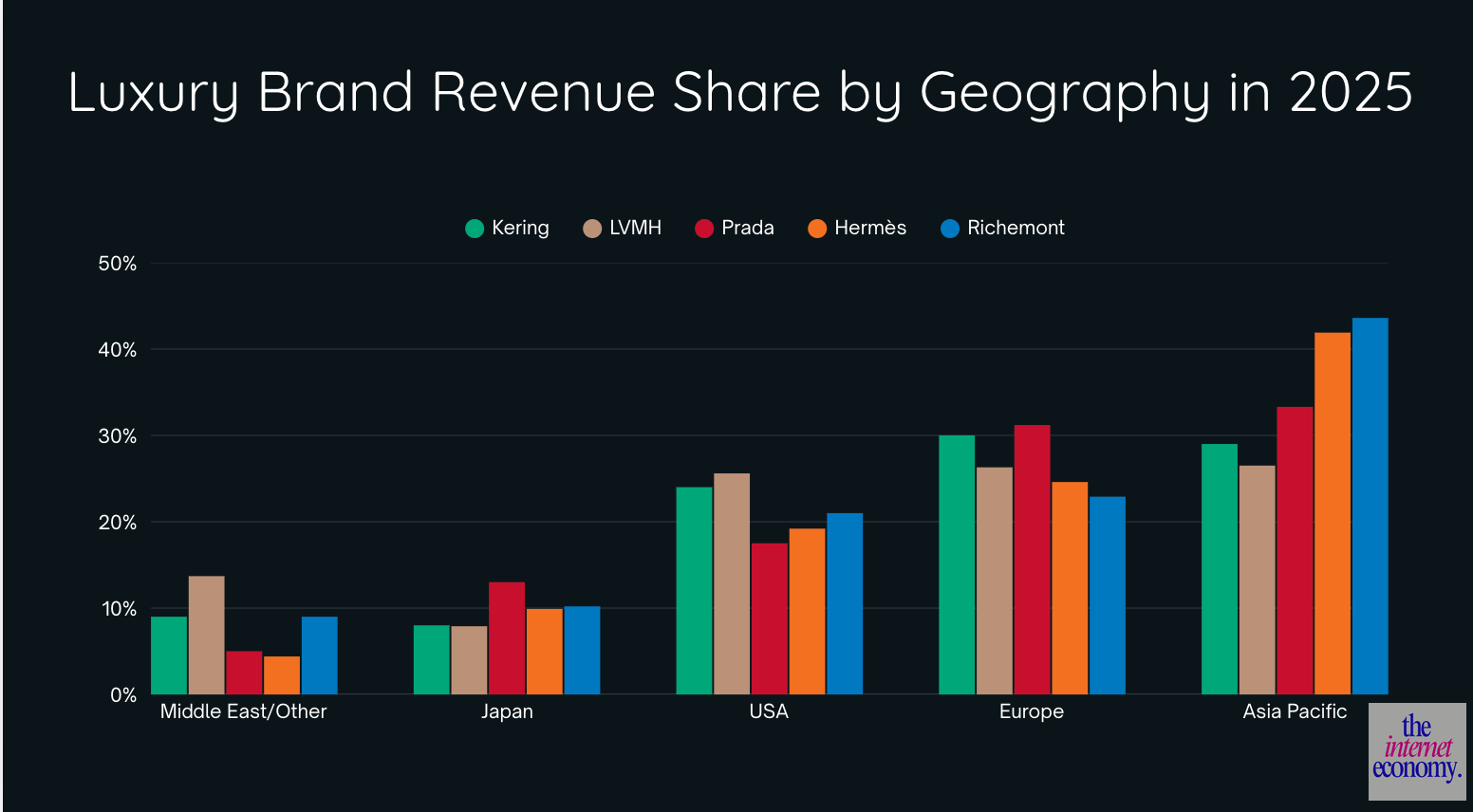

Geographic Trends and the Asia-Pacific Myth

The common narrative of over-reliance on Asia-Pacific is false. In fact, two of the biggest growers this year (Hermès and Richemont) derive the majority of their revenue from that region, roughly 10 percentage points more than their peers.

Key geographic observations:

Japan shows polarization: Richemont and Hermès gained ground while LVMH and Kering lost share

United States demonstrates similar trends with clear winners and losers

Kering is losing in all geographies

Hermès and Prada grew across all geographies

Richemont declined in its most important market despite overall strength

The growth stories have largely been Japan and the Middle East.

LVMH posted negative growth in all key markets

Flagship products with truly high-end luxurious status remain in demand, while product line extensions, speculative assets like watches, and aspirational goods have faltered.

Consumers have become skeptical. If secondary market prices drop or quality appears poor (paying for a logo rather than craftsmanship), they walk away. This mirrors the Gucci licensing debacle of the past.

Why the Luxury Model Is Failing

A review of recent financials and disclosures points to three structural failures across today’s major luxury houses, most visibly at LVMH and Kering.

1) Overextended Into Trends

Many brands have over-indexed on fast-moving trends at the expense of enduring icons and long-term brand equity. When hype becomes the primary growth driver, revenue volatility increases, product cycles shorten, and the perception of timelessness erodes. What was once cultural authority becomes cultural reactivity.

2) Erosion of Product and Service Quality

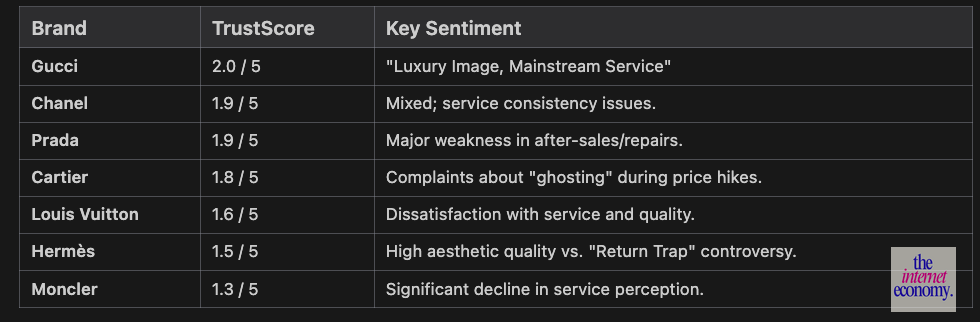

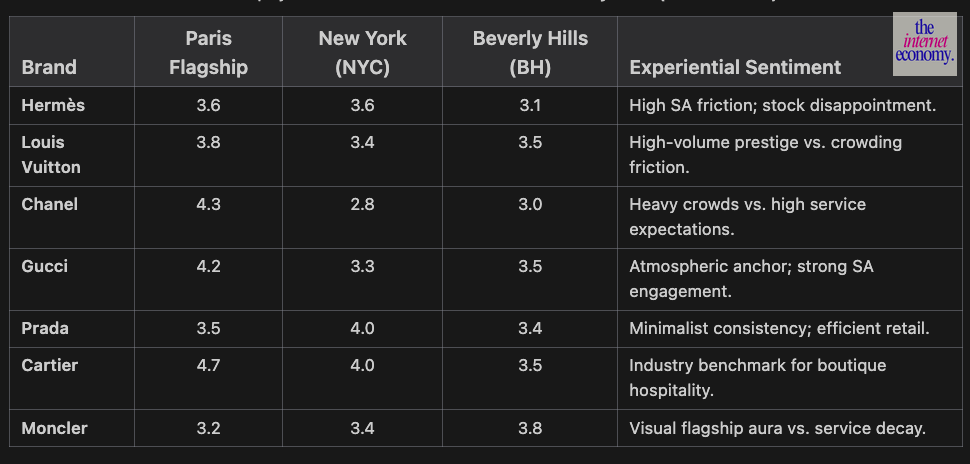

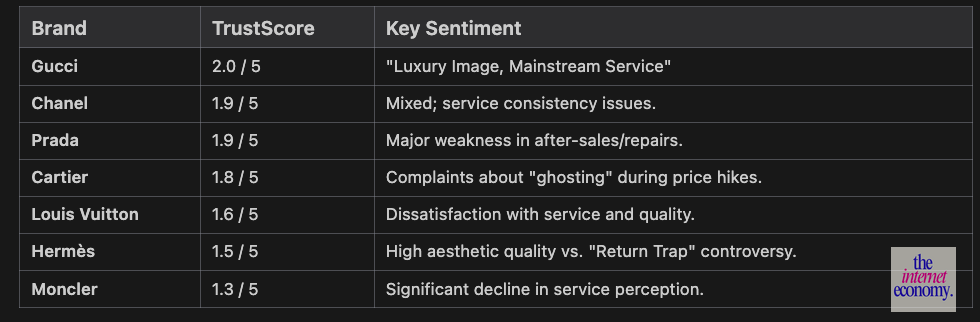

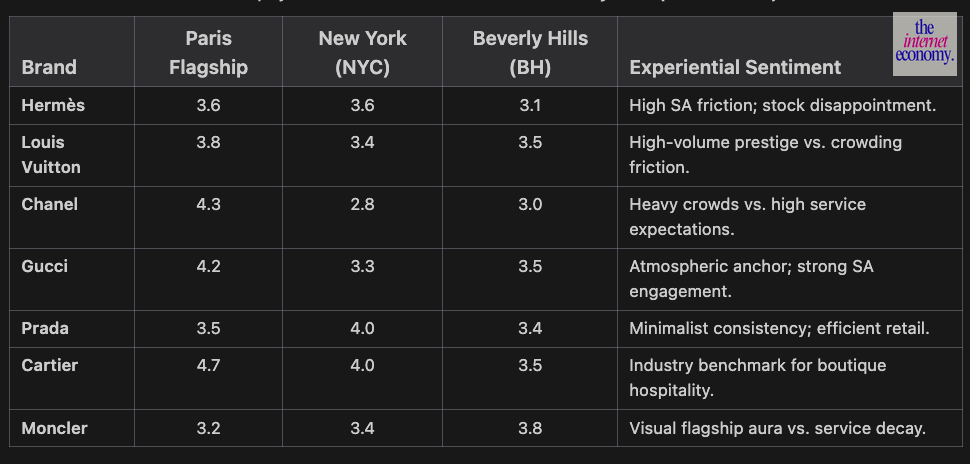

Luxury does not need to satisfy everyone, but it must be exceptional for the customers it chooses to serve. Aggregated analysis of customer reviews across major platforms consistently highlights the same weaknesses: slow responsiveness, uneven after-sales support, and inconsistent treatment across client tiers. The pattern is clear. Boutiques continue to sell a world-class promise, but many houses struggle to deliver world-class service at scale in a digital, omnichannel environment. This gap creates space for more agile, service-first competitors.

Two critical gaps emerge along the customer journey:

The boutique experience anchor: High-prestige flagships function as atmospheric anchors for the brand. Performance is driven by high-touch hospitality, including bespoke events, cultivated sales-associate relationships, and carefully choreographed in-store experiences. This establishes a sentiment floor that sustains loyalty among top clients even when other touchpoints underperform.

Service lifecycle misalignment: Post-purchase, many brands revert to defensive, policy-led service models. Returns, repairs, and complaints are handled through rigid, arbitration-style processes. This approach directly conflicts with the warmth and intimacy of the boutique experience, creating a persistent sentiment gap across the long-term ownership lifecycle.

I scraped trust scores and common pain points from Trustpilot (a review site)

I scraped trust scores and common pain points from Yelp (a review site)

3) Inflation and the Pullback of the Aspirational Buyer

Luxury price inflation has collided with a broader cost-of-living squeeze. Since 2020, aggressive ticket increases layered on top of general inflation have pushed aspirational buyers, and even parts of the affluent cohort, to pull back. Industry analysis increasingly links the loss of tens of millions of customers since 2022 to a combined effect of price elevation, value-perception collapse, and macro pressure. The active luxury customer base is shrinking, with the mid-tier absorbing the majority of the impact.

How Luxury Is Trying to Recover

In response to the shrinking customer base and weakening mid-tier demand, major groups are pivoting their strategies rather than standing still.

1) The Hard-Luxury Pivot

Jewelry has become the strategic priority for almost every group, viewed as a resilient “wearable asset” that outperforms soft luxury (ready-to-wear) in periods of volatility.

LVMH is aggressively elevating its Watches & Jewelry division, with Tiffany & Co. pursuing an upmarket “elevation strategy” (renovated flagships, high jewelry collections like Blue Book) and Louis Vuitton expanding in haute horlogerie and high jewelry through collections such as Awakened Hands, Awakened Minds. Bvlgari has expanded its Valenza manufacturing site to support this jewelry growth.

Kering is pursuing an industrial development strategy in jewelry, including a staged acquisition of Raselli Franco Group to secure manufacturing capabilities and tighter control of the value chain for houses like Boucheron and Qeelin.

Richemont, already the category leader, continues to double down on its jewelry maisons (Cartier, Van Cleef & Arpels), which are growing at double-digit rates and remain its primary growth engine, far outpacing the watch division

Luxury brand strategic positioning

2) Expansion Into Beauty, Fragrance, and Hospitality

Alongside hard luxury, groups are leaning into fragrance, skincare, color cosmetics, and hospitality to keep their brands present in customers’ daily lives while offering lower-priced, higher-frequency entry points. These moves let them monetize brand equity even as big-ticket fashion purchases slow.

3) Return to Direct-to-Consumer Control

Most major houses are steadily pulling distribution back to DTC channels. The rationale is straightforward: tighter pricing control (no discounting or grey promotions), access to rich first-party customer data in an AI-driven world, and full control over how the brand is staged at every touchpoint.

4) Experiences as the new moat

Finally, brands are investing more in experiences, from flagship “world-building” stores and private events to travel, culture, and hospitality, to make entry into their universe feel like stepping into a different world rather than just buying a logo. The open question for the next cycle is whose world will feel compelling enough to justify the price of admission.

Luxury is not dying, but the old model of scaled aspiration is. The future belongs to houses that protect their mystique, treat culture and service as core products, and build worlds that a smaller, more discerning audience is desperate to enter. From here, we can look at the issues through each brand’s lens.

Inside the Luxury Houses

Hermès: Leader in a Stagnant Market Real Physical Luxury

Hermès is the clear outlier in a stagnant luxury market. In 2025, revenue crossed €16 billion and recurring operating margins reached 41%, with the market valuing the house at a PE of around 49 versus roughly 20–25 for LVMH. That valuation gap only makes sense if Hermès is doing something fundamentally different from the rest of the industry. And it is.

1. Slow Luxury as the Ultimate Flywheel

Hermès’ core engine is leather goods and saddlery, still growing in the low teens even as peers stall, with sales up about 12–13% in 2025 on the back of new lines like Arçon, Faubourg Express, and Médor. Each Birkin is made by a single artisan over roughly 18–24 hours; there is no assembly line, which structurally caps supply at an estimated ~100,000 bags per year versus roughly 400,000 for a similarly sized competitor like Louis Vuitton. This enforced scarcity means every bag has a buyer, there is no need for discounting, and resale prices stay supported.

The result is that Hermès bags have behaved more like an asset class than a fashion accessory. Estimates put the average appreciation of Birkin/Togo bags at around 14% annually over long periods, with a Birkin 35 in Togo leather now changing hands at roughly €11,600 and pristine models commonly reselling at 2x retail. In practice, Hermès cannot sell dramatically more bags without breaking the model, so incremental profit growth increasingly has to come from cross-selling into adjacent categories (jewelry, homeware, ready-to-wear, and high-end travel goods) to the same ultra price-insensitive client.

2. Cultural Events Over Hype-Driven Marketing

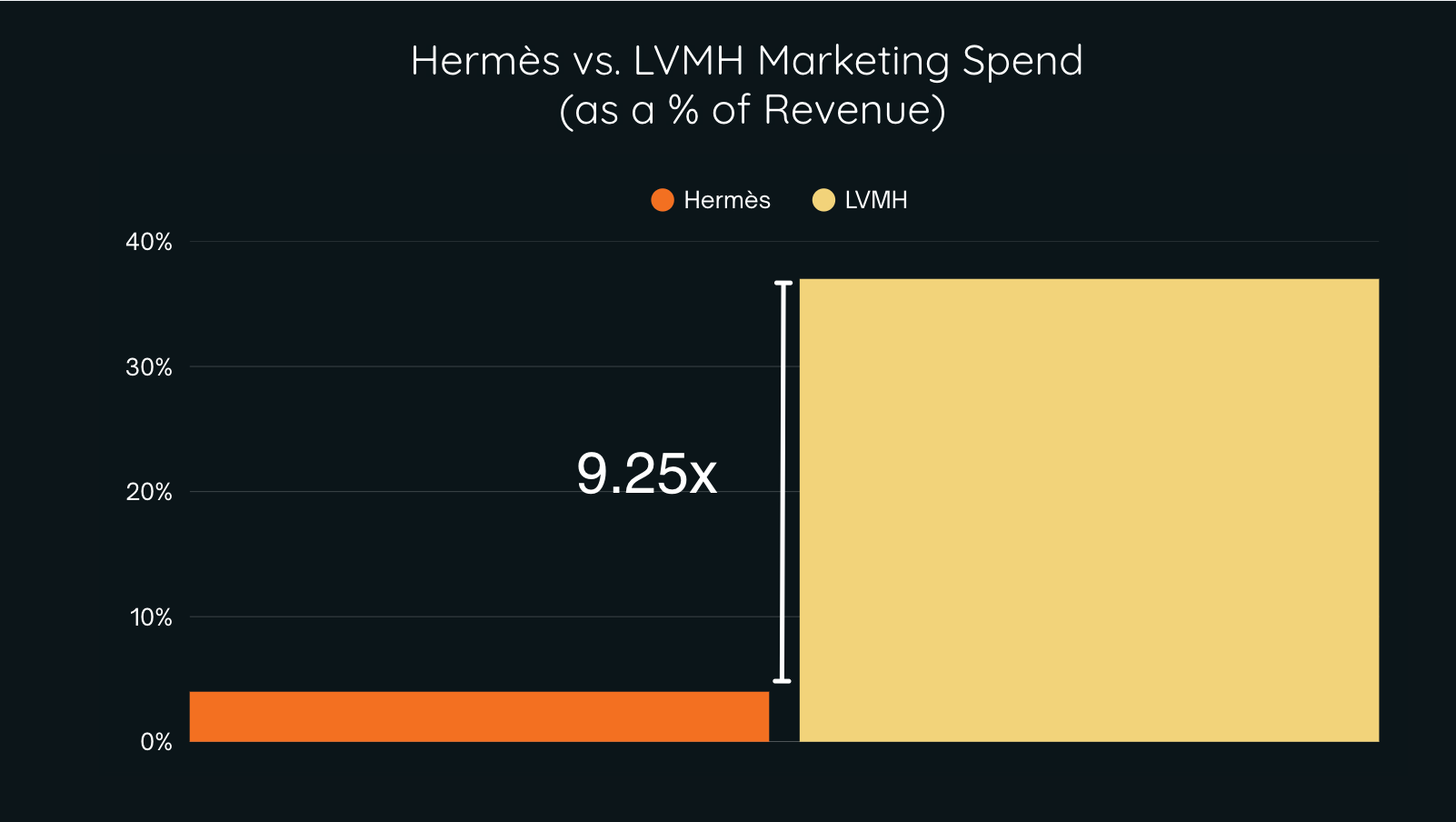

Where most luxury houses spend heavily to rent cultural relevance from celebrities, Hermès has built a system that makes that unnecessary. In 2025, LVMH spent around 37% of revenue on marketing and selling, whereas Hermès spends closer to 4%, yet Hermès still commands the higher multiple and stronger pricing power. The house has no celebrity brand ambassadors, no star “creative director” fronting the brand, and no dependence on hype cycles or influencer-driven trends.

Instead, Hermès invests in cultural events that are structurally on-brand. “Hermès in the Making” lets the public meet artisans and see how materials are transformed, while “Mystery at the Grooms’” stages an interactive, free narrative around the company’s 16 métiers in cities like New York and Tokyo. These are live, traveling proofs of concept for the brand’s core proposition. You aren’t buying stuff, you’re buying craft, time, and story.

3. Category- and Region-Specific Storytelling

Hermès treats fashion and product launches as chaptered narratives rather than isolated runway moments. After the main Paris show, it brings “Chapter 2” of collections to key markets like Shanghai, tailoring silhouettes (elevated streetwear, layered outerwear) to local aesthetics without diluting the brand’s equestrian and artisanal core.

At the same time, it builds category-specific stages:

High jewelry: Exclusive events like “Les formes de la couleur” in Singapore and Tokyo.

Home: Presence at Salone del Mobile in Milan to position Hermès as a serious design house, not a merch afterthought.

Watches: Launched new line at Watches and Wonders Geneva, even as the broader Swiss watch industry cools.

Despite venturing abroad, Hermès stays true to its French and equestrian roots. Since 2011, it has organized Saut Hermès, an annual three-day showjumping competition featuring elite equestrian action.

4. Vertical Integration as a Moat

Hermès’ business model is designed around one idea: control everything that matters to craft and brand, from the farm to the flagship.

In leather goods and saddlery, more than half of production now comes from company-owned or exclusive workshops, with the 24th leather facility opening in L’Isle-d’Espagnac in 2025 and several more slated through 2030. The group also directly manages tanning, textile printing, and parts of watchmaking, expanding its Noirmont site in Switzerland to boost in-house movements and cases.

Hermès has also taken minority stakes in suppliers like the 15% in Lanificio Colombo, an Italian mill known for cashmere and vicuña that has long supplied its shawls and knitwear, securing long-term access to rare fibers without absorbing the family business.

It has rolled out laser marking on hides to trace leather back to farm level extending and is phasing out fossil fuels in new workshops in favor of electrification and renewables.

Vertical integration helps Hermés guarantee quality, scarcity, and supply-chain sovereignty in a world where every other brand is fighting over the same outsourced capacity. Its reliance on local suppliers (74% of production operations in France, 98% of its materials from European suppliers) also makes it easier to navigate the volatile geopolitical and tariff issues.

5. Holding Structure That Is Built for the Long Game

Most public luxury companies are structurally set up to chase quarterly EPS and appease activist investors. Hermès is engineered to ignore that short-termism. The H51 family holding structure and the dominance of the Hermès heirs mean that listed shares are largely non-controlling, which makes hostile takeovers or short-term strategic pivots nearly impossible.

Internally, Hermès reinforces this long-termism with how it treats its workforce. After another year of record results, the company awarded thousands of employees a meaningful profit-sharing bonus (€3,000 per employee in 2025), on top of salary, framing artisans and sales staff as equity-like stakeholders in the brand’s success. That incentive design, layered on top of an industrial system that bans fossil fuels in new sites and wins transparency awards for climate reporting, creates a culture where doing things that “don’t scale” (like one artisan per bag, handsewn saddlestitching that machines can’t replicate) is not a bug but the point.

A Profitable Golden Cage

Hermès is not merely selling handbags, shoes, or scarves, but a scarce, culturally loaded object whose utility is part art, part social signal, and part store of value.

This pure heritage positioning has another advantage in that it effectively makes the company “AI-proof,” for better or for worse. Mechanizing manufacturing or over-optimizing advertising would, if anything, dilute the brand’s mystique rather than strengthen it. Instead, Hermès can introduce AI slowly and invisibly in back-office and analytical workflows, while keeping the client-facing experience resolutely human and artisanal. Many other luxury brands, more dependent on high-volume marketing and with messier internal organizations, stand to benefit more visibly from deploying the technology.

In downturns, that combination of extreme pricing power, tightly controlled vertical production, and a corporate structure insulated from short-term shareholder pressure is exactly what you want to own. While peers cut prices, chase trends, and overextend into wholesale and outlet channels, Hermès can simply keep doing less, better.

Key Risks

Hermès still relies heavily on real leather and exotic skins, and at some point, especially with younger generations, this may become less desirable as sustainability concerns and animal advocacy gain momentum. While Hermès has outperformed many competitors, its core growth engine in Asia-Pacific is facing softer demand and increasingly confident local luxury brands.

Given constrained production capacity, its main revenue lever, price, inherently has limits; beyond a certain point, customers may shift to other houses or adjacent categories. Growth has also been uneven across newer segments, for example, categories like watches have seen more modest traction, in part because Hermès is still primarily known for its leather goods.

In some ways, Hermès has built itself a golden cage: the very scarcity and artisanal constraints that protect the brand also cap its degrees of freedom. But as long as it maintains a category-of-one position in ultra-luxury leather goods, it is likely to remain a very profitable one.

LVMH: A “Recession-Proof” Private Equity Platform

For a deeper dive on LVMH’s strategy, I previously wrote about it here, here, and here.

A PE Fund in Luxury Company’s Clothing

LVMH is essentially a private equity fund in a luxury company’s clothing. Unlike competitors such as Hermès, which emphasize strict organic growth and holding assets indefinitely, LVMH actively prunes and expands its portfolio to optimize returns, much like a PE fund.

It ruthlessly cuts business lines when they are no longer relevant, for instance the disposal of Off-White in September 2024 and the sale of a significant portion of DFS (Duty Free Shoppers) in January 2026 to refocus on more profitable assets. LVMH also doubles down on winners, raising its stake in Loro Piana to 94% by acquiring an additional 9% from minority shareholders for €1.0 billion in July 2025. It seeks to consolidate control of the luxury market as a whole, successfully acquiring players like Tiffany & Co. and unsuccessfully attempting to take over Hermès.

More recently, LVMH entered a strategic agreement in September 2024 to acquire up to a 22% stake in Double R, the holding company controlled by Moncler CEO Remo Ruffini. This indirect structure allows LVMH to back a “winner” and gain exposure to Moncler’s growth while keeping the founder firmly in charge, a classic PE-style growth equity playbook.

LVMH is also quietly centralizing its supply chain and technology stack, using agentic AI and digital supply chain twins to model factories and inventory in real time, with the goal of boosting efficiency, widening margins, and stripping out redundancies.

This strategy is well-suited to fast growth and internal hedging. Strength in Jewelry and Beauty has offset softness in Fashion & Leather and Wines & Spirits, with high jewelry (e.g., Tiffany’s 2025 Blue Book “Sea of Wonder”) and new beauty launches such as La Beauté Louis Vuitton acting as incremental growth engines. Sephora, an atypically “mass” brand in the LVMH portfolio, can be read as a feeder: it pulls in younger and more price-sensitive customers at the top of the funnel, then funnels a subset into more premium, higher-margin offerings.

Culturally Relevant Experiences as the Demand Driver

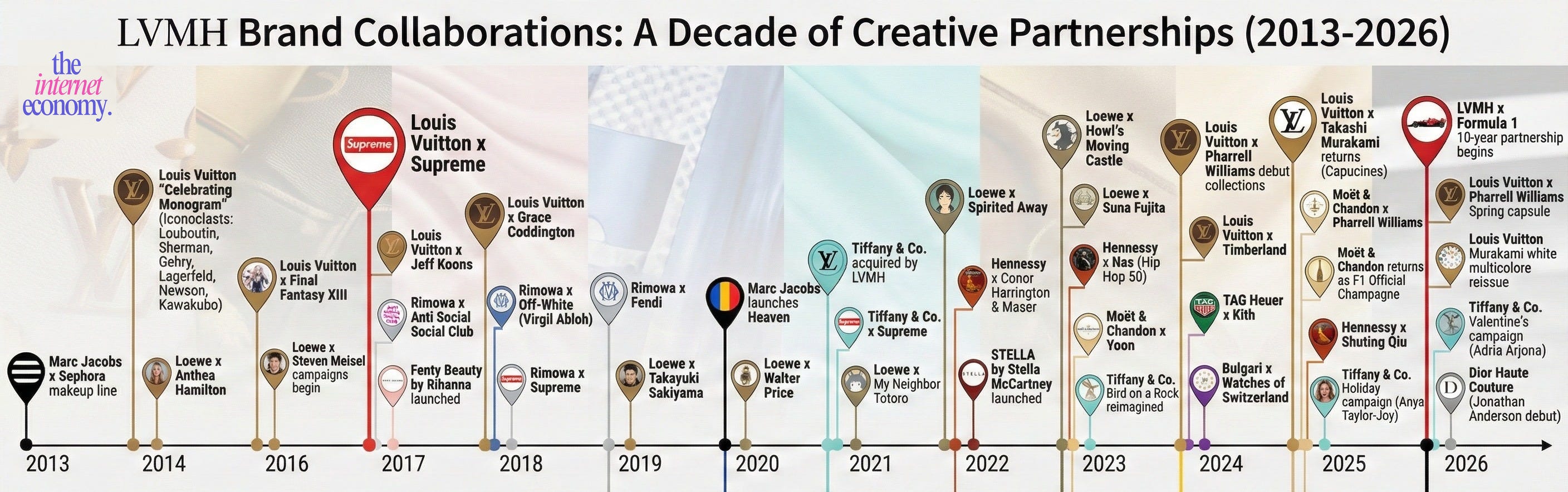

Unlike Hermès, LVMH relies heavily on celebrity ambassadors, acquisitions, and cultural events to maintain relevance. You can think of it as a solid heritage base that stays current by associating with culturally timely brands and personalities. This is both a blessing and a curse: it is expensive, and audiences are fickle. Cultural trends can turn quickly, as we saw with hype cycles around names like Supreme and CryptoPunks.

On the other hand, collaborations allow LVMH to borrow cultural relevance without tying itself too deeply to any single underlying brand. If a brand or celebrity loses momentum, LVMH can simply let the partnership lapse and pivot to the next one.

The next decade in luxury will be increasingly defined by experiential offerings. Consumers have shifted toward valuing experiences over products, and luxury brands have been quick to follow. LVMH is pushing this to the next level.

While the losses from this category are substantial (recurring operating losses of roughly €491 million in “Other activities and eliminations” in 2024), it is a core part of brand building and long-term desirability. Experiential highlights include:

LVMH as an Official Partner of Formula 1 under a landmark multi-year global partnership.

Cheval Blanc and Belmond, its luxury hotel brands, with locations in Paris, the French Alps, St-Tropez, the Maldives, the Caribbean, and upcoming properties in Dubai (2029) and Porto Cervo, Italy (2026).

A strategic partnership with Accor to revive and develop the historic Orient Express brand.

Ownership of Royal Van Lent, a high-end yacht builder, rounding out the ultra-luxury travel and leisure ecosystem.

Even with a roughly $100 million annual Formula 1 deal and a strong presence at the Paris Olympics, there is still a noticeable gap in the sports/lifestyle vertical that LVMH could fill.

From the outside, two experiential gaps stand out:

Lifestyle/high-end sports gap

LVMH could begin investing in unique experiential and real estate assets like members-only tennis clubs. Tennis, in particular, is seeing renewed interest among millennials and younger cohorts; it is simultaneously a lifestyle, an experience, and a real estate play. More broadly, there is room to build around the “top 10 elitist sports” cluster: polo, yacht racing/sailing, equestrian, golf, fencing, rowing, tennis, alpine skiing, squash, and Formula 1, as branded ecosystems rather than just sponsorships.1:1 hospitality offerings

Beyond existing hospitality investments such as Cheval Blanc and Belmond, there is an opportunity in ultra-niche travel destinations for VIP clients, think Lapland, a popular choice among Asia-Pacific consumers and celebrities. Imagine ultra-high-end, fully serviced properties owned by LVMH, effectively “black-card Airbnb” experiences gifted or reserved for top clients only. Standard luxury experiences will not be enough; they will need to be luxury experiences that no one else can access.

Recent examples of this “elevated experiential” strategy include the reopened Milan Louis Vuitton flagship and immersive concepts like the Blue Box Café in New York, which combine retail, dining, and cultural programming. The Da Vittorio Café Louis Vuitton and DaV by Da Vittorio restaurant meld simplicity with refinement, pairing “luxury snacking” with three‑Michelin‑star cuisine and reimagined classics like osso buco with saffron risotto served in the shape of the Louis Vuitton Monogram flower. These openings sit within a broader elevation strategy at Tiffany & Co., which has renovated nearly a third of its network to enhance brand desirability and the quality of the customer experience.

The risk is that LVMH cannot afford to get sloppy. Acquisition for acquisition’s sake will not work in a slowing luxury cycle. The group also reported around €1.065 billion in losses from exchange rate fluctuations, which raises uncomfortable questions about why FX hedging was not more effective given its scale, geographic footprint, and relatively predictable currency exposures. For an operator this sophisticated, failing to better mitigate known FX risk feels like an unforced error.

PRADA: The Miu Miu Success Story

Prada Group enters 2026 in an unusually strong position: €5.4bn in revenue (+17%), €1.28bn in EBIT (+21%), a 23.6% EBIT margin, and net cash of around €600m after four straight years of double-digit like-for-like growth.

Structural Challenges

The group is now a two-speed machine: Miu Miu in hypergrowth versus a Prada “mothership” that is solid but slower (low single-digit growth or slight decline, depending on the period). If Miu Miu’s aesthetic moment cools, as fashion moments always do, the group needs Prada to carry more weight than it currently does.

A second issue is self‑inflicted: the Versace acquisition adds complexity and near-term margin drag. Prada is giving up a near-pristine balance sheet and taking on real execution risk.

Strategic Response

First, Prada is keeping Miu Miu’s engine running. Miu Miu is being treated as the group’s primary growth engine. Its “schoolgirl chaos” aesthetic (micro‑minis, ballet flats, shrunken knits, exposed lingerie) has become a dominant cultural reference, driving extraordinary retail momentum. The brand maintains the momentum via cultural programming: Women’s Tales films, Literary Clubs, Atheneum pop‑ups, and collaborations like New Balance × Coco Gauff. A new series of pop‑up stores across Asia this spring is designed as fully immersive spaces that pull consumers deeper into the Miu Miu universe. On top of that, the L’Oréal fragrance launch (“Miutine”) pushes Miu Miu into beauty and adds a high‑margin royalty stream to the growth engine.

Second, Prada is raising the “mothership” growth rate without breaking it. The Prada brand is being managed for durable desirability revitalising icons like the Galleria bag, adding new leather goods lines (Explore, Etude, Dada), and using cultural platforms (Prada Mode London, Art Basel activations such as “30 Blizzards”) to stay intellectually relevant rather than chasing viral trend cycles.

Third, Prada is using Versace as its big portfolio bet. It bought the brand at a distressed price (around €1.25bn EV, funded with roughly €1.5bn of new debt) and is attempting a clean identity reset. Donatella has stepped down and Dario Vitale (formerly design lead at Miu Miu) is in place to rebuild product and relevance, with early buyer reception reported as strong. Governance signals long-term intent with Lorenzo Bertelli installed as Versace’s chair. Near term, Versace is likely to drag margins, while medium term the upside is a non-overlapping customer base and a stronger Americas mix.

Fourth, Prada is doubling down on brand control. It is using its own stores and in‑house production to defend full-price selling, manage distribution tightly, and build a tight loop between physical retail and digital touchpoints where events and hospitality create emotional pull, and directly operated stores capture both the transaction and the data.

Prada’s ultimate edge is control, built on three pillars:

Around 90% of revenue comes from directly operated stores, enabling pricing discipline, control of the brand environment, and customer‑data ownership with minimal wholesale leakage.

26 owned factories provide vertical integration that protects quality, speed, and supply stability, and create a clear integration path for Versace manufacturing.

A historically strong balance sheet (net cash pre‑deal) gives the group room to absorb a turnaround without starving its core brands.

This is why comparisons to “Italy’s LVMH” keep surfacing, but the model is narrower and more focused: a small portfolio of distinct identities sharing infrastructure, not creative voice.

Richemont: Narrow, Hard-Luxury Powerhouse

Richemont, owner of Cartier, Van Cleef & Arpels and Buccellati, enters 2026 as the hard‑luxury benchmark. Jewelry and watches are carrying the group through a messy macro environment, with growth still solid even as cost inflation and weaker China demand drag on performance. The core tension is that the portfolio is compounding, but each incremental euro has to work harder against higher gold prices, a strong Swiss franc and patchy demand across Asia.

What makes Richemont interesting is how well its structure fits this moment. Jewelry is the engine. Cartier, Van Cleef & Arpels and Buccellati, now joined by Vhernier, have become an industrial compounding machine, with high single‑ to mid‑teens growth at constant FX and operating margins in the low‑30s even after the spike in gold. The playbook is deliberately conservative: rely on “timeless” platforms such as Panthère and Alhambra, then punctuate them with jewelry events and one‑off pieces.

Presenting these collections in the right way is key. Cartier stages invite‑only En Équilibre presentations, Van Cleef & Arpels builds full worlds around collections like l’Île au Trésor, Buccellati hosts intimate gatherings in Italy, and Vacheron Constantin, on the watch side, places an elaborate piece such as La Quête du Temps in the Louvre, turning it into a culturally situated object where history, craftsmanship and engineering are read together. That mix of timeless product and well-curated cultural experience is precisely what very wealthy clients are paying for.

Richemont has also rebuilt its operating model around control. Roughly three‑quarters of revenue now comes from its own boutiques and e‑commerce, with retail growth outpacing wholesale. That gives the group much tighter grip on pricing, assortment and client experience than wholesale‑heavy models that peers are still trying to unwind. Regionally, it is leaning into depth where demand is resilient, focusing on local clients in the US, Japan and the Middle East, while treating Greater China as a market to manage rather than a growth crutch and accepting that recovery there will be gradual and uneven. Underneath sits a fortress balance sheet. Net cash at year‑end 2025 is in the mid‑single‑digit billions, and Richemont has used that position to keep Capex elevated in jewelry manufacturing and flagship boutiques, acquire assets such as Vhernier, fund the clean exit from YNAP, and still pay dividends and buybacks while remaining in net cash.

Structural Challenges

Richemont’s main operational concern is not Cartier’s jewelry watches, but its standalone Specialist Watchmakers division, which includes IWC, Panerai and Vacheron Constantin. A strong franc, higher precious‑metal costs and softer volumes are moving through a largely fixed‑cost base and squeezing profitability, which in turn weighs on group margins.

At the same time, the long tail of fashion and accessories, including Chloé, Dunhill and Alaïa, remains loss-making, even if those losses are narrowing. That reinforces the idea that Richemont’s natural home is hard, not soft, luxury.

Strategic Response

Richemont’s response is unusually disciplined for a listed group. Rather than chasing volume, it is leaning on the equity of its maisons to implement “balanced and targeted” price increases and is explicitly prioritizing unit economics over headline growth.

On the cost and capacity side, it has resisted the reflex to cut capex. Instead, it is pushing more investment into jewelry manufacturing through new workshops, expanded lines, craft training and selective flagship upgrades in key cities, keeping the retail network high‑quality and curated rather than ubiquitous.

The exit from Yoox Net‑a‑Porter in 2025, via a sale into Mytheresa’s LuxExperience platform, a clean deconsolidation and a one‑off hit from discontinued operations, is part of the same functional discipline. Hard luxury has been put back at the centre, platform risk has been externalized and the P&L has been de‑cluttered.

Heading into 2026 and beyond, Richemont’s thesis is intentionally narrow. Instead of trying to match LVMH’s breadth or Kering’s fashion‑turnaround story, it is effectively betting that controlling the leading jewelry maisons, a tightly curated set of prestige watch brands and most of its own distribution is enough to ride out a volatile decade.

Chanel: A Surprisingly Innovative Heritage House

Chanel enters this slowdown as one of the few truly global, fully independent mega-brands in luxury. Ready-to-wear, leather goods, watches, jewelry, and beauty all sit under a privately held, debt-free structure, which gives the house more freedom than listed peers to invest through the cycle rather than defend quarterly margins.

Structural Challenges

Chanel is navigating a cyclical slowdown from a position of strength. After years of aggressive pricing, demand is softening among aspirational clients. In 2024, operating margins fell to roughly 24% from the low-30s, with operating profit down about 30%, even though the brand still generates strong cash.

The issue is not brand desirability, but rising expectations. As customers buy fewer pieces, every product, interaction, and experience has to feel earned. Luxury is no longer forgiven for friction, whether digital, physical, or experiential.

Chanel’s structure gives it room to respond differently. The house is privately held, debt-free, and insulated from quarterly market pressure. Instead of defending margins, 2024 became a year of higher investment (Chanel’s latest reporting period), with a clear step-up in capex and spend on brand support, real estate, and craft.

Headcount rose from about 36,500 to more than 38,400, even as peers froze hiring. Chanel has committed to net-zero emissions by 2040, sourced 99% of its electricity from renewables in 2024 with a target of 100% in 2025, and continued upgrading boutiques to higher environmental standards. The signal is long-term intent, not short-term optimization.

Strategic Response

Chanel’s strategy is focused and selective.

First, investing through the downturn. Capex rose sharply as the house expanded boutiques and flagships, including a Watches & Fine Jewelry store on New York’s Fifth Avenue and CHANEL & moi – Les Ateliers in Seoul, and scaled CHANEL & moi care and repair services globally. Those Ateliers focus on care, repair, and longevity, reinforcing the idea that Chanel pieces are maintained, not just sold.

Second, using AI where it actually moves the needle. Chanel is using AI to remove purchase friction and win attention in crowded feeds:

Lipscanner (beauty shade-matching + AR try-on): +32% lipstick conversion and –27% return requests tied to shade mismatch; reported 1.2M+ downloads and strong app-store ratings, turning color uncertainty into a unique advantage.

Storyteller Nail (generative creative at scale): generated 45,000 shade-specific micro-stories; nearly tripled view duration (to ~8 seconds), lifted click-through, and increased add-to-cart, making ads feel personal without diluting brand control.

Conversational assistants (service + internal copilot pilots): handled a majority of routine inquiries end-to-end, improved first-contact resolution, reduced handle time, and increased CSAT; also reclaimed hours weekly for boutique teams by reducing manual lookups. (The strategic point: AI protects the “impeccable service” promise while scaling.)

Third, making physical retail culturally relevant again. Chanel is staging specific, unflattenable moments rather than generic shows, from the Métiers d’art collection in Hangzhou, inspired by coromandel screens, to Cruise repeat shows in Hong Kong designed to create local cultural heat, not just global impressions.

Fourth, expansion with intent. In 2025–2026, Chanel is expanding in India and Mexico and adding boutiques across Mainland China, Japan, and Canada, positioning stores as destinations as much as transactional spaces.

Fifth, securing savoir-faire and innovation. Chanel continues to invest in innovation infrastructure, partnerships with institutions such as the MIT Media Lab, internal entrepreneurship programs, and selective external stakes. Its 25% investment in independent watchmaker MB&F, following earlier stakes in Romain Gauthier and F.P. Journe, is about protecting high-end watchmaking capabilities and keeping access to rare skills inside the ecosystem.

Kering: A Prime Example of What Can Go Wrong

Kering enters 2026 as the laggard among the global luxury groups. Once defined by Gucci’s outperformance, it now faces falling sales, collapsing profits, and a portfolio whose desirability has slipped just as the market has become more polarized between true ultra‑luxury and everyone else.

Structural Challenges

Kering is a prime example of what can go wrong in modern luxury when brand equity and positioning slip. Group revenue fell 13% in 2025, and net income attributable to the group dropped more than 90%, far worse than the broader sector, even though it faces the same Asia–Pacific cooling as peers.

The core problem is brand desirability across the portfolio. Gucci has lost momentum with core and aspirational clients. Alexander McQueen is in restructuring and has seen a “sharp decline in footfall” and Balenciaga is no longer generating previous levels of interest, with Kering explicitly stating that it needs to revive interest in the house and acknowledging that the prior creative direction did not capture demand in a more polarized, uncertain environment.

Kering is also over‑indexed to aspirational rather than ultra‑high‑end clients, the segment that has cooled the most, and has historically relied more on wholesale than the likes of Hermès, LVMH or Richemont. Gucci deliberately cut wholesale revenue by 34% in 2025 to limit access to only the most exclusive accounts, accepting a near‑term revenue hit to try to rebuild scarcity and elevate the brand. At the same time, the broader luxury market is shifting incremental innovation from pure product to experiences, hospitality, dining, travel, events, where entertainment, emotion and ethics matter as much as the object itself, and Kering has been slower to build that layer at scale.

Kering is over-indexed to aspirational (vs ultra-luxury) clients, the segment that has cooled the most, and has relied more heavily on wholesale than peers. Gucci deliberately cut wholesale revenue by 34% in 2025 to limit access to only the “most exclusive accounts,” accepting short-term revenue loss to elevate the brand. In parallel, the wider luxury market is shifting innovation from pure products to “experiences” (hospitality, cruises, fine dining), emphasizing entertainment, emotions, and ethics over goods alone.

Strategic Response

In response, Kering is executing a multi-pronged transformation it describes as “flawless execution” of a new roadmap.

First, creative shock therapy at the flagship brands. Kering is attempting to reset its two most important fashion houses with high‑profile creative appointments. Demna, formerly synonymous with Balenciaga, became Gucci’s Artistic Director in March 2025, and his debut “La Famiglia” collection has been credited internally with sparking renewed interest in the brand. In parallel, Pierpaolo Piccioli, ex‑Valentino, was appointed Artistic Director of Balenciaga in May 2025 to steer the house back toward growth and away from a more polarizing phase.

Second, a governance and leadership overhaul. In September 2025, Kering split the roles of Chair and CEO, appointing Luca de Meo as Group CEO while François‑Henri Pinault stayed on as Chair. One of de Meo’s first moves was to put Francesca Bellettini, Kering’s long‑time Deputy CEO and head of Saint Laurent, in charge of Gucci as President and CEO, signaling that the group’s most important asset will now be run by one of its most operationally minded leaders.

Third, a strategic pivot in beauty. In October 2025, Kering agreed a long‑term strategic partnership with L’Oréal and sold Kering Beauté, including Creed, for roughly €4 billion. In exchange, its brands secured multi‑decade beauty licenses, effectively swapping in‑house execution risk for a high‑margin royalty stream and immediate balance sheet repair.

Fourth, asset management and vertical integration. Kering has been reshaping its asset base at both ends of the value chain. It sold stakes in prime properties on Paris’s rue de Sèvres and New York’s Fifth Avenue to Ardian while retaining a significant minority interest, freeing up capital without fully exiting strategic locations. On the production side, it has moved to secure more of the value chain in hard luxury, signing an agreement to acquire Raselli Franco Group, one of Europe’s leading independent jewelry manufacturers, and buying eyewear suppliers such as Visard and Lenti to strengthen Kering Eyewear’s integrated model.

Fifth, operational rationalization and channel control. Gucci closed a net 25 stores in 2025 and is shutting outlet locations to focus on “highly exclusive venues.” At group level, wholesale revenue fell nearly 20% as Kering aggressively cut third‑party retailers to push more business into its own network, again choosing near‑term pain in service of tighter brand and pricing control.

As the group enters 2026, management is framing this as the start of a multi‑year reset: a leaner, faster Kering that has to rebuild brand desirability, regain control of distribution and mix, and gradually rebuild margins and cash generation rather than relying on the easy growth of the last cycle.

Moncler: Between Resilient and Stuck

Moncler enters 2026 as a solid but not spectacular performer in luxury. It has largely held revenues flat while others have swung from boom to correction, but it has not broken out the way true ultra‑luxury winners have, and its growth engine is starting to sputter.

Structural Challenges

Moncler Group sits in the middle tier of luxury performers heading into 2026. It has avoided the sharp revenue and profit declines seen at players like Kering, but it is not matching the structural momentum of houses such as Hermès or Richemont.

The immediate issue is stagnating growth. For the first nine months of 2025, group revenue was down about 1% reported and essentially flat at constant exchange rates. Two things explain most of that stall. Tourism weakness hit EMEA and Japan, weighing on the Moncler brand, which still over‑indexes to traveling luxury customers. At the same time, the group is deliberately sacrificing wholesale revenue as it cleans up distribution and elevates positioning. Moncler brand wholesale fell around 5% at constant FX, with Stone Island down more, creating a short‑term drag on the top line.

Beneath the numbers, there is a more structural question. Moncler’s technical innovation has, to some degree, become normalized. As high‑end outdoor brands such as Arc’teryx expand consumers’ choices in performance outerwear, some customers are asking whether €1,000‑plus price points for Moncler are still fully justified. At the same time, the brand has edged close to hype saturation, a place that has historically been dangerous for long‑term equity, as seen in prior cycles at street and “hypebeast” names like Supreme or NFT‑driven drops. The recent “Warmer Together” campaign, built around heritage pieces like the Maya 70 and Bretagne with a message that “warmth was never about the outside”, is a conscious pivot back toward function, warmth and human connection over pure hype.

Structural Positioning

Moncler’s resilience is rooted more in structure than in growth. The group plays in “luxury performance,” a category that tends to hold up better than pure fashion when sentiment tightens, because cold‑weather function is a real need as well as a status signal. Nearly 90% of Moncler brand sales come from direct‑to‑consumer channels, and the group reports gross margins above 78%, giving it far more control over pricing, experience and data than wholesale‑heavy peers. Net cash of roughly €1.3 billion gives Moncler the balance sheet to accept short‑term revenue pressure without compromising strategic choices.

The two‑brand architecture adds another layer of protection. Moncler and Stone Island speak to different audiences, global luxury performance versus technical street culture, which allows the group to manage different cycles and aesthetics without over‑relying on a single “it” moment.

Strategic Response

Moncler’s response is focused rather than reactive.

First, it is accelerating DTC and accepting near‑term pain. Moncler is continuing to push more of the business into its own stores and digital channels and to prune wholesale aggressively in both brands. That weighs on reported growth, but it tightens control over price, assortment and brand environment. The strategy is already showing up in the Americas, which outperformed other regions in the latest period, driven by solid direct‑to‑consumer demand in the US.

Second, shifting from hype to community obsession. The group is trying to reframe Moncler around belonging and lived experience rather than constant drops. The Moncler Grenoble Fall/Winter 2026 show in Aspen, staged as a nighttime snowmobile ride through the forest to a snow‑covered mountain runway, is a blueprint: a physically exclusive event for the brand’s global community that generates durable cultural value and organic digital reach, instead of a one‑off stunt.

Third, re‑anchoring the brand in purpose and performance. The aforementioned, “Warmer Together” marks a deliberate move away from pure hype dynamics and back toward emotional relevance and functional credibility, reminding customers that Moncler earned its pricing power by keeping people warm in extreme conditions as much as by being seen in the right places

In short, Moncler’s problem is flat growth and more volatile tourism flows at a time when its once‑distinct technical edge feels less unique. It is countering that with a mix of DTC acceleration, tighter distribution, and extreme experiential marketing that leans into community, heritage and performance rather than chasing the next hype cycle.

The Forces That Will Matter in Luxury

Sustainability May Be Overrated

Over the past decade, luxury has treated sustainability as both a moral obligation and a competitive superpower. Heading into 2026, it looks more like regulated hygiene than a real growth driver. The brands winning on revenue and market cap are not the ESG darlings, and looming rules like the EU’s Digital Product Passport are turning “green” from a differentiator into a simple licence to operate.

Regulation is now closing in. The EU’s Digital Product Passport (DPP) regime, expected to be mandatory by 2030, will require brands to assign each product a scannable digital ID capturing origin, materials, manufacturing and recyclability. That will lift traceability expectations and compliance costs, but it also pushes sustainability further into the realm of licence‑to‑operate rather than a source of incremental growth.

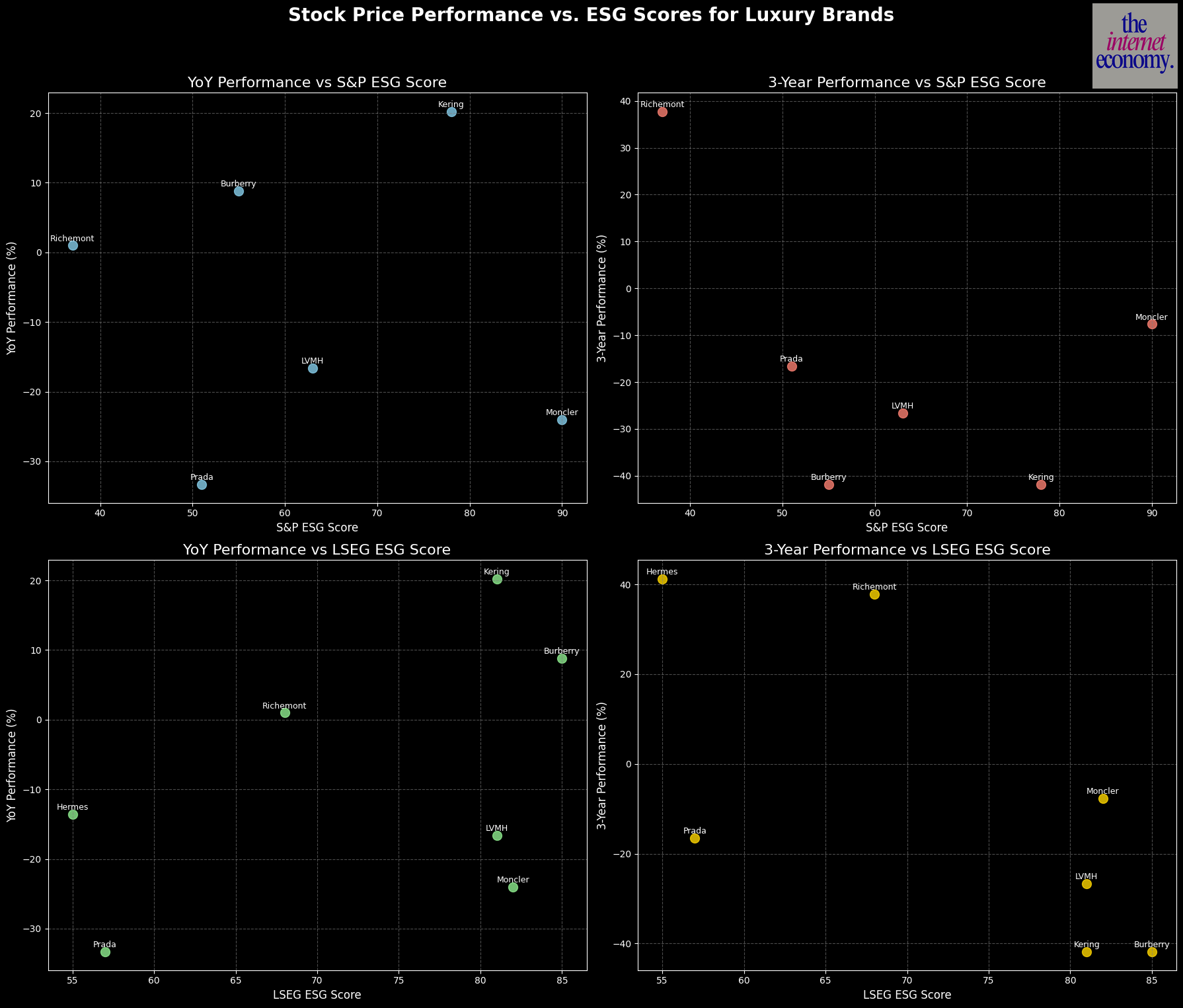

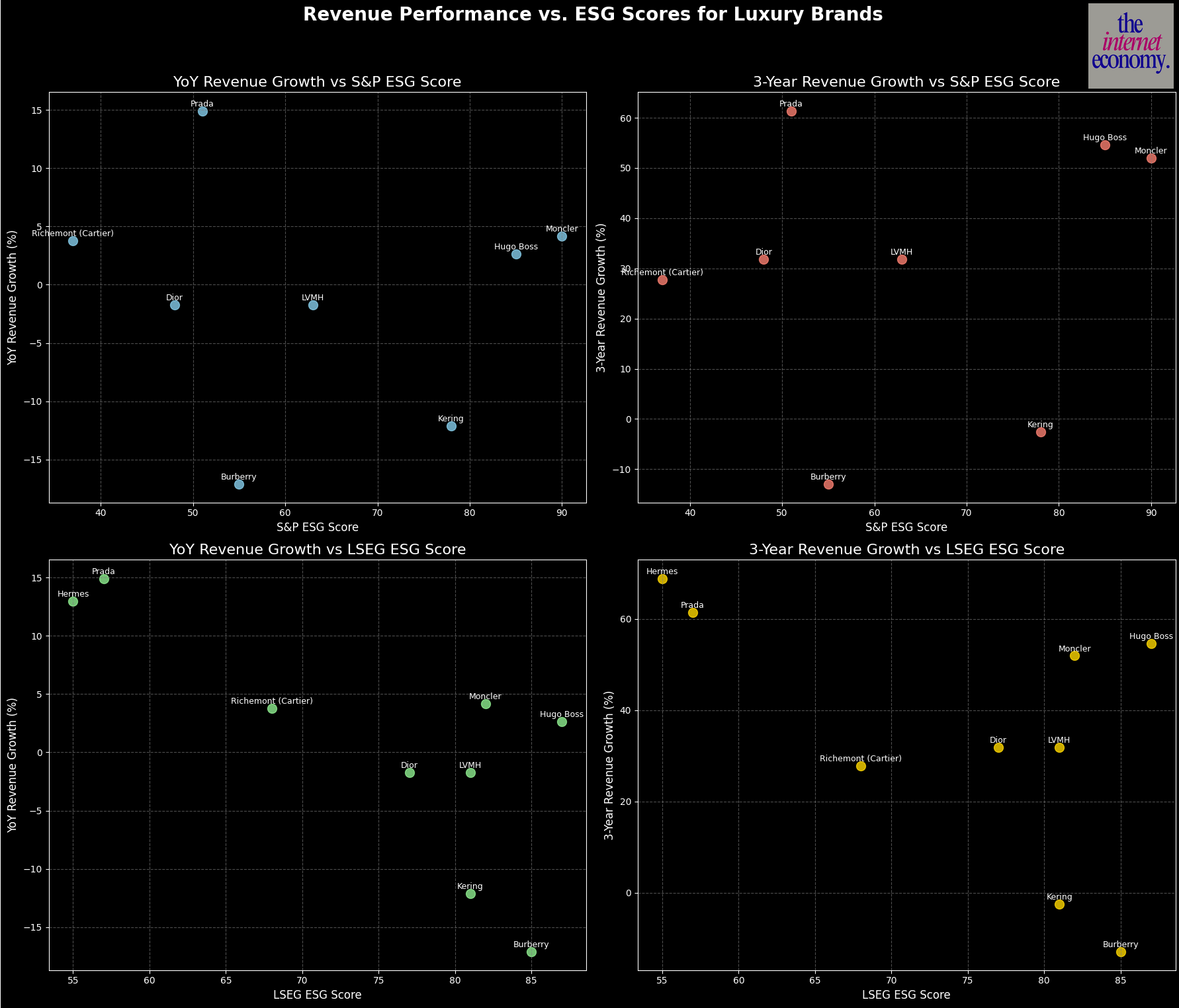

The market data tells a similar story. Across major listed luxury names, there is no meaningful positive correlation between ESG scores and either revenue growth or share‑price performance; when you plot LSEG and S&P ESG scores against 1‑ and 3‑year returns, you see something closer to the opposite, with lower‑scoring ESG names often outperforming over three years. Hermès, Prada and Richemont, three of the strongest stock and revenue performers of the last few years, sit near the bottom of the ESG rankings table in 2025.

The same pattern holds when you run the numbers against revenue growth, no statistically significant positive relationship, and a visible negative trend line where higher ESG scores often map to weaker top‑line performance. Consumers may say sustainability matters at the checkout, but in aggregate they still reward desirability, scarcity, and execution first.

Against that backdrop, the sustainability strategy of the major houses going into 2026 looks less like a commercial bet and more like regulatory and operational inevitability. LVMH’s LIFE 360 roadmap is a good example: by 2026 it targets zero virgin fossil‑based plastic in customer packaging, a 50% cut in energy‑related emissions versus 2019, 100% renewable or low‑carbon energy for stores and sites, and full certification of “strategic” raw materials, with all new products carrying a customer information system, effectively a proto‑DPP layer, and all staff trained on environmental issues via the LIFE Academy.

Hermès is taking an even more supply‑chain‑centric route, aiming by 2026 for all raw materials to be deforestation‑ and conversion‑free, with strict policies for leather, wood, rubber, palm and soy and a 2020 cut‑off date baked into supplier contracts, backed by certifications such as FSC and LWG. Chanel, meanwhile, is pushing industrial circularity: by 2026 it plans for roughly 30% of handbags and 50% of shoes to use recycled structural components, has launched “Nevold” to recycle cotton, wool, silk and cashmere at scale, and is working toward eliminating plastic components from shoes and bags entirely.

At the industry level, 2026 is essentially a dress rehearsal for mandatory DPPs. Groups like Kering, Moncler and Richemont are building digital product registries to comply with the EU’s Ecodesign for Sustainable Products Regulation, which will require each item to carry a verified data trail on origin, composition and recyclability; Moncler, for example, has already moved beyond 50% recycled nylon by 2024 and is formalising “thinking circular” as a core operating principle, with the critical work happening in PLM, ERP and traceability architecture rather than in slogans.

Where sustainability may actually start to matter, commercially, is not in first‑sale demand but in supply chain economics and secondary-market value (something I’ve previously covered here). On the cost side, brands that can see and renegotiate their upstream exposure, think agentic AI systems dynamically repricing logistics, materials and freight contracts – will have an advantage far more tangible than any ESG badge.

LVMH’s recent struggles in its wine and spirits division are a reminder that when supply chains misfire or demand shifts regionally, you cannot recycle your way out of a margin squeeze; you have to re‑route inventory, reset terms and re‑plan production in real time. On the revenue side, Digital Product Passports open the door to authenticated resale at scale: if a bag carries a cryptographically secure, DPP‑linked provenance record from day one, its residual value can be higher and more liquid, reinforcing pricing power and desirability over the long term even if it never appears as “sustainability revenue” on a P&L.

So the paradox heading into 2026 is this: sustainability is non‑optional and increasingly codified in law, yet the brands delivering the best financial outcomes are not the ones scoring highest on ESG indices. The real battleground is shifting to supply chain and data: who can build the infrastructure to comply with DPP, strip cost out of complex networks and turn traceability into higher resale value. At the same time, the front end still has to stay focused on what has always moved luxury: product, story and status.

AI as a Means, Not the End

For luxury, the AI play is narrower than in mass fashion. AI will mostly live in back‑end efficiency rather than front‑end marketing, because a high‑touch, human creative layer still defines campaigns and clienteling.

For conglomerates like LVMH, AI is already improving supply‑chain performance via predictive routing, regional vendor‑risk analysis and sharper inventory and demand forecasting. Several houses are also training models on their archives to help designers generate brand‑native ideas, a pattern I flagged in 2023. Online customer service remains a weak point for many luxury brands, and AI agents will not only raise baseline service quality but also enable new concierge‑style experiences that remember preferences and history for VIP clients.

In some ways, luxury brands are not moving fast enough. Third‑party AI personal‑shopper platforms like Daydream (essentially “Pinterest meets Amazon for fashion discovery) risk inserting themselves between maisons and their customers, and are already aggregating behavioural data across thousands of brands at a scale individual houses cannot match. The brand that controls the richest data will have the edge in the age of AI, and while ultra‑high‑net‑worth clients may stay with in‑house advisors, more price‑sensitive aspirational shoppers can be steered toward whichever label is best surfaced, or discounted, by these intermediaries.

AI also adds a new dimension to advertising strategy. On one side is Generative Engine Optimization, where the goal is to be the brand that AI shopping agents and chat‑search surfaces recommend, driven by user sentiment, reviews and material‑quality signals. On the other is physical experience, and as content gets commoditized by AI, live shows, installations and in‑store theatre become even more important differentiators that algorithms can point to but not replace.

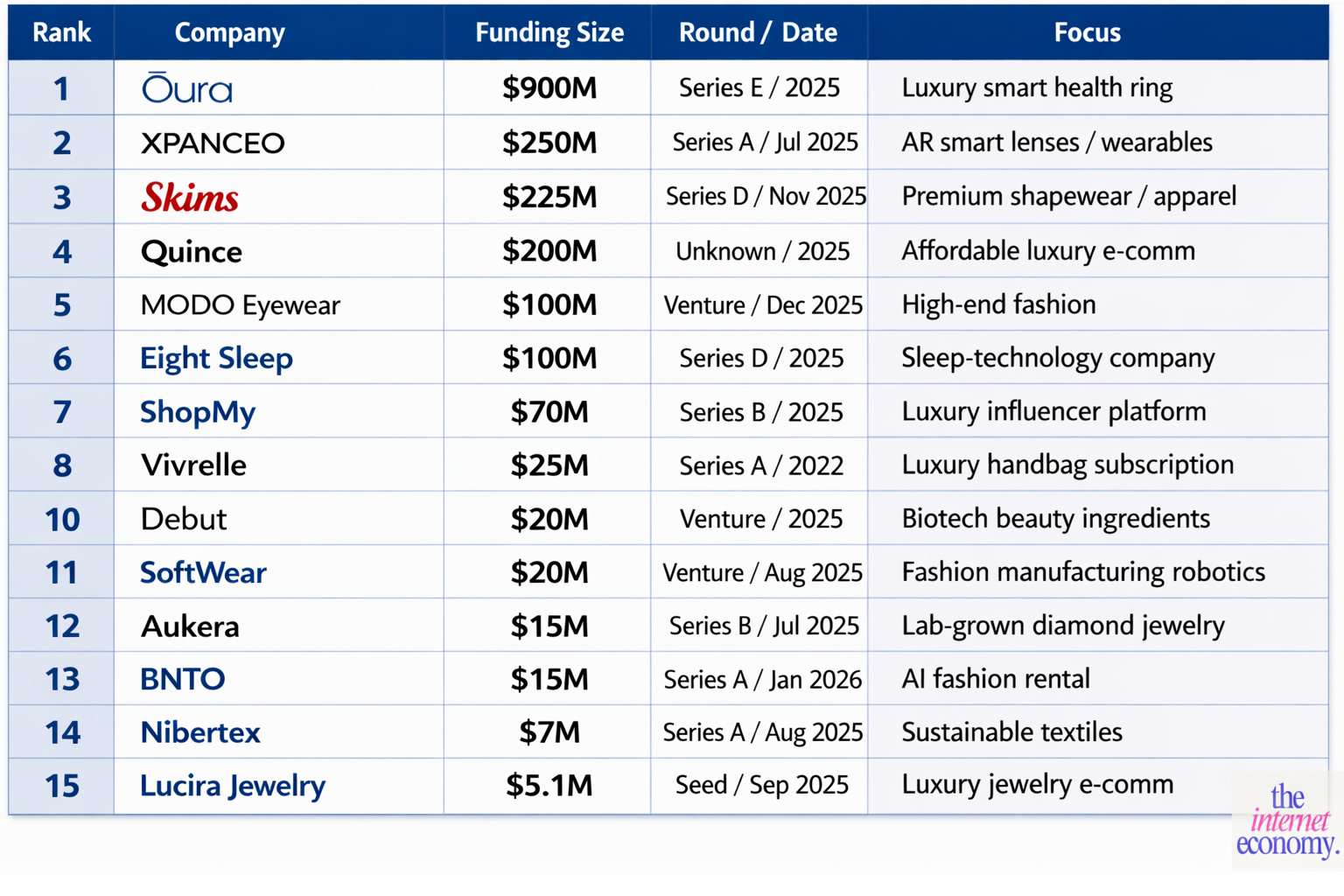

Funding flows suggest where AI’s impact will show up first, in infrastructure around luxury rather than in the maisons themselves. Oura, XPANCEO, Eight Sleep, SoftWear, BNTO and Nibertex sit in health data, AR lenses, sleep optimization, robotics, AI‑enabled rental and advanced textiles, and have raised far larger rounds than pure “luxury content” startups, underscoring that the early value is in materials, supply chain and data pipes rather than campaigns. If conglomerates do not build or partner into this stack, these intermediaries will own the customer insight and the AI‑driven margin upside. LVMH’s own 2025 Innovation Award slate points in the same direction: the highlighted startups cluster in AI and data intelligence (Kahoona, OMI), sustainability and circularity (Genesis, Aectual), and supply‑chain and media infrastructure (Authena, Ircam Amplify), not front‑end storytelling tools.

For luxury brands, the end goal with AI is straightforward: expand margins and redeploy the savings into experiences, more distinctive product, better service and richer physical worlds that preserve the category’s scarcity and status.

Where Luxury Goes Next

At the end of the day, luxury is not leather, diamonds or watches. From first principles, luxury is something scarce, something we do not see often. There are two attributes that matter most, desirability and scarcity. A desirable but non‑scarce good like air is not a luxury, and a scarce but non‑desirable good, like an out‑of‑fashion logo‑heavy sweatshirt, is not either. Luxury brands can manufacture desire or manufacture scarcity, but the winners pull on both levers.

The next wave of luxury startups will emerge in the gaps legacy houses cannot or will not fill. One group will build local luxury on Asian cultural codes rather than imported European ones. Another will act as experience facilitators, designing elitist but modern clubs (tennis, racquet sports, wellness) and unique destination real estate such as Lapland‑style retreats for VIPs. A third will be tech partners that own the AI layer, offering hyper‑personal concierge, data‑rich personal shoppers and dynamic drops without fully disintermediating the brand.

On the product side, the big white spaces are health as luxury (genome‑ or biomarker‑based beauty, longevity programs, and performance wearables that shift status from “things” to “self”), quiet‑luxury brands built on drop‑only models to limit inventory risk while supporting secondary prices, and a truly superior non‑animal material that can credibly replace exotics for houses like Hermès. These are the next frontiers where innovation meets aspiration, expanding the definition of what luxury can signal.

The target customer for these categories looks less like an old-world logo collector and more like the kind of consumer backing brands such as Gentle Monster, Miu Miu, or Arc’teryx’s Veilance, seeking edge, scarcity, and cultural relevance alongside heritage rather than logos alone. The double-digit online growth projected for Gentle Monster and Miu Miu’s aggressive expansion suggest there is still plenty of room for new tiers of luxury at different price points, as long as the product feels like the right, resonant one.

Strategic Implications by Brand

Hermès:

Keep playing your own game, but push it one notch further into “life system” rather than “object.” Use the 40%‑plus margins and roughly €12.8 billion net cash to keep investing in ateliers, materials science and your forests and zero‑deforestation agenda, while expanding the world around the product with traveling craft exhibitions, Mystery at the Grooms’ style experiences and quietly elite sport and wellness touchpoints that make Hermès feel like a way of living, not just a thing you buy.

LVMH:

Lean into more personality and less clinical perfection. Use high‑brow culture, ideas and unexpected collaborations to speak to younger clients who want to feel intellectually as well as aesthetically engaged, and extend your existing art‑driven flagships and hospitality ecosystems into new resonant formats, from members‑style tennis and arts clubs to ultra‑rare, story‑rich travel residencies for ultra‑VIPs that make the brand feel like a world they briefly inhabit, not just a logo they wear.

Prada Group:

Treat Prada as the thinking person’s Gucci and push harder into that space, high‑brow fashion with an urban edge, while treating Miu Miu less as a fad and more as a movement by listening obsessively to its core customer. The job is to sustain Miu Miu’s momentum, re‑accelerate Prada and turn around Versace without distraction, using your structural advantages in retail control, factories and disciplined stewardship.

Richemont:

Keep doing what you do best, but make it feel even more like culture and even less like retail. Use the jewelry engine and roughly €6.5 billion net‑cash buffer to double down on museum‑grade moments, Cartier and Van Cleef & Arpels jewelry worlds and Vacheron Constantin at the Louvre style exhibitions as the primary marketing channel, while quietly fixing Specialist Watchmakers’ economics with sharper SKU discipline, fewer mid‑tier points of sale and more true haute horlogerie.

Chanel:

Protect the mystique but modernize the interface. Let creative direction lead with material intelligence and silhouette rather than logos, while using AI quietly to remove friction in beauty and clienteling, Lipscanner style tools and CHANEL & moi grade service, without breaking the white‑glove spell. The goal is to make boutiques feel like cultural events and digital touchpoints feel invisible, so desirability, not distribution, remains the centre of gravity.

Moncler:

Move further away from hype‑beast territory and back to your mountain roots. Luxurious Patagonia is a better north star than the next drop; double down on DTC control, experiential shows and technical innovation so you stay ahead of Arc’teryx type competitors and build a brand that feels refined and durable rather than reactive.

Kering:

Go back to your roots, La Famiglia is a good start, and avoid replaying the 2000s hype cycle. You need your Tom Ford moment, which will not come from following trends but from setting them, backed by serious investment in AI and innovation where peers are already ahead.

Put simply, the recent winners have followed a fairly consistent playbook across different positions in the market.

Over the next cycle, the real divergence will come not from who can raise prices the fastest, but from who can keep compounding relevance while their customer base fragments. The brands that treat scarcity, creative focus and balance sheet strength as operating disciplines rather than marketing lines will still be standing in 2030. The rest will spend the decade relearning how to grow.

For Investors

On today’s numbers, the market is still paying a premium for certainty. Hermès and Richemont are the clearest quality compounders, Prada and Moncler offer the best risk‑reward in listed names, and Kering has effectively become a leveraged turnaround bet on Gucci.

The full valuation tables, risk grid, and 2026–2030 bull, base, and bear scenarios are available in an interactive dashboard for paid subscribers.

Prefer a visual, magazine‑style version of the free essay, with curated charts and brand breakdowns? Read it here: https://luxury-report-2026.theinterneteconomy.xyz/

If you want to work with me on strategy (brand resets, investor theses, AI roadmaps in luxury) or deep dives like this one, message me at jurgis@evoaai.com or on LinkedIn.